February 24, 2026

In a Nutshell

- Several Michigan counties were hit hard by the loss of property values resulting from the Great Recession. Property owners and local governments in these counties have navigated those lost values in the 17 years since the economic downturn began.

- A comparison of the most recent market values to inflation-adjusted 2008 values shows that property owners in most of those communities have recently or will soon enjoy full recovery of the lost values.

- A similar comparison of taxable values to inflation-adjusted 2008 taxable values shows that local governments in these counties have a ways to go to recoup the lost purchasing power their property tax bases afforded them.

Property owners in communities hit hard by property value reductions caused by the Great Recession recently or soon will have property values that exceed the inflation-adjusted value of the properties in 2008. New developments and the appreciation of existing properties are reflected in 2024 appraisals of property values. However, because the annual growth of the property tax base is capped, taxable values are recovering at a much slower rate. This affects the revenue-raising ability of local governments and their purchasing power. The loss in purchasing power affects their ability to maintain service levels.

The Detroit News recently published a quick analysis of changes in home values in Wayne, Oakland, and Macomb Counties. The main takeaway from the story was that 17 years after residential properties began declining as a result of Michigan’s declines in work opportunities and the foreclosure problems that plagued many areas, most of the cities and townships in these three counties have rebounded to pre-recession levels.

The problem with this back-of-the-envelope analysis is that inflation has eroded purchasing power over these 17 years. Real estate is the most common investment for most families. While a home is a place to live, property purchasers often hope the appreciation in value will pay dividends allowing them to move into larger homes or to downsize and use the gains to live a comfortable retirement. As is the case for any investment, the long-term investing aspiration is to exceed inflationary increases. To the extent that the value of the average property reflects the community or county averages discussed below, communities in the counties hit hardest by losses in property values because of the Great Recession have a ways to go to exceed the pre-recession, inflation-adjusted value of the properties.

Lost Property Value

Michigan was hit hard by the Great Recession (2007-09). After several years of economic malaise felt only in Michigan, the nationwide recession hit the Michigan economy relatively hard and affected property values in ways that most recessions do not. Property values statewide fell by 23 percent while taxable values declined 13 percent.

The effects were uneven, affecting some types of properties more than others and some regions and communities especially hard.

The taxable value of residential property declined 20.5 percent from 2007 to 2012. Commercial property declined from 2007 to 2012 in about the same inflation-adjusted amount as it had gained in the seven years before.

In contrast to the other classes of property, the value of industrial property had not grown much before the Great Recession and so the losses caused by the Great Recession were felt more severely.

Consequently, the parts of the state with the greatest concentrations of industrial activity were impacted the most severely by the Great Recession. Wayne and Genesee counties (-33 percent) fell the furthest below their peak values from 2007 to 2012, followed by Macomb (-28 percent), Oakland (-26 percent), and Midland (-25 percent).

Out of 1,515 cities and townships, 248 (16.4 percent) had inflation-adjusted taxable values in 2016 that were below their respective 2000 taxable values. This group included 169 cities and 79 townships, located in every region of the state and in 64 of the 83 counties. Almost half (48 percent) of the state population resided in a city or township that had a 2016 taxable value that was below the unit’s 2000 level.

These 248 local governments as a group had inflation-adjusted taxable values that were $33.5 billion (21.8 percent) below their 2000 values. Collectively, they lost 20.3 percent ($13.8 billion) of the residential taxable value that they had in 2000; 7.9 percent ($1.6 billion) of the commercial taxable value; and 51.1 percent ($5.6 billion) of the industrial taxable value.

One-half of the 248 local governments were located in nine counties – Bay, Genesee, Macomb, Midland, Monroe, Oakland, Saginaw, St. Clair, and Wayne. Wayne, Oakland, and Macomb Counties are home to 37 percent of the 248 local governments.

Not only were the tax bases of local governments in these counties affected by the loss of industrial tax bases, but many workers displaced by the decline in industrial activity sold their properties for less than they were worth when they sought employment elsewhere or faced foreclosure, thus accelerating the decline in residential property values.

To investigate the recovery, data was pulled for Calhoun, Dickinson, Genesee, Midland, Oakland, Saint Clair, and Wayne Counties.

Market Values

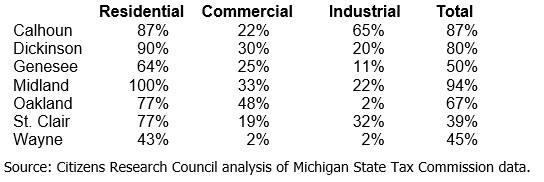

Table 1 reports the percent of cities and townships in each county for whom the 2024 values of properties as appraised by city and township assessors meet or exceed the inflation-adjusted values of those properties in 2008. Nearly all of the communities in Midland, Calhoun, and Dickinson Counties have met this threshold. Two-thirds of communities in Oakland County have met this threshold, but no more than half of the communities in Genesee, Wayne, and St. Clair Counties have met this threshold.

