July 28, 2026

In a Nutshell

- The Michigan Senate and House have both reserved significant funding for tax relief in their budget plans, and it seems like tax cuts in some form will be part of the final FY2023 budget agreement.

- However, Michigan is already a low-state. State tax burden has fallen signficantly after a decade-long revenue slump that began in FY2000. Further, a recent analysis ranks Michigan 46th in combined state and local tax burden.

- Policymakers should carefully weigh the budget tradeoffs that will be needed in implementing tax cuts, and ensure that there is a clear understanding of any budget reductions that will be necessitated by related revenue losses.

The Michigan House and Senate are moving Fiscal Year (FY)2023 state budget bills through their respective chambers this week, setting the stage for final budget deliberations with the Whitmer administration after state revenue estimates are finalized on May 20.

The spending plans in both chambers have one thing in common: they both leave room for a healthy amount of tax relief for Michigan residents. The Senate’s budget proposal specifically appropriates funding to a Senate Tax Cut Fund signaling its intent to implement $1 billion in permanent annual tax relief and another $1 billion in one-time relief for FY2023. In the same vein, the House budget plan also holds back $1 billion for tax relief. Both chambers lean heavier on tax relief than Governor Whitmer’s budget proposal, which proposed an expanded Earned Income Tax Credit and the gradual repeal of 2012 tax changes that reduced exemptions for certain retirement income. Those proposals are expected to reduce state tax collections by around $770 million by FY2025.

Clearly, finalizing the details on what taxes are cut, by how much, and for whose benefit will be a major agenda item as the legislature and administration work to finalize the FY2023 budget before everyone sets out for the campaign trail leading to the November election. But while election year tax cuts are popular with voters, we have noted previously that Michigan is just now climbing out of a decade-long slump in state revenues that significantly reduced state service delivery, cut state employment by over 20 percent, and resulted in major budget reductions in areas like higher education and state revenue sharing.

Should the top priority for billions of dollars in revenue reserves be tax relief or increased public investments for things like infrastructure, education, or public health? As budget deliberations move forward, here are three things that policymakers – and the public – should keep in mind as they deliberate on the appropriate level of tax relief.

1. Michigan is a Low-Tax State

It is said that nothing is certain in life except death and taxes, and few look forward to sending in their tax payments each April 15. But, contrary to what many may think, Michiganders actually have it relatively good when it comes to their tax burdens.

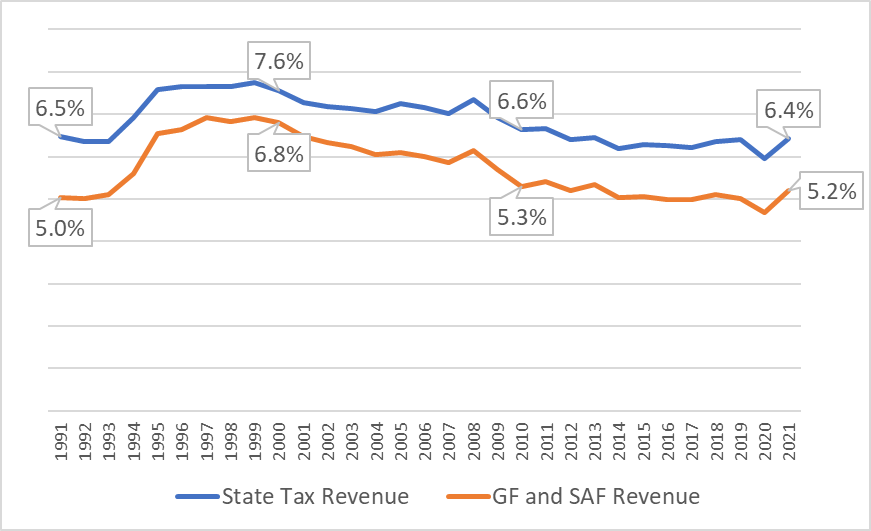

Michigan’s tax burden has fallen rather sharply since the beginning of this century. The chart below examines state tax collections as a percentage of Michigan personal income back to 1991. In 1994, Michigan voters approved Proposal A, which increased the rates of the state sales and use taxes from 4 percent to 6 percent and triggered other tax changes as part of broad reforms to K-12 school financing. As a result, the state tax burden shot up significantly in the mid-1990s. Since 2000, however, the state tax burden has been falling. For FY2021, state tax revenue collections equated to 6.4 percent of personal income, just below the rate in FY1991 prior to Proposal A.

