December 4, 2025

In a Nutshell:

- As a new legislative session takes shape, state policymakers are setting their agenda to grow Michigan into a prosperous state. Policymakers should put local government finance reform on their agenda.

- Well-managed and sustainably financed communities are a key component to the state’s economic success. To fund increasing operating costs and demands for improved public services, Michigan’s local governments may seek approval for new property tax increases.

- To allay potential concerns from inflation-weary homeowners and businesses about rising property tax burdens, policymakers should authorize local governments to access alternate revenue options as well as restore stability to the state’s revenue sharing program.

Paying for Local Community Services

The nearly $19 billion in property taxes collected each year funds Michigan’s essential local government services and public schools. And these taxes continue to rise.

Since 2013, statewide property taxes have risen an average of four percent year over year. From 2021 to 2022, statewide property tax collections rose 5.82 percent, followed by another 7.34 percent increase from 2022 to 2023. During these same years, Michigan personal income rose just 1.9 percent in 2022, and 5.3 percent in 2023.

Michigan taxpayers are not alone in seeing rising property taxes. Several efforts to control property tax growth have found success across the country. It would be prudent for policymakers to anticipate that such taxpayer frustration may find its way to Michigan. Last year, a group of concerned taxpayers launched a proposal to repeal all property taxes. The ongoing effort calls for sharing some statewide tax revenues only to fund certain essential government and infrastructure services (in addition to existing revenue sharing). Michigan’s property tax system is far from perfect, but with voter-approved guardrails in place, it is a predictable and administratively efficient source of revenue for local governments. It is also a tax that tends to have less impact on economic growth than a sales tax or income tax.

Tax economists explain that because property taxes are more transparent and visible than sales taxes or income taxes, taxpayers notice their tax burden rising more easily. For example, most homeowners would be hard-pressed to recall the total sales taxes paid in a year but would easily be able to calculate their total summer and winter property tax bills. And for many, income tax withholding assists taxpayers in making incremental payments toward what they will owe on their annual income tax return. They often receive an income tax refund, rather than needing to send an additional payment when the tax is due in spring.

Property owners can clearly see the amount of taxes due as they appear on one or two tax bills. They also can readily see the benefits from the property taxes they pay in their communities through the services they access routinely. Finally, property taxes may not alter a taxpayer’s economic decisions as much as a sales tax on purchases or an additional income tax because the tax is applied on a fixed asset, the land and the building upon it.

Funding for Local Governments

Local units of government rely on community-based property tax revenues and user fees. They also receive funding from the state and federal governments, either through state grants for specific programs such as infrastructure, public health, and courts, or through unrestricted revenue sharing payments. No local government can levy a local sales tax, while cities can levy a city income tax. The significant reliance on state aid and revenue sharing by local governments, plus the state restrictions on local option taxes underscores the nature of Michigan’s decentralized system of delivery for public services with a centralized public finance system.[1]

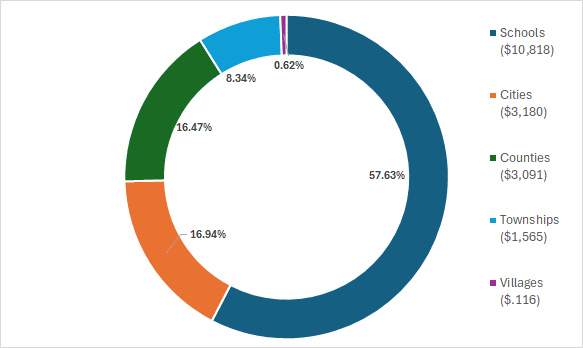

Statewide, property taxes raised $18.7 billion (2023) in revenues; 42.4 percent funded local governments, and 57.6 percent funded public schools (local school millages and the 6-mill state education tax combined). Local government services and operations vary across the diverse mix of the state’s counties, cities, villages, and townships. Services and operations range from providing public safety and parks, operating courts, conducting elections, overseeing zoning, and maintaining roads and local transit systems, to name a few.

2023 Michigan Property Tax Revenues – $18,771,362,956

Source: 2023 Ad Valorem Tax Report, Michigan Department of Treasury, ($million)

In previous efforts to address property taxation and manage public spending, voters have approved constitutional amendments that limit tax rates, levies, and property valuations. In 1978, Michigan voters approved the Headlee Amendment, which introduced restrictions on total state revenues, prevented the shift of state costs to local governments, limited the unit-wide growth of tax burdens, and required voter approval for property tax rate increases.

In 1994, voters adopted Proposal A. In addition to revamping the K-12 public school funding system, Proposal A established a cap on property assessments, cut homestead property tax rates, and raised the state sales tax rate to fund public schools. Accompanying the reforms to school finance and the cuts in local property tax revenues, the state also adopted new state-levied taxes. These new state tax revenues were dedicated to funding for local public schools.

These two landmark constitutional amendments changed the property taxation landscape in Michigan. Their application and administration of the implementing legislation is complex, and few could have anticipated the adverse impacts of some of the interactions between the provisions of these amendments.