Table 1 helps to understand how properties are recouping lost values. While most of the communities have done well at recouping lost residential property values, far fewer communities have recouped lost commercial and industrial property values. Only two percent of the communities in Oakland County have recouped lost industrial property values and only two percent of communities in Wayne County have recouped lost commercial and industrial property values.

Table 1

Percent of Cities and Townships in each County that have at least Recovered to Inflation-Adjusted 2008 State Equalized Values

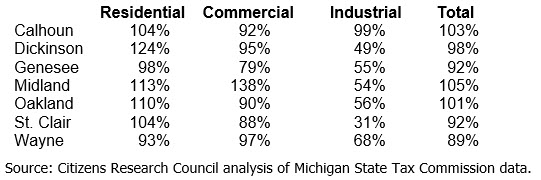

Looking at the data in a different way (see Table 2), only the county-wide value of property exceeds inflation-adjusted values in Midland, Calhoun, and Oakland Counties. The others have nearly recouped the inflation-adjusted 2008 values. Recovery of the lost values has been driven by gains in residential and commercial property values; except for Calhoun County, industrial property values severely lag their inflation-adjusted 2008 values in each of the counties. This county-wide data can be deceiving because changes in larger governments, or especially large changes in mid-sized governments, can obscure the changes happening in the balance of the county.

Table 2

2024 County-wide State Equalized Value as a Percent of Inflation-Adjusted 2008 State Equalized Value

Taxable Value

Local governments pay attention to changes in property market values for different reasons. Unlike homeowners who see the changes in market values through the lens of a major, long-term investment, municipal governments of all types and sizes view values as the tax base upon which property taxes are levied to generate the majority of their tax revenues.

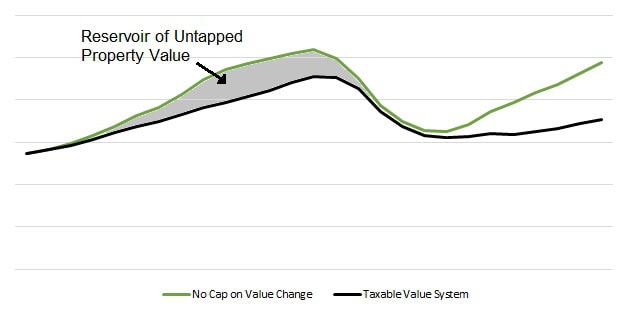

The measure of property value is modified for taxation purposes through limits placed on the taxable value of each parcel of property. The Michigan Constitution caps the annual growth of the taxable value for each parcel by the lesser of the rate of inflation or five percent, unless property ownership is transferred. Upon a change in ownership, the taxable value of a parcel is reset to its market value.

As we explored in our analysis of Michigan’s tax limitations, Michigan’s use of the taxable value system for valuing property for taxation limited the amount of decline during the Great Recession, but the system also moderated the rate of increase since the recession. Both statewide measures of value dropped sharply because of the Great Recession’s effects on property values, but the drop was sharper for SEV.

In essence, the mechanics of the TV system allowed the value of individual property parcels to continue to grow by the rate of inflation even while SEV was declining. This allowed local government revenues to continue to grow in some instances while property values declined. In other words, the untaxed property value (i.e., the gap between SEV and TV) did not represent a lost tax base as much as a reservoir of property value that could minimize the decline during the economic downturn.

The difference between the market value and the taxable value creates a reservoir of property value

After values reached their nadir and began recovering, the annual growth rate in the post-recession period has been slower than what was experienced in the pre-recession period. The post-recession growth of taxable values has not kept pace with the rate of inflation. The relationship between the appreciation of property values and tax revenues is diminishing. The property values in most communities have recovered from the losses caused by the Great Recession.

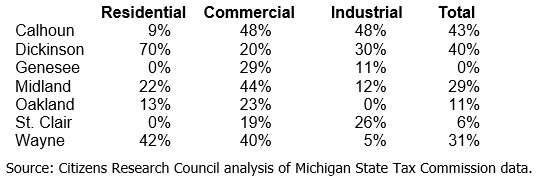

Table 3 reports the percent of cities and townships in each county for whom the 2024 taxable values of properties meet or exceed the inflation-adjusted taxable values in 2008. Here the restrained rate of growth is very apparent. Communities in Calhoun and Dickinson Counties have fared the best at recouping lost taxable values, but less than half of the cities and townships in these counties have done so. No community in Genesee has exceeded its inflation-adjusted 2008 taxable value and only two townships in St. Clair County have done so.

