July 6, 2026

This post appeared in the Michigan Association of Counties’ magazine Michigan Counties

Even well-informed people can be ill-informed about how state finance works. (How many times have you been asked why the state lottery hasn’t rescued Michigan schools?) This month I will try to dispel some common misunderstandings about state government finance.

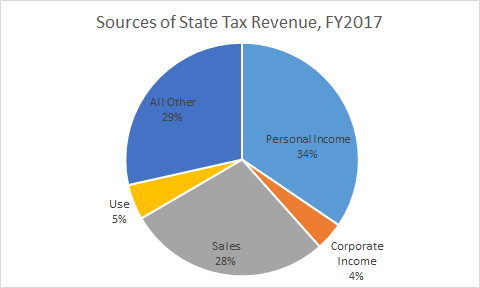

Misunderstanding No. 1: The state levies a lot of taxes yielding billions of dollars

Although the state levies 38 taxes generating nearly $33 billion to fund services and functions, very few contribute major amounts to the total. Income taxes — individual and corporate — contribute almost two-fifths of total state revenues. The sales and use taxes contribute another third. Revenues from all other taxes — on businesses, on the purchase of alcohol and tobacco, state property taxes, and transportation — contribute less than one-third of the total.

Source: Michigan Department of Treasury

Misunderstanding No. 2: State government is bloated

Spending by the state government in Michigan is unlike that of most other governments. About three-quarters of all state spending is to sent to other entities to provide services. Most of this goes to hospitals, other health providers, and human service providers for services such as Medicaid and public health. Funding is sent to K-12 school districts, community colleges, and universities for education. Cities, villages, and county road agencies receive funding for road maintenance. Once a significant line item, state revenue sharing to local governments remains but at much smaller amounts.

State government remains responsible for prisons, state police, and general administrative services.

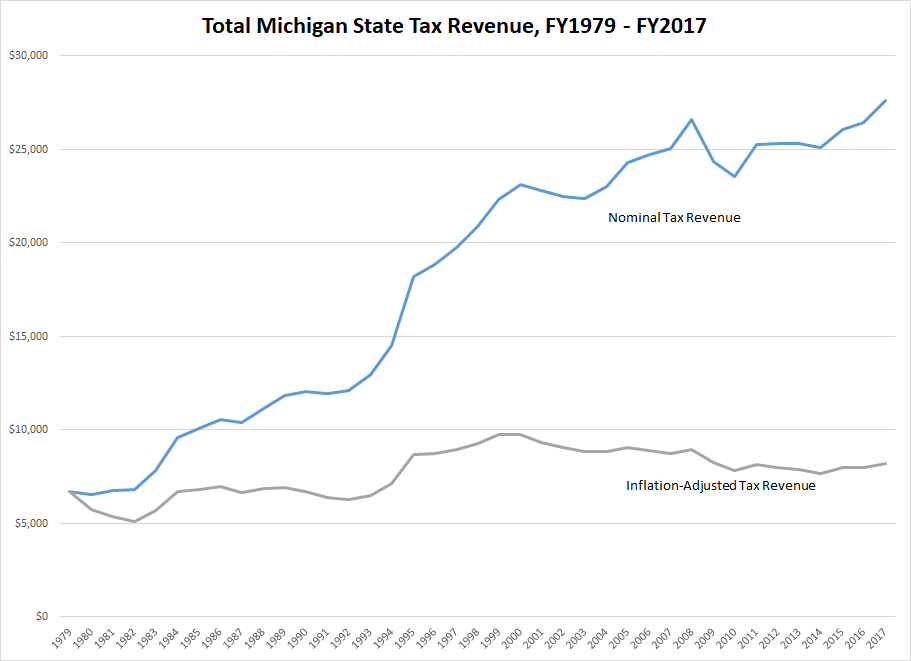

Misunderstanding No. 3: We are taxed more than ever

In raw dollar amounts, FY2017 tax revenues reached a new high water mark exceeding the previous high in FY2008. It took almost a full decade to recover from the devastating losses of the Great Recession. However, after accounting for inflation, FY2017 tax revenues are below FY2008, and well below FY2000 inflation-adjusted levels.