Review Michigan’s Municipal Finance System

Given that Michigan local governments currently have few options to diversify the taxes they levy beyond the property tax, what can be done to help local governments deliver and maintain the local services their communities expect?

Evaluating operational costs and improving managerial efficiency while not raising taxes is of course an option. Cutting services with an accompanying cut in property taxes, or shifting to fees for service, is yet another option. Policymakers will be challenged by the question of which services to cut and by how much, given that communities must still fund public infrastructure and provide services for the safety, health, and welfare of their residents. And since well-run communities with good schools and other attributes attract growth and more tax revenue, local policymakers must be pragmatic.

Given Michigan’s historical experience with property tax reform, before abandoning a stable revenue source upon which local governments so extensively rely, it would be best to first evaluate the contemporary fiscal landscape and long-term impact and interactions of constitutional and statutory tax limits on municipal finance.

The interaction of the Headlee and Proposal A limitations may have resulted in unintended impacts on local governments’ fiscal circumstances. For example, in communities where strong real estate growth would have raised overall property tax revenues above the local revenue limit, tax rates were rolled back per the requirements under the Headlee Amendment. Communities did not have access to this growth in property tax revenue when properties were sold and reassessed at market value. Addressing what is not working under the property tax system, such as this issue, should be a first step.

Restore Stability to State Revenue Sharing

State Revenue Sharing payments began historically to compensate local governments for tax revenues forgone when state law changes eliminated intangible property from their property tax base. Revenue Sharing payments – a constitutional payment and a discretionary payment – also fund public services local governments deliver on behalf of the state. Local governments also receive state aid for specific programs such as roads and community health. Overall, just over 50 percent of Michigan’s state revenues are shared with local governments such as counties, cities, villages, townships, county road commissions, school districts, and community colleges.

During the upcoming Fiscal Year (FY)2025-26 budgetary debate about the amount of discretionary state revenues that will be shared with local governments, state policymakers should review the objectives of revenue sharing program, especially how its distribution formulas meet those objectives, in context of the state’s overall municipal finance system. Historically, while the state budget has appropriated local governments revenue sharing payments required by the Michigan Constitution, discretionary revenue sharing payments were reduced during recessionary periods to address state budget shortfalls. Predictable revenue sharing payments would relieve some pressure on local governments to increase property tax rates, reduce local property tax burdens, and support the delivery of public services local governments oversee on behalf of the state government.

In the January 2025 consensus revenue forecast, state forecasters expect the state’s general fund revenues to be $591.2 million higher than anticipated when the FY2025 budget was adopted last summer. In that budget, revenue sharing payments increased overall by 11.5 percent – a welcomed increase after many years of stagnant funding. However, even with this increase, FY2024-25 revenue sharing payments will not be sufficient to fully replace the funding reductions from previous years. As an extreme example, if state policymakers prioritized all of the expected revenue growth for state revenue sharing, the total funding levels would still be below the levels earmarked in the 1998 statute that set a full-funding level for state revenue sharing. To acknowledge the role local governments play in the state’s economic health, state legislators could share some of this year’s surplus revenues by increasing revenue sharing payments and help to mitigate the need to raise property tax rates at the local level to meet increasing operating costs.

Offer Local Option Taxes

Michigan law restricts the taxes available to local governments to essentially the property tax. A city income tax and several minor taxes for counties are options, but not available to all local units. With the property assessment cap restricting growth in the property tax base, and the inability to levy non-property taxes, local governments have little option than to raise property tax rates or fees to sustain revenues over time.

One option to diversify revenue sources for local governments is to authorize local governments to levy local taxes, such as a local sales, tourism-related, or fuel taxes. Currently, 24 cities levy a city income tax. Some communities levy tourism-related taxes. While there may be additional administrative burdens and jurisdictional economic disparities between communities with local-option taxes, having greater revenue-raising options could help to lower property tax burdens for residents and businesses, and capture local economic activity as well. Allowing community residents to elect to impose a local option tax also gives agency to community residents to determine the level of services they wish to fund and generate income from non-residents. While authorizing local option taxes in Michigan will require a review of the constitutional and statutory provisions for such taxes, it is an appealing option worth investigating.

Tackle Local Government Finance Reform

Balancing taxpayer tolerance for property taxes, the need to retain healthy and well-run communities, and ensuring sustainable funding for local governments is a challenging, but important, task for state and local policymakers. The fiscal stability of local governments is critical to Michigan’s economic well-being. Without alternative ways to raise revenues and lower their community’s property tax burden, local governments face significant challenges in maintaining their operations, offering the public services they are expected to provide, and growing their local economies. Looking for improvements to the property tax system to address the unintended interactions from past reforms is a great first step. Diversifying revenue sources to reduce the reliance on property taxes by stabilizing state revenue sharing payments and offering local governments alternative taxing options are policies state policymakers should pursue this legislative session.

[1] Fisher, Ronald C, and Guilfoyle, Jeffrey P., Fiscal Relations among the Federal Government, State Government, and Local Governments in Michigan.