July 28, 2026

In a Nutshell

- A perennial, and often contentious, issue has been the use of School Aid Fund (SAF) dollars to finance appropriations for Michigan’s community colleges and four-year universities. This is likely to be a hot topic again as the governor and lawmakers sit down to write the upcoming Fiscal Year (FY)2027 state budget.

- A more complete and comprehensive review of the School Aid Fund/General Fund funding swap resembles more of a two-way street with resources moving in both directions; from the SAF to the General Fund budget, and vice versa.

- The flow of dollars out of the General Fund to “hold harmless” the SAF and public schools from the potential revenue losses arising from various state tax policy changes has grown over time. Collectively, “hold harmless” provisions are estimated to reach $900 million for the FY2027 budget year, or about 70 percent of the total $1.3 billion SAF appropriation for higher education purposes. Understanding the two-sided relationship between the two funds will enhance the discourse during the upcoming state budget deliberations.

Another Michigan state budget season is upon us. A perennial, and often contentious, issue has been the use of School Aid Fund (SAF) dollars to finance appropriations for Michigan’s community colleges and four-year universities. This is likely to be a hot topic again as the governor and lawmakers sit down to write the upcoming Fiscal Year (FY)2027 state budget. Updated revenue forecasts for the SAF and the General Fund, the state’s two main discretionary checking accounts, face very different near-term trajectories. Current projections show that money flowing into the SAF is estimated to grow modestly in FY2027, while General Fund revenue is projected to decline year-over-year. As our recent budget analysis shows, this will put even more pressure on the General Fund side of the budget and make an already challenging budget cycle a little more difficult.

As policymakers turn their attention to the FY2027 budget, some may eye the healthy School Aid Fund as a partial relief valve to address General Fund budget pressures. This has been a popular budget maneuver over the past 15 years. The School Aid Fund is already picking up $1.3 billion of higher education appropriations; the result of years of shifting what otherwise would be General Fund spending to the SAF side of the state budget. Rest assured, given the budget challenges ahead, there will be proposals from some corners to dip further into the SAF.

Because responsibility for community college and university funding had historically been placed on the General Fund, public school interest groups and politicians publicly characterize the current $1.3 billion in SAF higher education appropriations as a “raid” or “skim” of dollars away from K-12 schools, breaking with the spirit of 1994’s Proposal A. The Research Council sees the issue as being a bit more complex. In fact, Michigan’s constitutional history and evolving state fiscal architecture suggests the same.

A more complete and comprehensive review of the School Aid Fund/General Fund funding swap resembles more of a two-way street with resources moving in both directions; from the SAF to the General Fund budget, and vice versa. In fact, the Research Council estimates that there is nearly $750 million of General Fund resources this year effectively baked into to various SAF “hold harmless” provisions that were created as part of state tax policy changes dating back to Proposal A. But, unlike the $1.3 billion SAF appropriations for higher education that are clearly visible in state budget documents, the General Fund’s “hold harmless” obligations are largely shielded from public view. These obligations don’t show up in state budget reports, but they are incorporated into the details of annual revenue estimates for both the General Fund and School Aid Fund.

Much like the perpetual public confusion and misunderstanding about the role that Michigan Lottery proceeds play in funding K-12 schools, there is a growing tendency in state budget circles, as well as the public narrative, to view the General Fund/School Aid Fund swap only through the lens of the SAF appropriation for higher education. Here, the Research Council expands the aperture on this funding swap to provide insights into the true relationship between these funds and share important context that often gets little attention during annual state budget deliberations.

A Bit of Constitutional Background on the School Aid Fund

The School Aid Fund was already four decades old when voters approved the 1994 Proposal A constitutional amendment, Michigan’s landmark K-12 school finance and tax reforms. A deeper understanding of this history, including language added to the constitution during the 1961 constitutional convention, is critical context to better understand the current debate around the SAF/General Fund swap.

The School Aid Fund was first established as separate and distinct from the state’s General Fund through a 1954 amendment to the 1908 Michigan Constitution. Although public K-12 schools had been receiving a portion of the state sales tax levy (one half of one cent of the three-cent sales tax rate) since the adoption of a 1946 constitutional amendment, it was not until the 1954 amendment that these receipts were designated for deposit into a separate “school” fund, creating the School Aid Fund in Article X, Section 23 of the 1908 Constitution. The 1954 amendment also increased the earmark amount (two cents of the three-cent sales tax rate) and limited the use of SAF dollars for “aid to school districts and school employees’ retirement purposes.”

