July 27, 2026

In a Nutshell

- Weeks after Governor Whitmer proposed two major tax policy changes within her FY2023 budget recommendation, the state legislature passed its own tax relief plan that includes a reduction of the state income tax rate to 3.9 percent.

- While both the legislative proposal and the Governor’s broader budget and tax recommendations can be supported by drawing down a large General Fund surplus in FY2022 and FY2023, the legislative plan would create a $1.3 billion budget cliff in FY2024; one that would likely require a 10 percent reduction in state General Fund spending.

- Before enacting any tax relief legislation, the Governor and legislature should assess the budget tradeoffs linked to the related revenue loss and come to an agreement on how much tax relief is feasible given those tradeoffs.

Last month, Governor Whitmer released her Fiscal Year (FY)2023 budget proposal, which included two significant tax relief proposals that would undo major tax policy changes enacted in 2011; changes that were meant to raise additional state revenue to offset revenue losses tied to a broader plan to restructure the state’s business.

The proposal would restore the more favorable income tax treatment for retirement income that existed before the 2011 changes. Further, she proposed to restore the state’s Earned Income Tax Credit back to the pre-2011 level.

Just weeks after her budget was introduced, though, the state legislature approved legislation that would bring significantly more tax relief. It provides not only more immediate tax relief for retirement income, but also a reduction in the state’s income tax rate and a new child tax credit. That bill is currently sitting on the Governor’s desk, but she has already called the legislation “fiscally irresponsible” and “unsustainable”. A veto appears to be in the offing.

Is the Governor right about the “sustainability” of the legislative plan?

That answer depends on your definition of “sustainability”. All budget proposals – whether they involve spending or revenue changes – are invariably about tradeoffs. Spending more on “this” means we no longer have resources to spend more on “that”.

The key question for policymakers is this: how much are we willing to give up in state spending to live within our means with lower revenue? Below we take a deeper look at the long-term sustainability and trade-offs inherent in both proposals. As we’ll see, the legislative proposal does indeed come with a much higher price tag.

Governor’s Proposal: Retirement Income and the EITC

Then-Governor Rick Snyder and the legislature approved comprehensive tax policy reforms in 2011 that restructured the taxation of Michigan businesses by eliminating the Michigan Business Tax and replacing it with a new corporate income tax that applied to a far smaller subset of Michigan business entities. To help replace some of the revenue loss, two other tax policy changes were also enacted.

First, the income tax exemption of retirement income from public pensions was eliminated for retirees born after 1945, as were generous deductions for certain private retirement income. Those favorable provisions were replaced with a smaller general deduction applicable to all income; but for the affected retirees, that deduction only becomes available once the retiree reaches 67 years of age. In short, the income tax burden on retirement income has gone up significantly for most senior Michiganders.

Second, the 2011 changes reduced the state’s Earned Income Tax Credit (EITC) available to lower-income, working households. The state credit had been pegged at 20 percent of the related federal EITC but was reduced to 6 percent of the federal credit in 2011.

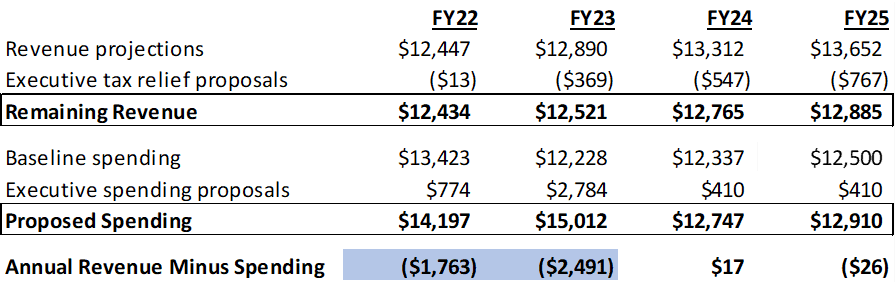

Governor Whitmer’s tax plan would do two things. First, it phases out the 2011 changes to the treatment of retirement income between tax years 2022 and 2025. By tax year 2025, all retirees in Michigan will be able to utilize the “old rules” to determine their income tax liability. Second, the state EITC would revert back to 20 percent of the federal credit starting in tax year 2022.