Recovery in Calhoun and Dickinson Counties has taken different paths. Nearly half of the cities and townships in Calhoun County have recovered their commercial and industrial taxable values. Recovery of residential taxable value has driven the rebound in Dickinson County.

The slow rate of recovery in the other counties is evident from the few cities and townships that have exceeded their inflation-adjusted 2008 taxable values for residential, commercial, and industrial properties. Not a single community in Genesee and St. Clair Counties have 2024 residential taxable values that exceed their 2008 values and only three cities in Genesee County have industrial taxable values that exceed their 2008 values. In Oakland County, no communities have seen the taxable value of their industrial property base return to the 2008 value. Only two communities in Wayne County have industrial taxable values that exceed the 2008 values.

Table 3

Percent of Cities and Townships in each County that have at least Recovered to Inflation-Adjusted 2008 Taxable Values

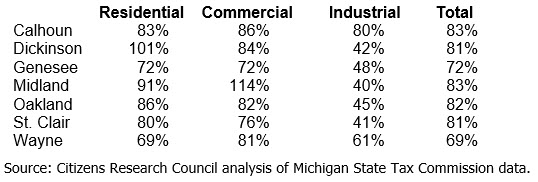

Table 4 shows that the 2024 county-wide taxable values have not exceeded inflation-adjusted 2008 values in any of the seven counties. County-wide commercial taxable value exceeds the inflation-adjusted 2008 value in Midland County, residential value exceeds the 2008 value in Dickinson County, and other components are nearing their 2008 values.

Notably, the recovery of industrial taxable values is at a much slower pace than residential and commercial values.

Table 4

County-wide 2023 Taxable Value as a Percent of Inflation-Adjusted 2008 Taxable Values

Analysis

Many things account for the slow rate of growth of both market values and taxable values. Detroit, Flint, and some of their inner-ring suburbs were hit particularly hard by foreclosures, job loss, and population exodus. Commercial values are affected by Internet sales causing the closure of many brick-and-mortar stores and some restaurants did not survive the disruption caused by social distancing orders during the pandemic.

The slow rate of recovery of industrial values reflects the larger issues confronting Michigan as it seeks a path to transition from a manufacturing economy in the 20th Century to a new technology and service economy in the 21st Century.

The differences between the market values of property and the taxable values that serve as the tax base for property taxes are evident. Some 10 years removed since property values hit their lowest points, the tax bases of local governments in counties that are home to almost 20 percent of the state’s population are growing at such a pace that maintenance of service delivery will continue to be a challenge for some time to come.

Policy Responses

Local governments have responded to the slow recovery of taxable values with the options afforded them. Local government is smaller today than it was 20 years ago. Those hit hardest by the loss of property values have created a new normal in the services provided to their residents.

In our follow-up paper after investigating property tax limitations, we documented the change in property tax rates local governments are applying to smaller tax bases. We found that from 2004 to 2020, the average county rate increased 17 percent, the average city rate increased 14 percent, and the average township rate increased 19 percent. The majority of local governments had higher tax rates in 2020 than they did in 2004.

State policymakers should take note of these trends. Unlike many other states, Michigan law affords local governments very few revenue-raising alternatives. The heavy reliance on property taxes in Michigan amplifies the significance of the property tax base trends.

Additionally, these trends shine a bright light on the reform of state revenue sharing. While the proposed state budget begins to restore funding to local governments that have long been neglected, without revisiting the funding formula to distribute the funding in a meaningful way to recognize variances in revenue-raising capacity (which are amplified by Michigan’s taxable value system) and local service demands, the additional state investments may not be put to their highest and best use.

Conclusion

The good news for property owners in communities hit hard by property value reductions caused by the Great Recession is that the value of their properties has recently or soon will exceed the inflation-adjusted value of the properties in 2008. The length of time to recognize the recovery speaks to the severity of the impact that the economic downturn had on several Michigan communities.

The troubling news is that the values upon which property tax rates are levied, taxable value, are recovering at a much slower rate. With property taxes as the primary source of revenue, this trend has caused losses in purchasing power of the revenues generated.

Efforts to engage in place-based investments in Michigan’s communities assumes that the local governments have the capacity to engage in these investments. The slow recovery of the property tax base challenges local governments’ ability to maintain current services even before they contemplate taking on new activities.