July 22, 2026

In a Nutshell

- With the November election drawing near, proposals to significantly reduce or even eliminate the state income tax have become prominent, but few details have been offered on how to either replace that revenue or absorb its loss.

- The income tax is the state’s largest single revenue source and makes up roughly 16 percent of the total state budget, but its revenue flows into the state’s two major revenue funds – the General Fund and the School Aid Fund – that drive much of budget decision-making. The tax makes up of 40 percent of these discretionary revenues.

- Eliminating the income tax without replacement revenue would necessitate major reductions to the some or all of the programs that receive the bulk of this discretionary revenue – programs such as Medicaid and human services, corrections, public education, revenue sharing, and state police.

Yesterday was April 15th – Tax Day. That means hundreds of thousands of Michigan taxpayers were putting the finishing touches on tax returns and sending them in to federal, state, and – for some – even city governments to meet the annual tax deadline. Few of those filers, however, would likely be able to answer this fundamental question: how are governments using these income tax proceeds?

In this election year, that question has become especially relevant to Michigan’s individual income tax. Several gubernatorial candidates have pledged to significantly reduce or even completely eliminate the tax with few, if any, details on plans to replace the lost tax dollars with new revenue from some other tax source or to absorb the revenue loss by shrinking specific areas of the state budget.

A basic understanding of the income tax’s role in financing public services will be critical to the public in evaluating these proposals as the November election nears.

To further that understanding, this brief examines the important role the income tax plays in financing state programs and services. The income tax is the state’s largest tax in terms of revenue collections, but its revenue is all deposited into the state’s two major discretionary revenue funds – the General Fund and School Aid Fund. Large portions of the state budget receive no support from income tax revenue, and the brief identifies the public services that are – and are not – supported by income tax proceeds to help illustrate the fiscal trade-offs policymakers would face with major reductions to the tax absent replacement revenue sources.

A Primer on State Revenues

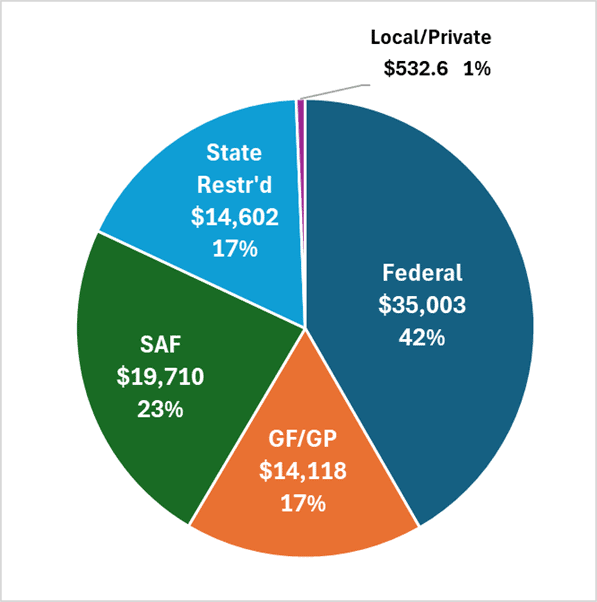

Before turning specifically to the income tax, it’s helpful to establish a general grounding in the revenues that support the state budget as a whole. The Fiscal Year (FY)2026 budget includes $84.0 billion in total appropriations to support the myriad programs administered by the state. Chart 1 breaks out the revenue sources supporting these appropriations.

Federal funding plays a vital role in financing the state budget. Forty-two percent of total state appropriations – around $35 billion – come from Washington D.C.. Federal funding supports an array of different public programs administered by states. Importantly, all these federal revenues are allocated for specific programs and purposes; states have no discretion to use them for anything else. The largest tranche is dedicated to state-administered Medicaid programs. Michigan’s Medicaid program taps over $21 billion in federal matching funds to provide health care coverage for low-income households, almost 60 percent of all federal dollars coming into the state budget. Federal funding also provides support for other public services, including K-12 education, public assistance and child welfare programs, highway and bridge infrastructure, and workforce development.