The table below outlines the long-run impact of the Governor’s plan on the General Fund/General Purpose (GF/GP) budget. The table adjusts current revenue projections for the impact of the Governor’s tax proposals. It also takes “baseline” state spending (current appropriations adjusted for known cost pressures such as Medicaid and social services caseloads and state employee payroll) and adds in the new spending proposals included in her Executive Budget request.

Long-Term GF/GP Impact of Governor’s Budget Proposal

(millions of $)

Source: State Budget Office analysis of Governor’s tax proposals; Senate Fiscal Agency analysis of FY23 Executive Budget. Note: Baseline spending in FY2022 includes significant one-time appropriations that are not continued in FY2023.

The table shows that GF/GP spending under the Governor’s proposal would exceed available revenues by around $4.2 billion across FY2022 and FY2023 (shaded in blue). That’s largely driven by the substantial one-time spending proposals included in her February budget request. That $4.2 billion is paid for by using a massive GF/GP surplus arising from surprisingly strong revenue growth.

Beyond FY2023, ongoing revenue and spending are nearly equivalent, so the budget remains structurally balanced. The Governor effectively pays for her tax relief by foregoing more generous GF/GP budget increases that would otherwise have been available in those future years. Under her plan, the state would be back to “continuation budgets” by FY2024 where any new spending initiatives would have to come from reductions somewhere else.

Legislature Pushes For More Tax Relief

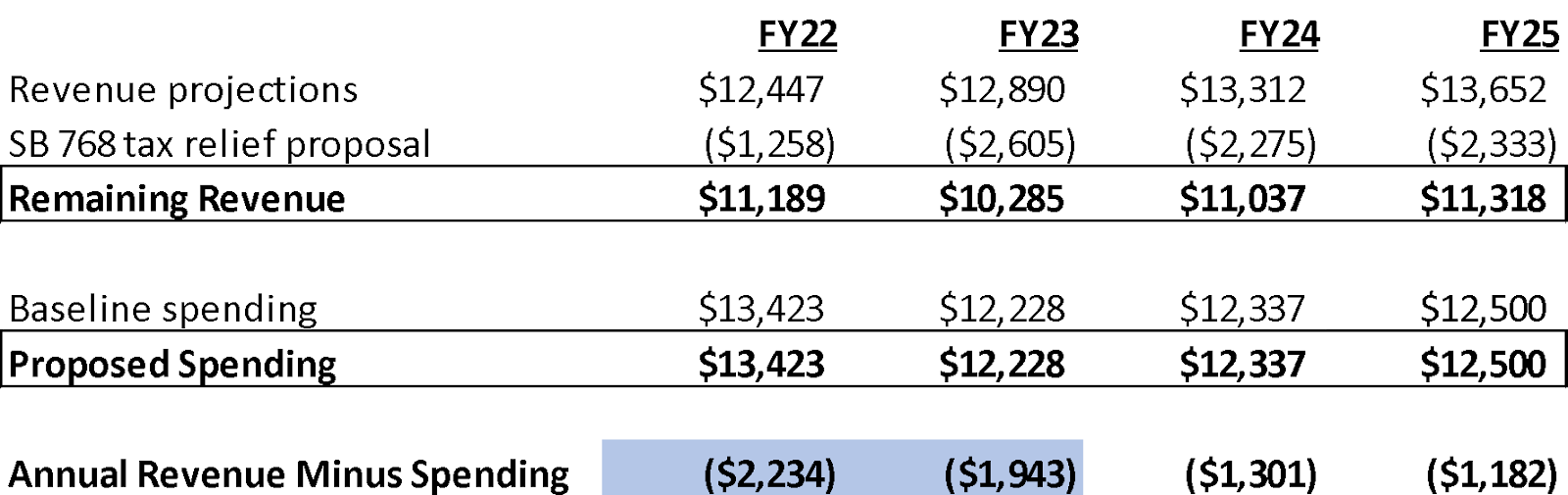

The fiscal tradeoffs are significantly larger with the legislature’s tax relief plan approved on March 3. That plan reverses some of the 2011 changes related to retirement income, but also reduces the income tax rate for all Michigan taxpayers. The bill’s key provisions include:

- Reducing the state’s income tax rate from 4.25 percent to 3.9 percent starting in tax year 2022

- Expanding the current income deduction for retirees and allowing retirees to access that deduction starting at age 62 (rather than 67 under current law)

- Creating a new non-refundable child tax credit of $500 per qualified dependent starting in tax year 2022

The inclusion of the general income tax rate cut and child tax credit mean the revenue impacts of the legislature’s plan are much greater than the Governor’s. Estimates from the legislative fiscal agencies suggest the plan would reduce annual GF/GP revenue by around $2.3 billion going forward.

