March 24, 2026

In a Nutshell:

- Bonds issued by state and local governments are federally tax-exempt, allowing state and local governments to issue debt at lower interest rates.

- The U.S. Congress is considering including interest earned on municipal bonds in federal taxable income for investors in state and local government bonds. This change will increase the interest rates state and local governments would have to pay for their bonds, and increase costs for their taxpayers.

- Changing the federal tax treatment of municipal bonds would bring uncertainty and disruption to the bond markets, delaying planning, budgeting, and much needed investment in Michigan’s public infrastructure.

Michigan’s state and local governments are wary of proposed federal income tax changes that could increase their borrowing costs. Today, state and local governments can borrow for public infrastructure projects at lower interest rates because investment income from municipal bonds can be excluded from investors’ federal income tax bases. Bonds issued by local governments are purchased by both individuals as well as institutional investors looking for relatively safe long-term investments. Access to debt financing gives local government the resources to fund public infrastructure projects.

The looming expiration of the Tax Cuts and Jobs Act (TCJA, 2017) has reignited the debate about the federal personal income tax exemption for municipal bonds.

Federal policymakers are seeking ways to ‘pay for,’ or extend, the terms of several of the tax cuts enacted in the TCJA by eliminating certain tax provisions in addition to enacting federal spending reductions. The proposal to repeal the exemption of municipal bond income would increase federal income tax revenues, increase the interest rates paid by state and local governments on their bonds, and increase the tax burdens of their taxpayers who pay for debt service on municipal bonds.

Earlier this year, the U.S. House Ways and Means Committee released a document listing the potential options to increase federal revenue as part of the discussion on how to extend the tax cut provisions of the TCJA. The proposal to include the interest earned on state and local bonds in federal taxable income is calculated to increase federal tax revenues by $250 billion over ten years. Changing the 100-year-old federal tax expenditure that benefits both state and local governments and individuals holding municipal bonds, could disrupt public infrastructure investments and the U.S. municipal bond market overall.

Debt Financing

Debt financing, or the issuance of municipal bonds, is a crucial tool for local governments to fund infrastructure services.

Building, maintaining, and repairing local public facilities takes significant investment. State and local governments may finance the construction and maintenance of public facilities using intergovernmental grants, tax revenues, or bond proceeds from issuing long-term debt. Debt financing introduces generational equity by allowing a state or local government to construct a project and match the payment for that project to those who benefit from the project over time or generations.

In Michigan, many state and local governments issue debt to finance their major capital projects and levy dedicated property taxes to meet annual principal and interest obligations. Taxes levied for bond repayments are voter-approved and outside the traditional property tax rate limits.

State and local governments issue primarily two broad types of municipal bonds, general government bonds, which are secured by local taxes, fees, or other revenues (such as a bridge toll, for example), and private-activity bonds. General government bonds fund public infrastructure projects and comprise most of the municipal bonds issued. Private activity bonds are bonds issued by private entities that have a public purpose. Some examples of facilities funded by private activity bonds include stadiums or hospitals.

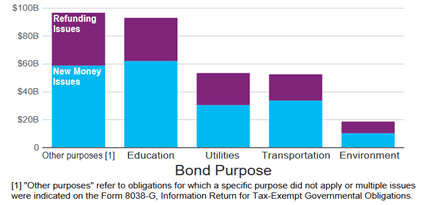

Across the U.S., there was a total of $370.6 billion in public-purpose government bonds (new money and refunding) issued in calendar year (CY)2021, according to IRS Statistics. Of this total, 76.3 percent was for municipal issues. Chart 1 shows the public purposes for which local governments issued bonds in CY2021.

Chart 1

Long-term Tax-Exempt Local Governmental Bonds

by Selected Bond Purpose and Type of Proceeds, Calendar Year 2021

Source: Internal Revenue Service, Publication 5439 (Rev. 9-2024)

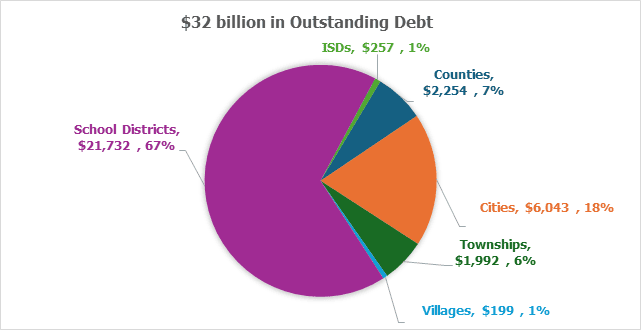

In 2024, according to the Municipal Securities Rulemaking Board, bond issuance was up 33 percent from 2023 with $450 billion in tax-exempt bonds issued nationwide. Michigan’s issuance of municipal debt totaled $7.89 billion in 2024. Chart 2 shows the current outstanding debt being held by Michigan’s local governments. School districts hold two-thirds of the total outstanding debt.

