December 4, 2025

In a nutshell:

- Detroit is using business tax abatement programs to spur economic development more than four of its peer cities – Cleveland, Columbus, Memphis, and Milwaukee.

- Between 2017 and 2021, Detroit averaged $31 per resident per year in property tax incentives; this compares to an average of $13.50 per resident across its four peer cities.

- Tax abatements account for 16.8 percent of the average annual property tax revenue generated between 2017 and 2021.

Introduction

Local governments utilize tax incentives to subsidize development to create jobs, grow the tax base, and generally promote economic growth. However, as with many economic development programs, it is difficult to determine how much economic growth would have occurred in the absence of the tax breaks. The foregone tax revenues from tax incentives and abatements, however, can be calculated and are reported in annual city financial reports.

The effectiveness of such programs has always been debated. Scholars and policymakers have long questioned the use of these programs. The City of Detroit has relied heavily on these programs over the years.

Earlier this year, Bedrock was granted a $60 million tax abatement for the Hudson site development. Some Detroiters were unhappy with this decision because abated taxes are dollars not available to fund vital public services. Just this week, Olympia Development requested state and city incentives for the $1.5 billion District Detroit development. Both examples highlight the city’s active role in providing developers and businesses with tax incentives.

This blog examines how much Detroit relies on tax abatement programs to spur economic development. It benchmarks Detroit to four peer cities as a way to better understand how heavily the city leans on these programs and compares the foregone revenue caused by economic development tax breaks. The objective here is to provide a high-level analysis of Detroit’s use of business tax abatements.

Our review of data from Good Jobs First, a national watchdog group and policy resource center, finds that Detroit has used more tax abatement programs than Cleveland, Columbus, Memphis, and Milwaukee. Further, Detroit’s heavy use of business tax abatements results in residents experiencing the highest per-capita foregone revenue among its peers.

Basics of Tax Abatement Programs

State and local governments across the country use tax abatement programs. Government officials waive some or all tax liability for particular parcels of land with the goal of lowering the financial burden of development projects in selected industries or geographic areas. The desired outcome is to increase the incentive for projects that might otherwise not occur to spur economic development.

These programs are an attractive option for a few reasons. First, state and local governments are able to determine the menu of tax incentives they are able to provide businesses to attract investment. This provides a level of control for taxes they choose to forego. Second, they are politically easier to implement because they do not directly require cuts or diversions in spending from other programs. Finally, it is hard for communities to abstain from using incentives when their neighbors use them to attract investment.

Detroit, like other communities with high unemployment and/or declining population, utilize these programs to capture and/or redirect business investment as a means to bolster employment and grow the population. While the city might forego tax revenues with these incentives, the businesses and jobs the city attracts serve as a benefit through increased city income tax from new jobs as well as any spin-off effects from new or improved developments.

Cities like Detroit tend to have underutilized infrastructure, so business investments in these areas are less likely to require new infrastructure that may be costly. In addition, business tax breaks are meant to partially offset the increased business costs such as higher property taxes, lower public services, and higher crime rates associated with locating in poorer areas of a city.

However, there are potential obstacles to achieving the development goals of tax abatement programs. Property taxes are a small part of total operating costs for businesses and sometimes tax breaks are provided to businesses that would have chosen the same location without incentives. The widespread use of incentives may also reduce their effectiveness. Thus, governments must be strategic in providing business tax incentives.

Tax Abatement Programs in Michigan

Michigan law offers many types of tax abatements for local governments to foster economic development. A strength of Michigan’s tax abatement landscape is the variety – abatements are available to targeted blighted areas and contaminated sites as well as high-tech investment and job creation. Michigan’s three primary tax abatement programs are Renaissance Zones, Neighborhood Enterprise Zones, and Industrial Facilities Tax Abatements.

Among the oldest and most commonly utilized tax abatement programs is the Industrial Facilities Tax (IFT) abatement program which applies to both the construction of new industrial facilities and rehabilitation of existing industrial facilities. IFT abatements encourage Michigan manufacturers to build new plants, expand existing plants, renovate aging plants, or add new machinery and equipment.

