February 7, 2024

In a nutshell:

- The local government fiscal structure is plagued by a number of problems; chief among them is inefficiency that results from the fact that the majority of services are delivered at the most local level of government (i.e., city and township).

- More local government services should be delivered at the regional (e.g., county) government level.

- Diversifying the local government tax menu, especially for regional government entities, is a key step to changing how services are delivered and financed.

The Citizens Research Council of Michigan’s new report, Diversifying Local Source Revenue Options in Michigan, highlights the need for local governments to start thinking regionally in terms of service delivery and financing. This report builds upon a previous report, Counties in Michigan: An Exercise in Regional Government, which examines the predominant local government service delivery model and calls for a system redesign to enhance the role of counties in providing services on behalf of constituent local governments.

Need Regional Governments to Deliver Local Services

A big problem with the current local government service delivery model is that most services are provided at the most local level – city, village, and township. This means that over 1,700 cities, villages, and townships across the state provide duplicative and overlapping services; 83 counties provide additional services on top of this. Given modern methods of transportation and communication, this is not the most efficient system to deliver local services.

The Research Council has identified a number of local government service areas that could benefit from county provision in some form, but the first step is to build up the information technology infrastructure to connect county governments with the cities, villages, and townships within them. Greater connectedness would position the counties to offer file sharing and develop resources to capitalize on advances in communications. This would enable counties to provide many back office functions on behalf of cities, villages, and townships, including such things as tax collection, elections, property assessing, maintenance of roads currently under city and village jurisdiction, and aspects of planning and land use. County sheriffs can assume responsibilities for policing communities or provide services to support municipal police and fire departments.

Handing over some of these services, or at least some aspects of the services, to the county could free the most local level of government to focus their efforts on developing the identity and place making that will attract people and businesses to their communities. However, conceptualizing changes to local government service delivery methods cannot happen in a vacuum and some alteration to county governance and the local government revenue structure may be necessary. First, counties could benefit by modernizing their governance structures and by changing the culture of counties from stand-alone governments to multi-purpose function providers for their local units of government. Strong county leadership (i.e., governance) will be needed to do this.

Second, counties will require more funding to carry out these changes. This realignment of local government service delivery can and should be done in conjunction with local revenue and tax restructuring. Providing services and raising taxes at the regional level can address a lot of concerns around local government service delivery and local-option taxes.

Need to Diversify Local Revenue Sources

The local government revenue structure has not been able to meet local government revenue needs in recent years. Current local government revenues – local property tax and state revenue sharing – are largely disconnected from the local economy. The local property tax captures only a narrow segment of economic growth and the economic recovery evident with bustling downtowns and job growth does not translate into growing revenue streams for local governments. State revenue sharing was supposed to capture that economic growth and share it with local governments, but the state regularly diverts revenue sharing payments to meet its own budget needs. Local communities need more mechanisms to allow them to capture the economic activity taking place within their boundaries. Some local communities with prohibitively high property tax rates need mechanisms to allow them to lower the property tax burdens on their residents.

Many states afford their local units of government a number of tax options – general and selective sales, income, transportation, “sin,” and tourism – to capture economic activity and create diverse revenue streams.

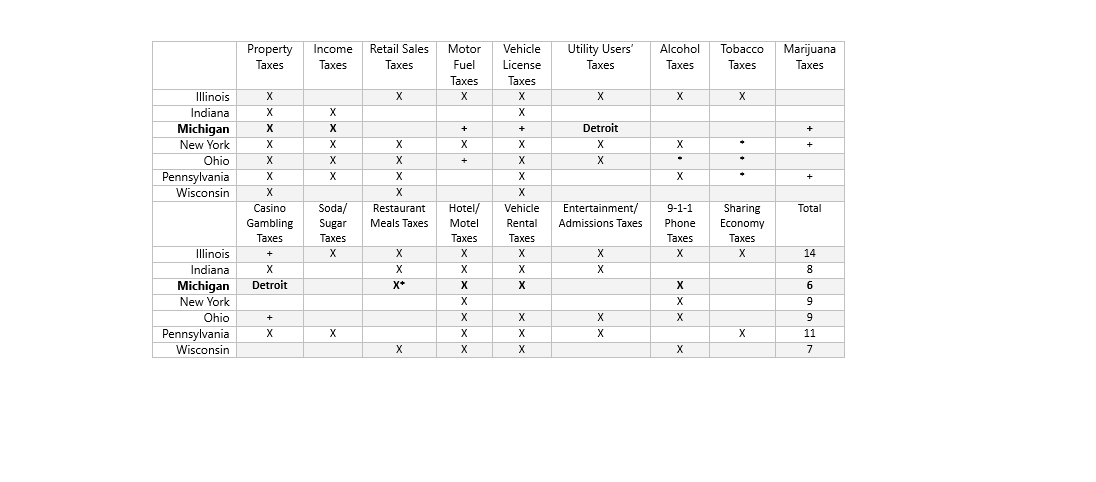

The table below compares local-option taxes in Michigan with its neighboring Great Lakes states. Michigan authorizes fewer local-option taxes than any other Great Lakes state. Only 23 Michigan cities levy a city income tax, and some select counties and cities levy tourism-related taxes, including hotel/motel and vehicle rental taxes. Detroit is authorized to levy additional local-option utility users and casino gambling taxes.

Local-Option Taxes Authorized in the Great Lakes States

* Question of constitutionality

+ State taxes shared with local units of government

Note: This table highlights which states allow at least some local units to levy a tax – does not mean that all types of local units within state can levy the tax.

Expanding access to local-option taxes in Michigan requires the state to authorize local units of government to levy additional types of taxes. It does not require local units to actually levy them. Expansion would simply provide more options for local officials. No new local tax could be imposed without local voter approval.

The question then becomes which level of government should be authorized to levy new local taxes. Local-option taxes may be best suited to the regional, or county, level of government. Authorizing local-option taxes to cities, villages, and townships would create confusion for taxpayers, could cause economic distortions, and would do more to help relatively healthy governments than struggling cities. Regional local taxes could help to ease administrative difficulties, lessen economic distortions, and minimize socioeconomic disparities.

The Future of Local Government is the Region

Moving forward, the discussion needs to continue on regional tax base sharing, regional services, and regional governance. Michigan’s economic challenges throughout much of the 2000s brought home the need to do local government differently. Local governments cannot rely on state revenue sharing during fiscal downturns and need access to more local-option taxes; however, local governments also need to reevaluate how services are provided and how things can be done more effectively and efficiently.