Chart 1

FY2026 State Budget by Fund Source

(millions)

Source: House Fiscal Agency, Appropriations Tracking and School Aid Budget Briefing

Virtually all of the remaining budget is supported by state revenues, but it’s important to note that – like federal revenues – a sizable amount of that state money also comes with use restrictions. In making annual state budget decisions, lawmakers must honor constitutional and statutory restrictions attached to this state revenue. About $14.6 billion falls into this category (17 percent of the total budget). The great majority of this revenue comes from two sources: motor fuel and vehicle registration tax revenue constitutionally dedicated to transportation infrastructure; and statutorily created taxes on health care providers that help leverage federal dollars to support the state’s Medicaid program. However, there are hundreds of smaller taxes and fees covering everything from driver’s and hunting/fishing licenses to regulatory fees on banks and insurance companies to different environmental fees and assessments that are also part of this category and have restrictions in their use.

That brings the discussion to the two remaining revenue categories: General Fund/General Purpose (GF/GP) and School Aid Fund (SAF). While these funds finance only about 40 percent ($33.8 billion combined) of FY2026 total appropriations, their discretionary nature makes them the primary focus within annual budget deliberations. The state’s major taxes (e.g., income, sales and use) generally flow into these two funds.

School Aid Fund appropriations total $19.7 billion in FY2026, making up 23 percent of the whole budget. This revenue is dedicated to public education which includes public K-12 schools as well as smaller appropriations for community colleges and public universities. In that sense, the School Aid Fund is restricted in nature. But since public education is a massive component of the state budget, deciding how to use these dollars within the broader context of “public education” involves critical decisions.

Finally, $14.1 billion in GF/GP appropriations make up the final 17 percent of the budget. GF/GP revenue represents the state’s wholly discretionary revenue pool. State policymakers can elect to use this revenue for whatever is of the highest priority.

Use of State Income Tax Revenue

The income tax is a prominent source of funding for the state budget generally, but it plays an even more critical role within the more discretionary GF/GP and SAF revenue pools which drive state budget decisions every year.

As background, the 1963 Michigan Constitution prohibits the state and local governments from levying an income tax with a graduated rate and/or base (i.e., rates/base change with income levels). Ever since 1967 when the state first authorized the income tax, it has been assessed with a flat tax rate (i.e., fixed rate for all taxpayers regardless of income). Currently, the rate is 4.25 percent. This rate is applied to a taxpayer’s adjusted gross income as reported to the federal government, but only after applying a host of Michigan-specific exemptions and credits. Based on the January 2026 state revenue estimates, the tax is expected to generate around $13.6 billion during FY2026.

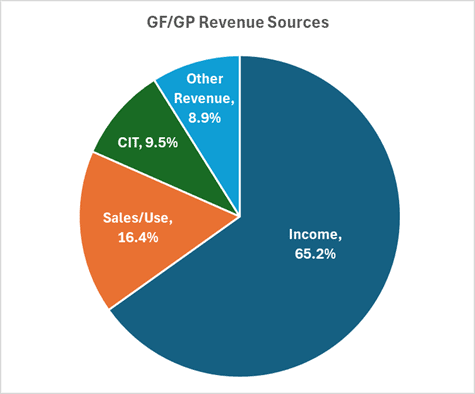

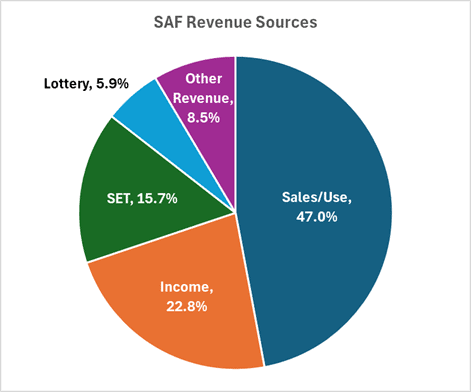

But here lies the conundrum for policymakers seeking to reduce the income tax burden. Doing the math, income tax revenue by itself makes up just over 16 percent of the state budget. That’s already a significant amount, but as was illustrated, most of the budget comes from other revenue sources. So, what specifically does the income tax support? Answering that question requires an analysis of the income tax’s contribution to the discretionary GF/GP and SAF revenue pools (see Chart 2).