The Renaissance Zone Act authorizes targeted-zone programs for qualifying local units of government in which business and resident site-specific state and local taxes get waived for up to 15 years. Local units of government have to meet certain criteria of economic distress to qualify. The City of Detroit has 18 renaissance zones.

Neighborhood Enterprise Zones (NEZ) are similar to Renaissance Zones, however, they are exclusive to residential development and improvements. The Neighborhood Enterprise Zones program offers two types of property tax reductions in economically distressed communities which include the NEZ New and Rehabilitated (NEZ-NR) and Homestead NEZ (NEZ-H) abatements.

NEZ-NR reductions are designed to induce major investments on new or existing residential property, while the NEZ-H program is designed to provide a measure of property tax relief to current property owners. While not a business tax incentive, it is one of the more commonly used tax abatement programs in Detroit. Detroit has 52 neighborhood enterprise zones.

Detroit’s Use of Business Tax Abatements

Detroit uses many of the business tax abatement programs available under state law. Between 2017 and 2021, Detroit used 13 different residential and business programs. The table below lists the nine business-specific programs employed and the foregone revenue from each program over the five-year period.

Detroit’s Business Tax Abatements and Average Foregone Revenue, FY2017 to FY2021

| Program Name | Average Foregone Revenue per Year |

| Renaissance Zone Act | $6,867,967 |

| Eligible Manufacturing Personal Property | $4,188,766 |

| New Personal Property Exemption Act | $3,510,264 |

| Commercial Rehabilitation Act | $1,933,161 |

| Obsolete Property Rehabilitation Act | $1,821,773 |

| Brownfield Redevelopment Act | $1,116,460 |

| Industrial Facilities Tax Abatement | $560,754 |

| Brownfield Authority | $235,968 |

| Commercial Redevelopment Act | $106,239 |

| Total Average | $20,341,352 |

Source: Good Jobs First; City of Detroit

Between 2017 and 2021, the city opted to forego an average of about $20 million in property taxes per year through the business tax abatement programs. Renaissance Zones comprised the largest share ($7 million or 34 percent) of the total abated business taxes. The average annual property tax revenue generated over the same period equaled about $121 million. Thus, tax abatements account for 16.8 percent of the average annual property tax revenue generated between 2017 and 2021.

The use of these programs may help to attract jobs and investment, but it leaves the city with foregone revenue which can negatively affect public services like public safety and libraries that rely on local taxes. If the development had happened without the abatements, the city could have generated more property tax revenue which would have been used toward city services.

Comparing the Cost of Business Tax Abatements

Comparing the use of tax abatement programs across cities is difficult because of the various ways different states’ laws are structured and the particular dimensions of each program. These differences relate to the type of properties that are eligible for tax-favored treatments, the design of individual programs, and local decisions about when/where/how to employ abatement programs. Programs also differ based on the costs of lost tax revenue and elements of a program employed to ensure projects deliver promised benefits.

Four peer cities similar in size and economic conditions were selected for this comparative analysis: Cleveland, Columbus, Memphis, and Milwaukee. They were selected based on population, land area, population density, median household income, and percentage of the population below the poverty level. Columbus, Memphis, and Milwaukee, like Detroit, are considered high-tax cities when assessing effective tax rates on homestead and commercial properties.

Economic measures such as median household income and percentage of the population below the poverty level are especially important in this analysis as they are indicators of distressed jurisdictions that may be incentivized to use economic development programs.

