July 27, 2026

In a nutshell:

- Ad valorem special assessments are levied unit-wide based on property value similar to a general property tax, but are treated like a special assessment under state law.

- The use of ad valorem special assessments has grown substantially in the 36 years we have been researching this issue. They skirt the tax limitations imposed on general property taxes and create issues of fairness and equity.

- Ad valorem special assessments have become a band-aid for local governments that allows state and local officials to avoid the hard issue of the broken municipal finance system.

‘Ad valorem special assessment’ – the average Michigan taxpayer may wonder what this abstruse phrase means, but to those that live in one of the 197 local governments that levy them, along with their general and dedicated-purpose property taxes, the assessments represent a real and growing financial burden. Because of their general complexity and unique status within local government finances, few taxpayers have taken the time to gain a full understanding.

Blurred Lines

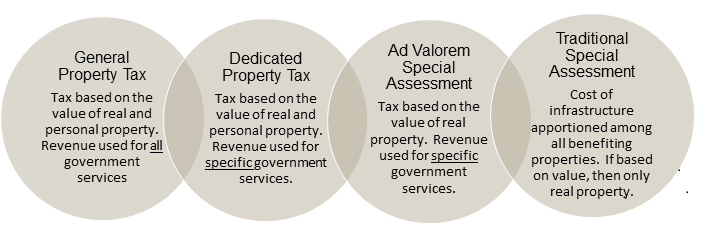

The crux of the problem, for taxpayers as well as the local governments that authorize their use, is where these unique public financing tools fit within, and how they function as part of, the constitutional and statutory framework of Michigan’s local government finance system. The graphic below illustrates where ad valorem special assessments fall on a continuum that covers general property taxes through traditional special assessments. Essentially, they are levied like a property tax, but regulated like a special assessment.

Four Types of Property Taxation

The use of ad valorem special assessments to finance local government services is technically legal, but it undermines the legal and practical distinctions that have been established between taxes and special assessments. Unlike traditional special assessments, ad valorem special assessments are generally levied to fund general government services that benefit everyone, not just those residing in a specific part of the community. The blurred lines for their use leads to confusion by both state and local officials as to how to report and track ad valorem special assessments. For example, they are not always included in a local unit’s total tax rate even though some units raise more revenue through ad valorem special assessments than they do from general property taxes. Clinton Township in Macomb County levies 5.4 mills in general property taxes and two ad valorem special assessment millages totaling 9.0 mills.

Further adding to the problem is that some, but not all, local governments are authorized to levy special assessments, which raises issues of fairness and equity. Townships and certain cities can levy them, but most cities cannot.

Ad valorem special assessments are not a recent matter that local governments and their taxpayers must contend with. The Citizens Research Council first identified ad valorem special assessments as a problem in a 1983 report that found the administration of ad valorem special assessments did not comply with the requirements of the law.

First, state law and case law require that property specially assessed receive a benefit from the improvement differing from the benefit to the general public. For most ad valorem special assessments, the linkage between property value and benefit is tenuous at best.

Second, ad valorem special assessments are often indistinguishable from general property taxes, yet they skirt the tax limitations applicable to general property taxes. Statutory tax rate limitations meant to constrain governments from creating excessive burdens have become meaningless for some levying ad valorem special assessments.

The Home Rule Cities Act limits cities to 20 mills. The City of Ecorse levies 22.3 mills for police and public safety and an additional 8.3 mills for fire protection for a total ad valorem special assessment millage rate of 30.6 mills. Ecorse had a 2020 general operating millage rate total of 38.1 mills for a total levy of 68.7 mills.

The Charter Township Act limits the tax rate to 10 mills with voter approval. Royal Oak Charter Township levies four different ad valorem special assessments for a total millage rate of 20.75 mills with a general operating rate millage total of 13.1. That means that total assessments and taxes in Royal Oak Township are 33.9 mills.

Third, special assessments are supposed to be levied on real property only, but in practice, they are levied sometimes like assessments (on all real property) and sometimes like taxes (on real and personal property). This is further complicated by the fact that some statutes authorizing ad valorem special assessments require them to be levied like property taxes and exempt property that is exempted from the general property tax (e.g., public educational institutions and nonprofit property).

Finally, inconsistent practice included ad valorem special assessments in some measures of statewide tax effort and excluded them in others.

Through clever use of nomenclature, the Legislature has accorded some units of local government a revenue raising authority that is essentially unfettered by the state Constitution.

Growing problem

The fact that we have been researching and reporting on this subject since 1983 testifies to the point that it is not a new problem. In fact, ad valorem special assessments are expanding their reach:

- In 1983, 87 ad valorem special assessment districts were identified generating at least $18.2 million in revenue statewide;

- In 1995, the total was 147 districts with at least $55.5 million in revenue;

- In 2018, that total reached 246 district levies by 192 local governments (11 percent of the 1,773 cities, villages, and townships in Michigan) with $195.2 million in revenue.

- In 2020, there were 250 special assessment district levies by 197 local units with $212.7 million in revenue.

Ninety percent of ad valorem special assessment districts were used to fund some type of public safety service and 97 percent of all revenue raised went to fund public safety services. Further, 84 percent of special assessments are levied by townships. In 43 percent of all units levying an ad valorem special assessment, the levy for special assessments was greater than the general property tax levy, showing that in many local units special assessment levies represent a significant portion of their budget.

Potential solutions

State law and policy has greatly limited the revenue options available to local governments and for many, these special assessments are one of the few tools they have left at their disposal. In this context, the increased use of the assessments in place of, and sometimes in addition to, general property taxation suggests more systemic problems facing Michigan’s municipal finance structure.

Some recommendations to curtail their use include 1) state policymakers should eliminate statutory authorization for unit-wide ad valorem special assessments; 2) local governments that rely on them to fund public safety should establish emergency service authorities, which would require local authorization and let the voters determine the millage rate limitation; and 3) state policymakers should authorize new local-option taxes and local officials should provide services more regionally.