Chart 2

Income Tax Revenue as Share of GF/GP and SAF, FY2026

Source: Research Council analysis of January 2026 Consensus Revenue Estimating Conference detail

The income tax is expected to contribute $9.2 billion to GF/GP revenue in FY2026 and is the predominant source for this fund (65 percent of total GF/GP). State sales and use taxes – the next highest contributor – support just 16 percent and the corporate income tax another 10 percent of all GF/GP resources. For the School Aid Fund, the income tax plays a different role; it is expected to generate $4.4 billion for the SAF, making it the second largest contributor (23 percent) behind sales and use taxes (47 percent). Other major SAF revenue sources include the State Education Tax (SET) and net proceeds from State Lottery operations. Combined, the income tax revenue provides 40 percent of all GF/GP and SAF resources.

Implications of Eliminating the Income Tax with No Replacement Revenue

So, what does this imply for proposals calling for the elimination of Michigan’s income tax without some form of replacement revenue to offset the revenue impact?

Without that income tax contribution and no replacement revenue to the School Aid Fund, public education funding would have to be reduced by 23 percent to bring appropriations in line with revenue.

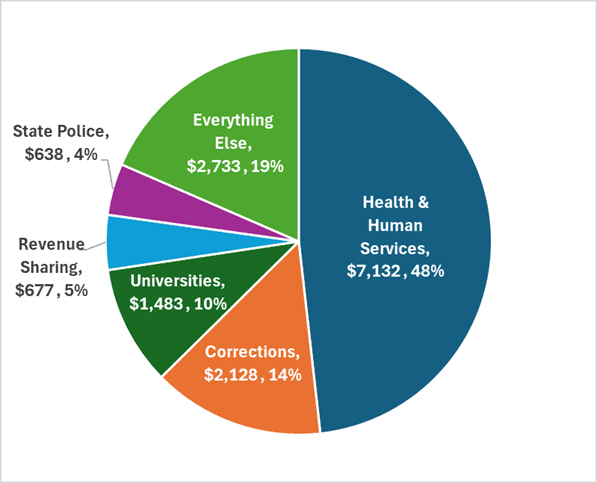

The impact would be much larger on the GF/GP side of the budget to address the resulting 65 percent revenue decline. Notably, Chart 3 shows over 80 percent of GF/GP appropriations are tied to five major state departments and programs. By itself, the Department of Health and Human Services absorbs 48 percent of the state’s discretionary GF/GP revenue to support Medicaid, child welfare, mental health, public health, and other social services.

Chart 3

GF/GP Appropriations by Department/Program

(millions)

Source: House Fiscal Agency. Chart includes appropriation for statutory revenue sharing which, for technical reasons, are not directly appropriated as GF/GP but do come from GF/GP revenue.

The other four areas include

- The Department of Corrections budget, which supports personnel costs for corrections officers and other staff as well as food service and legally-mandated health care services for incarcerated prisoners;

- State support to public universities and community colleges, which then helps to subsidize tuition costs for college students;

- Statutory revenue sharing allocations to local units of government in Michigan;

- And support to the Department of State Police in providing state trooper coverage.

The “Everything Else” portion of Chart 3 represents the $2.7 billion in GF/GP revenue appropriated to every other department, agency and program within state government. If all of that funding were eliminated to help address the loss of income tax revenue, these five major programs would still face reductions of more than $6.4 billion with the loss of income tax revenue. That amounts to a 54-percent reduction from FY2026 GF/GP appropriations across all five areas.

In short, eliminating the income tax without any revenue replacement would require a fundamental restructuring of these core services. Operational efficiencies and reforms to programs and services are wise endeavors and critical to legislative oversight, but those strategies, by themselves, cannot generate the budget savings necessary to absorb the substantial revenue loss that would come from eliminating the income tax. On the contrary, the loss of $14 billion from the GF/GP and SAF budgets would require large-scale reductions to some or all of the five major GF/GP-funded departments/programs as well as to public education appropriations.

State lawmakers have an appropriate and necessary responsibility as guardians of the public purse to ensure that state government spending is both efficient and necessary. Cost-saving strategies though efficiency improvements and eliminating programs that don’t bring value to the public are both important parts of this role. But, both lawmakers and the public should enter policy debates on major tax restructurings open-eyed with regard to the magnitude of the budget impacts of the reforms. Major changes to the income tax translate to major changes to the state budget.