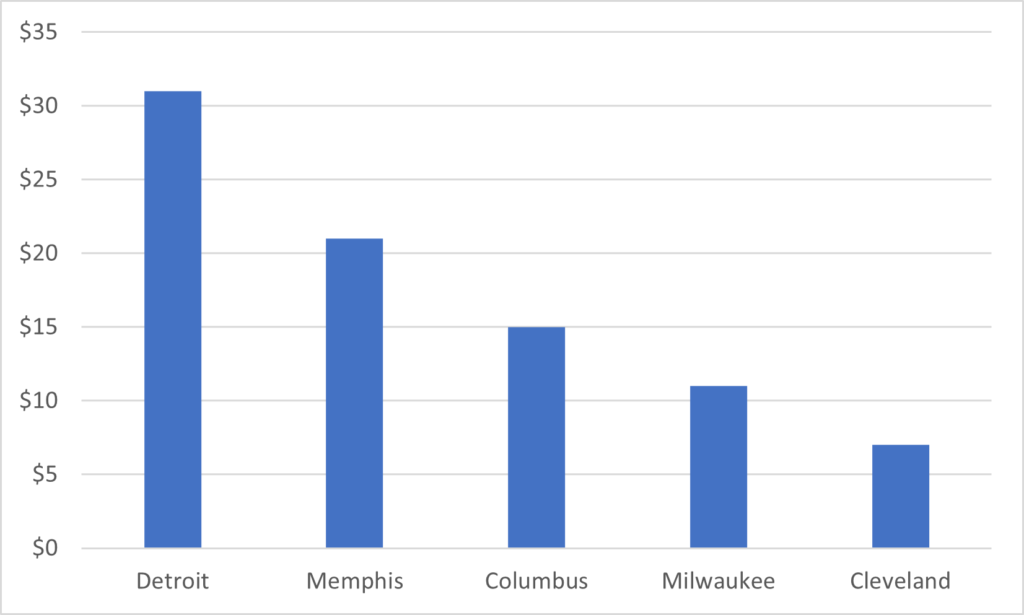

The chart below shows the average annual per-resident foregone revenue of business tax abatements across the five cities over the five-year period, FY2017 to FY2021.

Average Per Capita Foregone Revenue, FY2017 to FY2021

Source: Good Jobs First; City of Detroit; City of Cleveland; City of Columbus; City of Memphis; City of Milwaukee; U.S. Census Bureau

Comparing Detroit to its four peer cities, Detroit ranks the highest in average annual per capita foregone revenue at about $31 per resident with Memphis ranking second at about $21 per resident. The average annual per capita foregone revenue of the four peer cities was $13.50, meaning Detroit is providing more than twice the business tax incentives via tax abatements as the comparison cities.

In addition to leading the pack with forgone tax revenue, Detroit used the most (nine) business tax abatement programs compared to its four peer cities. Most others used fewer than five.

Discussion

It is important to note that when looking at these numbers, it can be hard to provide an apples-to-apples comparison of the impact tax abatement programs have on local governments based on the gross foregone revenue of each city. There are several dimensions at which tax abatement programs can differ between states and the number of programs a state makes available to its municipalities also differs.

Nevertheless, some of those differences are overcome by scaling the data using average per capita foregone revenue and counting the number of programs used. This gives a sense of which municipalities need to rely on tax incentives more for their perceived business climate disadvantages, and which cities tend to rely more on abatement programs for business development.

Detroit makes use of the options the state provides to try and bolster economic development. One of the main features of using tax abatement programs to incentivize business investment is to create and retain jobs in the city. Over the last decade, Detroit’s unemployment rate has trended down while the municipal income tax has trended up. While it is hard to quantify how much of that trend is due to the tax abatement programs the city has used, it is certainly a good sign for the city.

The verdict on tax abatement programs is still unclear. The literature shows a generally poor record of these programs promoting economic development, but incentives can be helpful in some cases. For cities like Detroit that have struggled to retain population and business, economic development tools like abatement programs were made to alleviate that.

When incentives attract new businesses to a jurisdiction they can increase income or employment, expand the tax base, and help to revitalize distressed urban areas. But these programs must be used prescriptively. Tax abatement programs tend to lose their effectiveness if used abundantly and Detroit must be aware of that as it moves forward trying to spur its economic growth.