State Revenue Collections as a Percent of Michigan Personal Income

Source: Historical data from Senate Fiscal Agency; FY2021 data from Michigan Comprehensive Annual Financial Report and January 2022 Consensus Revenue Estimating Conference Executive Summary

Similarly, revenue to the General Fund and School Aid Fund – the state’s two major discretionary revenue funds that dominate annual budget deliberations – fell from 6.8 percent of state personal income in FY2000 to 5.2 percent in FY2021. In short, while it may not feel like it, state government takes a smaller bite out of the average Michigander’s paycheck than it did 20 years ago.

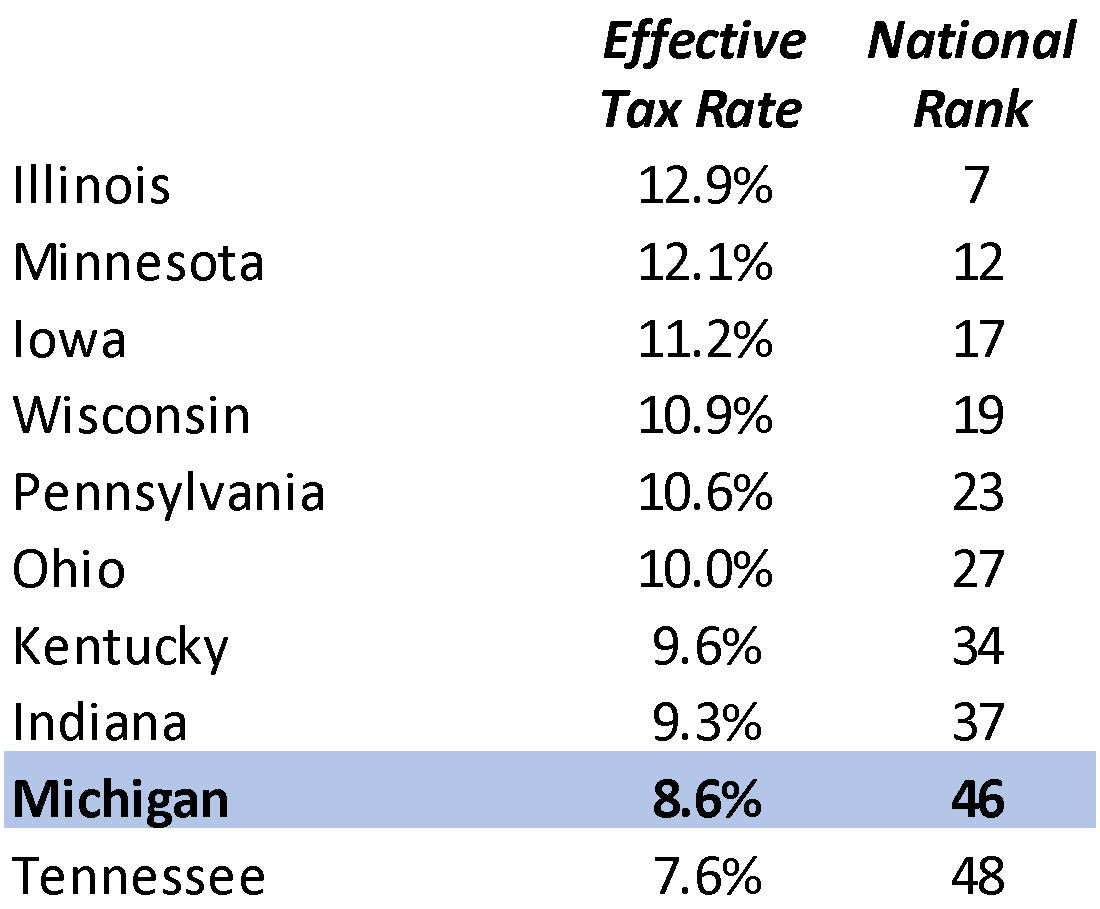

Further, Michigan’s overall tax burden is relatively low compared to the other 49 states. A recent report from the Tax Foundation, a non-profit think tank, found that Michigan’s combined state and local tax burden ranked 46th among the 50 states. The table below compares Michigan’s effective state and local tax rate (defined as total state and local tax collections as a percent of the state’s share of net national product) to that of its closest neighbors. The effective tax rate in Michigan falls below the rate in eight of these states. Only Tennessee residents have a lower state and local effective tax rate.

State and Local Tax Burden – Michigan and Neighboring States

Source: Tax Foundation, State and Local Tax Burdens, Calendar Year 2022. Effective tax rate reflects state and local tax collections as a percentage of the state’s share of net national product.

2. State Tax Cuts Don’t Result in Economic Stimulus

Like the rest of the country, Michigan is facing economic challenges related to lingering employment declines arising from the COVID-19 pandemic; the impacts of abnormally high inflation on family budgets, and economic uncertainties internationally with the war in Ukraine. Many see tax relief as a timely way to stimulate the economy and put money back into the pockets of Michigan residents.

However, on the whole, state tax cuts don’t generate any net boost to the state’s economy. That’s because Michigan’s constitution mandates that the state enact a balanced budget that brings spending in line with available revenue. To be sure, tax cuts increase disposable income for affected households, and at least some of that added disposable income gets spent. That spending creates new income for others (e.g. workers at the local grocery store or restaurant), and the economic ripple effect of a tax cut does indeed generate new economic activity from taxpayers.