Chart 2

Michigan Local Governments, 2025

($ million)

Source, Municipal Advisory Council of Michigan, retrieved April 1, 2025)

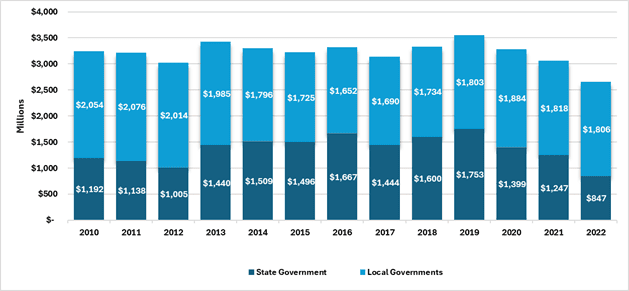

Chart 3 indicates the total interest paid on debt by the state and local governments in Michigan from 2010 to 2022. Interest payments by state and local governments vary over time during this period due to variations in the terms of the bonds and interest rates. Also, interest payments have been declining in recent years, with 2022’s payments being the lowest during the period shown.

Chart 3

Interest Paid on Michigan State and Local Government Debt, 2010-2022

Source: Census of Governments: Finance

Benefits to State and Local Governments

Income earned by municipal bond holders has been exempt from federal income tax since the adoption of the federal Revenue Act in 1913. At the time, legal experts argued that a federal tax on state and local bond interest would violate the constitutional doctrine of intergovernmental tax immunity. However, over time, the U.S. Congress has curtailed the favorable treatment of certain types of municipal bonds and several legal cases have addressed the issue of a state’s immunity from federal taxes.

In 1982, the Tax Equity and Fiscal Responsibility Act (TEFRA) required that the exemption only apply to registered municipal bonds. This change was challenged by South Carolina on the grounds that states were guaranteed the right to issue debt tax free. In South Carolina v. Baker (1988), the U.S. Supreme Court clarified that taxing the interest received by someone who owns a municipal bond was unlike taxing a state government and therefore, taxation of interest income from municipal bonds was permissible. Even with this new legal interpretation, because the role of municipal debt has become so intertwined in subsidizing public infrastructure investment, the exemption remains despite the many efforts to change it.

Economists explain that the municipal bond market exists only because of the federal tax code. The non-taxable municipal bond market provides state and local governments, as well as their taxpayers, a significant fiscal benefit – lower borrowing costs for public infrastructure projects. Because the investors who purchase government bonds receive a tax benefit on the income earned on their bonds, they are willing to accept a lower interest rate, especially if the bonds are secured by the full faith and credit of the government issuer. Should the federal income tax exemption for municipal bond income be repealed in the future, state and local governments will not benefit from a discounted interest rate. Their higher debt service costs will be passed on to taxpayers.

Given that state and local governments issue bonds primarily to pay for the important infrastructure projects on which residents depend – roads, bridges, wastewater systems, schools, and other public facilities – the repeal of the exemption will increase the costs to construct or purchase the public infrastructure and capital. If enacted, costs will rise at a time when Michigan communities need greater investment and more asset management of public facilities. Higher capital costs will be passed on to local taxpayers in the form of increased taxes.

In addition, state and local governments will have to change how they structure their bonds to compete for investors in the taxable bond market. The unique municipal bond market offers certain advantages. State and local governments tend to issue bonds infrequently and in structures or amounts that the taxable bond market does not usually see. State and local governments would be competing in a competitive market where investors expect a higher yield (since they do not receive a tax benefit) and have shorter-term maturities. Today, state and local governments issue long-term maturities for bonds allowing them to budget debt service payments for capital investments with longer lifespans over time.

Currently, in Michigan, and in other states, local governments take advantage of state programs that offer pooled borrowing. Michigan’s Local Government Loan Program, for example, assists those local governments who are infrequent bond issuers or might benefit from a program that can offer shared credit to lower the interest rate on the bonds they issue. Participation in pooled borrowing programs will probably become more popular as local governments will try to compensate for those higher rates.

Until state and local governments work through a transition period and learn to navigate the different character of the taxable bond market, overall borrowing costs, including related professional and issuance fees would increase. The Public Finance Network of the Government Finance Officers Association estimates borrowing costs will total in the billions nationwide.

There are other benefits to retaining the exemption. By relying on debt-financing, public infrastructure investments can access private capital sources. Without the exemption, there would be greater pressure on the federal government to offer more financing options and support for state and local governments infrastructure investments. Budgets, and residents’ tax appetites, for funding infrastructure are already strained at the state and local level as the need for ongoing investment in public facilities continues to grow.

Finally, public facilities projects often provide economic development and employment opportunities in communities. Building roads, wastewater systems, and healthcare facilities provides opportunities for business development, and creates employment for planners, engineers, and construction workers, among others.