Source: Michigan Department of Treasury

Misunderstanding No. 4: With a $59 billion budget, there must be a lot of wiggle room

Advocacy for favored government services and inherent fear that future policymakers will alter past funding priorities has led to a great deal of tax earmarking, i.e. dedicating revenue for specific purposes, rather than leaving it to the legislature to distribute. Constitutional or statutory provisions leave elected leaders little discretion to make budgetary decisions. Transportation (fuel taxes and registration fees) revenues are dedicated, by the state constitution, to road care. Almost $16 billion of sales, use, income, property, liquor, and real estate transfer taxes are earmarked for school funding. Collectively, these services constitute more than one-third of the revenues. Other moneys are tied up as the need match for federal funding.

Only about $11 billion (less than 20 percent of the $59 billion) of tax revenues are not earmarked and end up in the state General Fund. But even then, there are expectations that funding will be used for prisons or Medicaid spending on an ongoing basis. The Senate Fiscal Agency estimates that only about $5.3 billion (9 percent) of state revenues are truly discretionary.

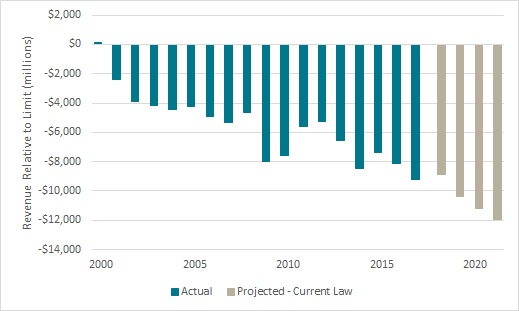

Misunderstanding No. 5: Michigan is a high-tax state

There are two ways of looking at this. One approach is to compare how much taxes were paid in the past and the other is to look at Michigan’s taxes relative to other states. Voters amended the Michigan Constitution in 1978 — commonly referred to as the Headlee Amendment — to provide a number of state and local tax limitations. Among those was a provision that if total state revenue exceeded the proportion of personal income in that fiscal year, the excess is to be refunded to taxpayers. This provides a benchmark for state revenue relative to the wealth of its residents. Using this measure to compare where Michigan taxes are, and have been in the past, shows that state revenues are a declining proportion of state personal income. The state is expected to be more than $10 billion below that limit at the end of this fiscal year. Twenty years ago, the state was right at the limit. While total state revenues are higher than they have ever been in raw dollar amounts, we’re collecting a smaller percentage of personal income than we did in past years.

Source, House Fiscal Agency

Alternatively we can look at Michigan state and local tax revenue relative to other states. For this we can look to statistics compiled by the U.S. Census to track economic activity related to taxes and government spending. From at least as far back at the 1960s through the beginning of this century, Michigan was considered a high-tax state — usually ranking in the neighborhood of 13th to 16th in per-capita tax revenue among the 50 states. This changed drastically because of Michigan’s troubled decade and the Great Recession. Michigan now ranks 34th among the states.

Misunderstanding No. 6: Lottery money was diverted to non-school purposes

As mentioned above, Michigan has a habit of tying revenues to favored services. This became a very public exercise when voters were asked to permit a state lottery in a 1972 constitutional amendment, with the promise that revenues would be used for school funding. In approving the funding it became an extreme example of the fungibility of money. Adding a dedicated revenue to school funding has at times allowed state policymakers to use resources previously used for school funding for other purposes.

Beyond that, it is a minor funding source. Lottery revenues contribute only $1 billion (8 percent) of the $13.6 billion of funding sources dedicated to schools.

Misunderstanding No. 7: A huge amount of road money goes to non-road issues (transit, ports, etc.)

The public approach to the use of transportation money (gas tax and vehicle registration fee revenues) has gradually — very gradually — shifted from roads to “mobility,” i.e. all the ways people get around their environments. The Michigan Highway Department became the Michigan Department of Transportation. Some road funding was used for transit. To keep this development constrained, the state Constitution was amended in 1978 so that no more than 10 percent of road funding can be used for transit. The state usually appropriates the full 10 percent. The state uses revenue from other sources for ports, airports, and other transportation issues.

A $59 billion pool of money can be irresistible for armchair pundits and their opinions. But this pool has lots of roped-off areas; free swimming is very limited.