The 1963 Michigan Constitution maintained the SAF as a separate fund (Article IX, Section 11) and continued the sales tax earmark (one half of the four-cent state sales tax). But importantly, the new constitutional language expanded the use of the fund to include “higher education”. Interestingly, this language change did not get incorporated into the proposed text of the new constitution until the very last day of the convention. All previous committee drafts considered by convention delegates referred to “public education and school employees’ retirement.” The language’s sponsor, Alvin Bentley, characterized the inclusion of “higher education” in the constitution as a “technical” change when he presented to the Committee on Style and Drafting on August 1, 1962, hours before the final convention vote to approve the revised state constitution.

Fast forward 30 years. As part of 1994’s Proposal A school finance reforms, voters again modified the SAF’s constitutional language. As part of the broad shift in public school funding responsibility from local property taxes to state-levied taxes, Proposal A’s constitutional changes increased the existing four-cent sales tax earmark (from 50 to 60 percent) and raised the sales tax rate by two cents (dedicating 100 percent of the proceeds from this rate increase to the SAF). While the amount of earmarked sales tax revenue flowing into the SAF jumped dramatically, the constitutional language around the permissible uses of the fund were unchanged under Proposal A. One can reasonably surmise that the architects of Proposal A did not see the “higher education” language as problematic to the operations of the new school funding system, either at the time of implementation or into the future.

State Budget Challenges Breathe Life into Dormant Provision

This constitutional provision laid dormant for decades as SAF dollars were appropriated exclusively for traditional purposes – aid to public K-12 schools and school employee retirement obligations. Although the 1963 Constitution has always allowed School Aid Fund dollars to be used for “higher education”, state leaders did not tap the fund for this purpose for nearly 50 years. Appropriation decisions to use SAF dollars for higher education trace back only 15 years and were born out of the fiscal pressures to address a long-standing structural imbalance in the General Fund budget.

The first non-traditional use of SAF for higher education came at the end of Governor Jennifer Granholm’s term in office. At the time, lawmakers directed a $208 million SAF appropriation in the FY2010 community college budget to offset a similar reduction in General Fund spending, allowing those resources to be shifted to address the budget shortfall. This was part of a larger suite of General Fund budget-balancing actions involving several one-time, nonrecurring budget fixes. At the time, the SAF transfer to the community college budget was seen as a “one-off”, short-term fix for the General Fund budget. But any sign that the General Fund/SAF budget swap would be temporary were short-lived.

Two years later, the funding swap became a more permanent fixture in the state budget. Facing an estimated $1 billion General Fund structural budget deficit in FY2012, newly elected Governor Rick Snyder proposed tapping into the SAF for higher education purposes as a key component of his 2011 tax and spending plan. To address portions of the state’s on-going fiscal problems, while accommodating the budget effects of the switch from the Michigan Business Tax to a new Corporate Income Tax and major adjustments to the Individual Income Tax, Governor Synder’s FY2012 budget recommendation included a proposal to move $800 million in SAF appropriations into higher education budgets.1 The final FY2012 budget scaled the amount down considerably, including $400 million as base funding for community colleges and universities, replacing state General Fund support. This move effectively freed-up the same amount of discretionary dollars to be used elsewhere in the state’s General Fund budget.

Since then, this funding shift has become a key and permanent feature of the state’s School Aid Fund/General Fund budget landscape. The entire community college budget has been funded from the SAF since FY2019, while SAF appropriations for the public university budget have ebbed and flowed with the financial health status of the General Fund.

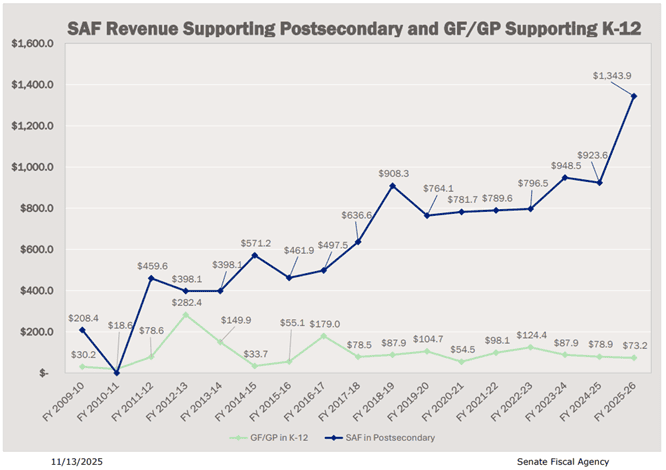

Most recently, as part of last year’s state budget/road funding deal, Governor Whitmer and the Michigan Legislature agreed to nearly double the university SAF appropriation from $462 million last year to $851 million in FY2026, jumping the total higher education appropriation from $923 million to $1.3 billion (45 percent) over the two years (Chart 1). Since FY2010, a cumulative total of $11 billion in higher education funding has been shifted into the SAF.