Arguments For Repealing the Municipal Bond Tax Exemption

The primary reason for the proposal to eliminate the federal tax exemption on municipal bond interest income is the sizeable nature of the federal tax expenditure. The Fiscal Year (FY)2026 Tax Expenditures Estimates issued by the U.S. Department of Treasury shows that the exemption of municipal bond income ranks 16th in the list at $469 billion for the period FY 2025-2034 – just over $40 billion in 2025 alone. Other hefty tax expenditures include employer contributions to medical insurance premiums, IRA contributions, and deductions for state and local property taxes paid for owner-occupied homes. Note that several states, including Michigan, base their state income tax on federally-adjusted gross income, so these tax expenditures affect state income (and city income) tax revenues as well.

A long-standing criticism of the municipal bond income exemption has been that some tax-exempt municipal bonds benefit private entities. Municipal bonds can be used for constructing facilities such as stadiums for professional sports, entertainment venues, or other economic development projects jointly financed with private or non-profit entities. However, this concern has been addressed in the tax code. Congress moved to limit their use after noting the significant rise in issuance. The volume of these private activity bonds, which take advantage of lower interest rates through tax-exempt issues, were limited by changes first adopted in the Deficit Reduction Act of 1984. Additional restrictions on private activity bonds have also been enacted since then.

Others argue for repealing the exemption because it is a flawed federal subsidy. While state and local governments should receive the full benefit of the subsidy, they do not. Individual federal income taxpayers that earn income from municipal bonds receive part of the subsidy through their income exclusion. Also, as tax designers note, the subsidy generally benefits higher income taxpayers over lower income taxpayers, increasing the regressivity of the federal income tax.

Finally, some argue that the exemption is also an economically inefficient federal subsidy to state and local governments for their capital expenditures. They claim that a federal exemption should not be used to support state and local government financing, given that it is the local residents that benefit not all federal income taxpayers. Whether such a subsidy is an appropriate federal expenditure when there are potentially non-local beneficiaries, or whether there is an overall federal benefit to reducing infrastructure costs for state and local governments is still under debate.

Other Options to Consider

The municipal bond income exclusion has come under scrutiny – and survived several attempts to generate more federal revenue. However, changes to the exemption could be made in the future. There are some potential policy changes that could be made to reduce its fiscal impact on the federal budget. Anticipation that changes might be forthcoming only adds to the uncertainty for state and local governments and the municipal bond markets. Since neither bond markets nor governments handle uncertainty well, it is helpful to anticipate some of potential modifications that could be made to offer both revenue relief and moderate flaws in the exemption design.

First, a criticism of the policy to exempt municipal income is that the lower cost of borrowing encourages overinvestment in public infrastructure. It is tricky to measure whether that is actually the case. However, given the overall high cost and risk of funding and managing infrastructure projects, it is more likely that state and local governments would underinvest in public facilities. Lower interest costs for public infrastructure may well be a worthwhile policy to pursue through the federal income tax code if lowering costs for public infrastructure benefits taxpayers more broadly. An option could be to simply lower the amount of interest income that is exempt from federal income tax.

States could also move to change their state income tax exemptions if Congress changes the federal income tax exemption for municipal bond income. For example, since Michigan’s income tax base relies on the definition of federally adjusted gross income, the Michigan Personal Income Tax Act could be amended to add a new specific exclusion for municipal bond income earned on Michigan bonds interest income.

Second, in reaction to the past increase in private activity bonds activity, the federal tax code was amended to apply an overall cap to the volume of private activity bonds to limit the benefits to private entities. A similar volume cap could be established in the federal tax code for municipal bonds overall to reduce the total federal revenue impact of the tax expenditure.

And last, the exemption could be changed to a federal income tax credit instead of a federal income tax exemption to address the tax equity concerns that are raised by tax theorists. As an exclusion to income on the federal tax return, a higher-income taxpayer enjoys greater benefits than a taxpayer in a lower income tax bracket. An alternative would be to change the federal income tax exclusion to a tax credit, allowing taxpayers in a range of incomes to benefit, and potentially also reducing the budgetary impact of the overall tax expenditure. Changing the federal tax treatment of municipal bond income in this way would also allow for municipal bonds to retain their yield advantage in the bond marketplace.

Conclusion

Municipal bond market experts note that changing the exemption for municipal bond interest would be disruptive, for the borrowers and investors alike. Uncertainty in what could happen will make state and local governments skittish about making plans and budgeting for future near-term projects. This will delay planning and budgeting for much needed infrastructure investment in Michigan’s public facilities. And while it is fair to anticipate that a full repeal of the federal exemption is unlikely given past experience, changes may occur and push up future borrowing costs for Michigan, its local governments, and taxpayers.