February 7, 2024

In a nutshell:

- In Michigan, all types of local government levy property taxes to fund services. Many communities in Southeast Michigan are already levying property taxes at high rates, limiting the usefulness of the property tax as a funding source for regional transportation.

- Tax-base sharing, which is difficult in a region as diverse as Southeast Michigan, is necessary to fund regional services like public transportation that transcend political boundaries and have the potential to benefit the region as a whole.

- Many regions in other states utilize multiple taxes to support regional transportation, with a local sales tax often the primary source.

As the 2018 election season nears, it is unclear whether voters in Southeast Michigan will be asked again to support the Regional Transit Authority (RTA) with a property tax millage; a 1.2-mill property tax question was defeated in November 2016. (For purposes of property taxation in Michigan, one mill equals $1 of tax for every $1,000 of taxable value.)

Current discussions include a proposal by Wayne County Executive Warren Evans to put a 20-year, 1.5-mill transit levy before voters in the four-county region in November. This plan has the support of some elected officials in Wayne and Washtenaw counties, but the Macomb and Oakland leaders say their residents have already voted against a regional transit tax. With support lagging, talks have also included the possibility of a Wayne-Washtenaw transit plan to connect the two counties via bus service and rail lines.

Whether a proposal is submitted to voters on the 2018 ballot remains an open question. It is clear that funding regional public transportation is not easy. It is made more difficult because the RTA’s proposed funding source, the property tax, has many drawbacks.

The tax voters hate

A recent Research Council report highlights the fact that Michigan severely limits its local governments when it comes to raising local own-source revenue; most are limited to the property tax. The problem with this system is that property taxes are levied by all types of local units in Michigan, including counties, cities, villages, townships, school districts, intermediate school districts, community college districts and special authorities, as well as by the state.

The arrangement of overlapping units of government found throughout Michigan, and the resulting overlapping taxing authority, led to growing property tax burdens that ultimately sparked adoption of a number of property tax limitations. Even with those tax limitations, property tax rates in some parts of Michigan are among the highest in the nation.

The problem of overlapping taxing authorities is most acute in urban areas, such as Southeast Michigan, where many local governments, especially those closest to Detroit, are already taxing at prohibitively high rates. Two factors lead to this phenomenon.

First, local governments serving densely populated areas are often called upon to provide more services than those in rural communities. Public safety services are staffed at higher levels, refuse collection is vital, and parks provide green spaces that are more abundant away from the urban core.

Second, local units with lower-income populations, and therefore lower property values, must tax at higher rates to raise the same revenue that wealthier areas can generate at lower rates.

Michigan’s heavy reliance on property taxes can act as a disincentive to economic investment in urban areas. A cycle is created wherein those residents and businesses that can afford to leave a high-tax community do so, further lowering taxable values and requiring even higher rates to raise the same revenue as before.

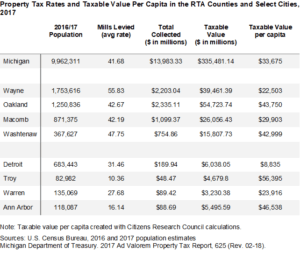

The table shows that each of the four counties in the RTA region have average property tax rates equal to or above the state average. When looking at the most populous city within each county, taxes levied range from 10 mills to over 30 (these are just for city revenues and do not include all property taxes levied on city residents by other types of local government). It is clear, especially at the city level but also in counties, that property taxes are fairly high in Southeast Michigan in general, but quite high in certain communities within it.

Tax-base sharing can be challenging

The table also highlights the major differences in taxable value per capita among communities in Southeast Michigan, which is directly related to the ability of communities to pay for services and the need for tax-base sharing to fund regional transportation. Detroit has far higher property tax rates than Troy because Detroit has less than one-fifth of the value per capita as Oakland County’s most populous city. Socioeconomic differences are not as stark at the county level, but Wayne still has about half of the taxable value per capita as Oakland.

Political leaders and some residents of Oakland and Macomb, especially those in communities farther from the urban center, argue they won’t get the benefits of the regional transportation system, and ask why they have to fund it through higher taxes, especially since many of these communities already pay the SMART millage.

The reality is that some public services and benefits go beyond political boundaries and are only possible through a regional funding model. While it is true that the direct beneficiaries of enhanced transportation services will be the actual users, others in the region also benefit indirectly. Visitors will enjoy an enhanced transportation system driving up tourism; the regional community will have expanded regional and cross-county services; residents throughout the region will be more connected to jobs; and all will benefit from any potential decrease in congestion or other benefits to road use in the region. However, it is true that not all will get the same level of benefit from expanding public transportation, even though all in the region would pay the same property tax rate for it.

The issue of tax-base sharing is further complicated by the region’s unique political and historical issues. Detroit’s population peaked in 1950 at 1.8 million residents, losing almost two-thirds of its population since. Discussions around coordinating and funding regional transportation in Southeast Michigan have been ongoing since the end of Detroit’s streetcar operations in the 1950s, but they’ve never managed to go anywhere, hampered by political, financial and racial divisions between Detroit and the suburbs, which worsened with the migration of business and capital to the suburbs.

Since 1950, Detroit has experienced decreases in city resources, increases in crime and violence, the 1967 disturbance, racial and financial tensions with its surrounding suburbs, and a municipal bankruptcy in 2013. However, before and since emerging from bankruptcy, Detroit, and certainly the downtown area, appear to be experiencing a renaissance.

Furthermore, commuting data from the U.S. Census Bureau show that from 1990 to 2013, commuters into Wayne County increased even though the population of the county decreased over the same period, which suggests that at least some jobs are moving back to the central Detroit area.

How do other states fund regional transit?

Local sales taxes are the most popular method to fund public transportation in other states. A 2003 U.S. Government Accountability Office study of the nation’s 25 largest transit systems found that 15 of these systems received dedicated sales tax funds. Data from the National Transit Database show that transit agencies and local governments levy sales taxes in support of public transit more than any other kind of local tax.

Other metro areas fund regional transportation with more than one tax. Public transportation in Chicago is funded by local sales and real estate transfer taxes; in Seattle, it’s funded by local sales, property, and other taxes. The Cleveland and Atlanta regions support transit primarily with local sales taxes.

Local governments in Michigan, however, do not have access to a local-option sales tax or many of the taxes that other states authorize. The state Constitution limits the state sales tax rate and dedicates a large portion of its revenue to purposes other than public transit; it is unclear if and how these limits would affect a local sales tax. Any attempt to allow a local sales tax in support of transit would require, at a minimum, a state law, and perhaps a constitutional amendment. This would require a statewide vote of the people, no easy task.

The RTA currently is limited to a property tax and/or a motor vehicle registration tax (which would have limited revenue raising capacity). Regional transportation in Southeast Michigan will not succeed without the funding support of a major tax (i.e., property, sales, or income taxes). But Michigan’s Constitution and governmental framework will make any such proposal a difficult journey to passage.