Across FY2022 and FY2023, the tax plan would reduce GF/GP revenue by a combined $3.9 billion, driving revenues significantly below even baseline spending levels. Those deficits can be covered by the same $4.2 billion GF/GP revenue surplus that pays for the Governor’s one-time spending proposals, but it also means that the state could no longer afford any of the Governor’s new spending proposals. Any spending enhancements the legislature favored would have to come out of cuts to other areas of the state budget. If the legislature is willing to forego any net spending increases, however, the table shows the bottom line impact of their plan in FY2022 and FY2023 is virtually the same as the Governor’s.

Long-Term GF/GP Impact of Legislative Tax Bill

(millions of $)

Source: Senate Fiscal Agency analyses. Note: Baseline spending in FY2022 includes significant one-time appropriations that are not continued in FY2023.

The critical difference between the Legislature’s tax relief plan and the Governor’s budget proposal doesn’t show itself until FY2024. Under the Governor’s plan, about $2.4 billion in one-time GF/GP spending in FY2023 goes away in FY2024; that brings spending back in line with projected revenue. The legislature’s tax relief plan, however, aims to provide greater long-term tax relief for Michiganders. As such, revenue remains down in FY2024 and all subsequent years.

The result: projected GF/GP revenue falls roughly $1.3 billion short of baseline state spending in FY2024. When the Governor calls the legislature’s plan “unsustainable”, this is what she means. To keep the budget balanced in FY2024, the legislature’s tax plan would require $1.3 billion in a combination of either permanent state spending cuts or offsetting revenue increases from some other source .

But cutting the income tax liability of Michigan residents, only to turn around and pay for that tax relief by raising taxes elsewhere doesn’t appear to be on anyone’s “to-do” list. It seems likely then that structural balance would need to be achieved largely through budget cuts.

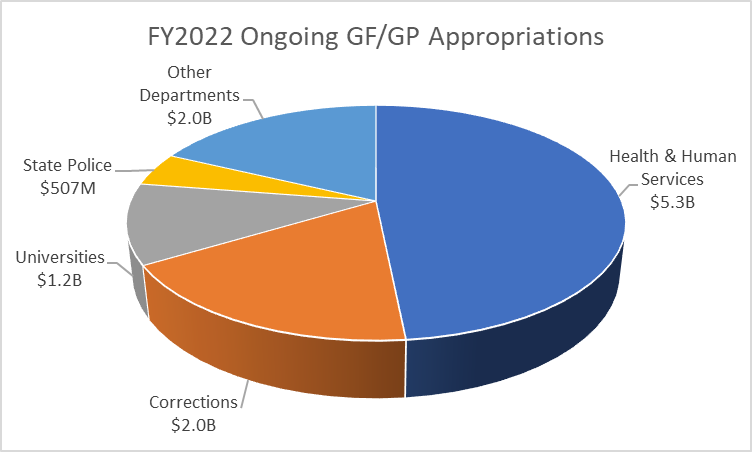

Cutting $1.3 billion from existing GF/GP spending won’t be an easy task, however. That’s equivalent to just over 10 percent of all baseline GF/GP spending. Further, the chart below highlights that over 80 percent of this spending is focused in four areas: Health & Human Services, Corrections, Higher Education, and State Police.

Source: State Budget Office, FY2023 Executive Budget Book

So, is the legislature’s tax plan sustainable beyond FY2023? In short, yes – if legislators can identify future state spending reductions necessary to live within the reduced revenue levels. But lawmakers should be both clear-eyed and transparent regarding the budget tradeoffs that their plan brings to bear. Enacting tax relief without any consideration of its long-term budget implications is short-sighted and another example of kicking the proverbial budget can down the road.

We should do better than that. Tax cuts are politically popular and easy to enact; but responsible budgeting means tax policy cannot be done in a vacuum. Before enacting any tax legislation, the Governor and legislature should come to an agreement on the parameters of any tax relief, and that agreement should be based on a realistic assessment of the feasibility of the kind of program reductions or eliminations that would result. Such an agreement would require compromise from both sides but also avoid future budget surprises.