However, without any tax cut, that same revenue would still get spent. Only in this scenario, it gets spent on public services financed by the state. This spending includes payments to health care providers for Medicaid-funded services; grants to K-12 school districts, universities, and community colleges for educational activities; revenue sharing to local governments; and of course paychecks to state employees. This public sector spending brings the same economic ripple effect as the tax cuts. In short, a $1 million tax cut adds $1 million in disposable income for taxpayers but at the same time eliminates $1 million in income for persons who would otherwise have been delivering public services, whether they be state employees, school/university employees, or state contractors.

Note that the story is very different at the federal level. As we showed last year, federal stimulus related to the COVID-19 pandemic (e.g., tax refund checks, enhanced unemployment benefits, Paycheck Protection Program) provided a huge short-term boost to Michigan personal income, which in 2020 grew at the highest rate in over three decades. That boost was realized because, with no balanced budget requirements, the federal government could increase spending and implement tax relief at the same time; financing the resulting budget deficit by borrowing. Most economists agree that persistent deficits bring their own challenges in the long run, but deficit spending can and has been used to stimulate the economy.

That’s not allowed in Michigan, though, which negates any net economic impact of state tax cuts here.

3. Tax Cuts Come with Budget Tradeoffs

When the Michigan Legislature approved a plan in March that would have cut state income tax revenue by $2.5 billion annually, Governor Whitmer vetoed the bill calling it “fiscally irresponsible”. Our March analysis of the legislative plan illustrated her concerns. It showed that one-time revenue surpluses were sufficient to cover the resulting revenue loss in FY2023, but that the plan would require a permanent $1.3 billion cut to the state’s General Fund budget starting in FY2024. That equates to roughly 10 percent of all current General Fund spending.

As tax relief discussions are revived, budget writers – and the general public – should have a clear view of how any resulting budget shortfalls will be addressed before decisions are finalized on an amount. To be clear, state taxes should be no higher than they need to be. Our tax system should generate sufficient revenue to provide necessary public services in an efficient and effective manner. If the state is providing services that aren’t necessary, then those services can properly be eliminated allowing revenue savings to be returned to taxpayers. The challenge is that what constitutes a “necessary public service” is inherently shaped by one’s ideological and political views.

It seems highly likely that tax relief in some form will be a significant component of the final budget agreement that should be reached sometime before the July 4 holiday. Optimally, the agreement on tax relief will recognize Michigan’s recent revenue history and be transparent about budget tradeoffs that are required.