Chart 1

School Aid Fund Benefits from Several “Hold Harmless” Provisions

It is certainly true that, over the course of past 15 years, the School Aid Fund has picked up an increasing share of the responsibility for financing higher education appropriations. Today, 100 percent of the community college budget and over one-third of the public universities budget comes from the SAF. That is not in question. But, to stop the analysis and discussion of the SAF/General Fund budget swap at that juncture only tells half the story. A full accounting of the shifts in the revenue disposition between these major state funds and across the two budgets must consider several “hold harmless” provisions that have had the effect of the General Fund absorbing state revenue losses that would otherwise have hit the School Aid Fund. Consideration of these “hold harmless” provisions can provide a fuller and more accurate picture of how this fiscal swap impacts the state budget, both on appropriations and state revenue allocations to the two funds.

Even before state budget writers began using SAF dollars in the higher education budgets, lawmakers adopted “hold harmless” provisions to shield the SAF from state tax policy impacts. Starting in tax year 2000, the percentage of “gross” income tax collections earmarked to the SAF changed in material way. To guard the SAF from revenue losses arising from an income tax rate reduction, this statutory earmark was changed from a fixed percentage (23 percent) to a ratio (1.012 percent divided by the income tax rate). The inverse relationship between the income tax rate and the earmarking percentage prevents the reduction of funds to the SAF when the income tax rate decreases. All that revenue impact then falls to the General Fund. As the income tax rate was gradually cut from 4.4 percent to 3.9 percent in the early 2000s, the corresponding SAF earmark percentage increased from 23 percent to 25.95 percent as a function of the tax rate ratio written into state law. Based on current estimated “gross” income tax collections, this provision amounts to $143 million that would otherwise be pulled out of the School Aid Fund in FY2026 had these changes not occurred.

In addition to the provisions related to the income tax, the state also reimburses local school districts or the School Aid Fund directly for revenue losses tied to other tax policy changes. These reimbursement-based “hold harmless” provisions tap into existing state tax receipts that would otherwise go to the General Fund.

In 2014, policymakers included provisions to reimburse local school districts for revenue losses associated with the newly enacted personal property tax exemptions. Through a complex formula written into state law, the Department of Treasury annually reimburses school districts for lost revenue from various debt and non-debt millages. Based on current local school taxable values and millage rates, Treasury estimates that public school districts (local and intermediate) will receive close to $90 million in FY2026. These reimbursement payments come from a portion of use tax proceeds that would otherwise go the state’s General Fund.

Most recently, Michigan’s new 2025 transportation funding package exempts the sale of motor fuel from the state sales tax. Because nearly three-quarters of the sales tax revenue is earmarked to the School Aid Fund, any reduction to the sales tax base (removal of motor fuel purchases) has a substantial revenue impact. As part of the overall funding package, state law was amended to hold the School Aid Fund harmless from the motor fuel exemption. As such, the Department of Treasury must annually calculate this revenue loss and deposit the full amount from the General Fund into the School Aid Fund. This reimbursement is estimated to cost the General Fund $469 million in FY2026, by far the largest of all the SAF “hold harmless” enacted since the state began using the School Aid Fund for higher education.

Similar, yet much smaller, SAF reimbursement requirements for sales tax exemptions tied to the purchase of feminine hygiene products and data center equipment. As with the motor fuel exemption, the Department of Treasury must estimate the amount of “lost” sales tax dollars to the School Aid Fund and reimburse the full amount from the General Fund. These inter-fund deposits are baked into the official revenue estimates for both funds, but don’t show up in the actual budget bills. While both types of “hold harmless” provisions (income tax earmarking and reimbursement-based) differ on their mechanics, their effects are the same – reduce state General Fund dollars available to program into the state budget.

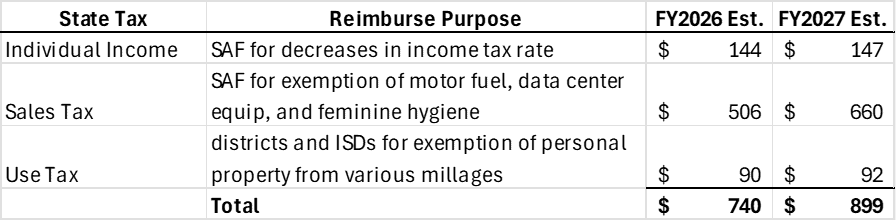

Table 1 provides estimates of the various SAF “hold harmless” provisions coming out of the state General Fund for FY2026 and FY2027, based on current state tax law.

Table 1

Current Estimated GF to SAF “Hold Harmless” Provisions (millions)

Source: Consensus Revenue Estimating Conference detail documents, January 2026

Michigan’s Evolving Fiscal Landscape – Blurring the Lines Between the General Fund and School Aid Fund

In several respects, the current fiscal interplay between the state’s two primary funds is a byproduct of Proposal A school reforms. These reforms shifted the primary responsibility for funding K-12 schools to the state government and state-levied taxes, and away from local school districts and local property taxes. In addition, annual school funding decisions shifted from local school boards and locally-approved millage rates to Lansing lawmakers as part of the state budget process. The School Aid Fund was already an important component of the overall funding structure for public schools, but the fund took on much broader funding responsibility in the post-reform period as SAF tax collections grew and the state’s role in funding K-12 education expanded.

Today, annual School Aid Fund and K-12 school funding decisions effectively compete with other state programs and services for limited state resources on two fronts – budget and tax policy. On the budget front, this competition largely plays out in annual appropriation decisions involving the General Fund and School Aid budgets. Collectively, the two funds account for one-third ($35 billion) of the total $46 billion in state-sourced appropriations. For this reason, most legislative and public attention during state budget negotiations are focused on decisions regarding, 1) how much to spend on a specific program/service, and 2) how to finance the approved spending amounts (i.e., what funding source to use). The direct flow of SAF dollars to support higher education appropriations ($1.3 billion in FY2026) is just one side of the fiscal relationship between the General Fund and School Aid Fund budgets.

While the competition among state programs and services for General Fund and School Aid Fund dollars is directly reflected in appropriation decisions, this competition also plays out when policymakers adjust the state tax code and decide how to allocate tax revenues among the two funds. Equally important is the flow of dollars out of the General Fund to “hold harmless” the SAF and public schools from the potential revenue losses arising from various state tax policy changes. The number and size of “hold harmless” provisions have grown over time. Collectively, they are estimated to reach $900 million for the FY2027 budget year, or about 70 percent of the total $1.3 billion SAF appropriation for higher education purposes.

Since the adoption of Proposal A, these various “hold harmless” provisions have effectively pushed a larger portion of state-led tax relief (e.g., income, sales and use, property) to the General Fund. Shielding the School Aid Fund and K-12 funding from potential tax revenue losses, either through SAF earmarking or General Fund reimbursement, has had the practical effect of blurring the lines between the two funds.

Conclusion

Michigan policymakers face another tough budget cycle with challenges arising from a confluence of factors. Revenue and spending decisions will be influenced by downward revisions in tax revenue projections, the fiscal impacts arising from the recently-enacted $2 billion transportation funding package, as well as the budget impacts from various changes in federal safety net programs. According to state fiscal experts, these factors will entirely impact the General Fund side of the budget as current estimates now show a nearly $800 million spread between baseline spending and the amount of on-going General Fund dollars available for FY2027. Given Michigan’s evolving fiscal landscape since Proposal A, some policymakers are likely to look to the healthy School Aid Fund as a partial solution to future General Fund budget problems. Understanding the two-sided relationship between the two funds will enhance the discourse on these potential actions.

The business tax switch from the Michigan Business Tax (MBT) to the Corporate Income Tax (CIT), combined with personal income tax changes, resulted in a large reduction in business tax revenue and a net increase in personal income tax revenue. Because of earmarking provisions, the switch also eliminated dedicated MBT funding to the SAF. All CIT revenue is deposited in the General Fund. We note that the MBT (with the SAF earmarking) replaced the Single Business Tax (SBT) as the state’s primary business tax in 2008, with 100 percent of SBT collections directed to the General Fund. The current CIT revenue allocation (no SAF earmark) aligns with how the SBT tax revenue was allocated to state funds at the time of Proposal A. (Note: SBT was in effect from 1976 to 2008).