March 24, 2026

In a Nutshell:

- Special education services are funded by intermediate school districts primarily with dedicated property tax revenues, the amounts of which vary considerably.

- The State of Michigan provides financial aid to low-wealth districts to help equalize their tax base and augment the revenue generated by these dedicated taxes.

- A new $34 million appropriation provides intermediate school districts with supplemental payments that would work at cross purposes with existing state efforts to equalize funding for students with disabilities across the state.

When they return from their summer recess later this week, Michigan lawmakers will be eyeing a September 30 deadline to complete action on the state’s Fiscal Year 2021-22 (FY2022) budget before the new fiscal year begins on October 1. While major portions of the state’s spending plan for next year remain unresolved, Lansing officials were able to finish work on the K-12 education budget in July, well in advance of the start of the new school year.

The nearly $17 billion FY2022 School Aid Budget enacted in mid-July includes increased state funding for students with disabilities, some of the students most adversely affected by the current pandemic and the subsequent switch to remote/hybrid learning models. Notably, the final budget includes a $44 million increase in special education cost reimbursements (existing appropriation) as well as a new appropriation line item ($34.2 million) intended to further equalize local special education millage levies across the 56 intermediate school districts (ISDs).

Few observers of Michigan’s special education financing system would argue that the current design is equitable. Study after study has revealed persistent and growing inequities in the amount of funding that students with disabilities have access to, largely because of the ISD in which they live. That is why state efforts to reduce per-pupil funding disparities, whether through millage equalization or other mechanisms, are needed. In this light, the additional $34 million added to the School Aid Budget should be welcomed news.

However, instead of working to reduce per-pupil revenue disparities across the state, the new ISD appropriation will actually exacerbate existing inequities by providing the same, or greater, amount of per-pupil state funding to ISDs that already capture more in per-pupil local taxes. By doing so, the new appropriation works at cross-purposes with existing state efforts to ensure a more level per-pupil funding environment. More troubling is the fact that the new state funding will likely contribute to greater funding disparities among students with disabilities.

Doubling Down on ISD Millage Equalization

When Michigan policymakers created a new school funding model in the mid-1990s, they largely concentrated their reforms on general operations funding. One key reform of 1994’s Proposal A school funding system was a reduction in local property taxes to support K-12 education in exchange for a greater reliance on state-level taxes (i.e., sales, income, tobacco). However, these property tax reforms did not impact the financing of special education services or school capital improvements. Instead, these services continue to be financed by locally-approved property tax levies. As was the case for general operations funding prior to Proposal A, communities with more property wealth are able to generate substantial tax sums to support special education, some at very low tax rates.

Because of the continuing large role played by property taxes (they account for almost one-third of total special education spending annually) and the significant differences in property wealth across the state, the amount of locally-generated special education funding generated by ISDs varies substantially. The yield from a one-mill special education tax levy across each of the 56 ISD taxing jurisdictions varies from $663 per student in the Charlevoix-Emmet ISD (highest) to $157 per student in Wayne County RESA (lowest). These property wealth variances are amplified by the fact that districts tax themselves at different rates (they are capped by state law). Factoring in tax rate differentials, the special education millages yield varies from $2,053 per student in Huron ISD (highest) to $188 per student in Lapeer ISD (lowest).

The state appropriates $40 million to mitigate the wide differences in per-pupil revenue that arise from property wealth/rate disparities. For the current year, the state funds only equalize ISD tax bases up to $215,900 taxable value per student, well below the statewide average of nearly $275,000 taxable value per student. With this limited funding, only 16 ISDs (those generating around $200, or less, per student per mill levied) qualified for the state aid. Further, the large number of students and low property wealth of Wayne RESA results in it receiving more than 60 percent of the funds each year.

In an apparent attempt to further the state’s tax base equalization efforts, the FY2022 School Aid Budget includes an additional $34.2 million. This new appropriation comes on top of the existing $40 million appropriation, basically doubling down on the state’s assistance to help those ISD’s that generate the least amount of tax revenue from their special education levies.

Here’s the Rub

Instead of adding the new funding to the existing millage equalization formula in Section 56(2) of the State School Aid Act, lawmakers crafted a different formula as part of Section 56(7). The design of that formula, however, results in funding allocations that DO NOT equalize per-pupil revenue disparities and works at cross purposes with the existing formula. The new formula provides the same amount, or greater, state per-pupil funding to those ISDs that already generate greater amounts of per-pupil revenues from their ISD millages.1 The table below provides estimated allocations under the new formula for four ISDs that will receive Section 56(7) funding, highlighting the per-pupil funding inequities that result from the design of the formula.2

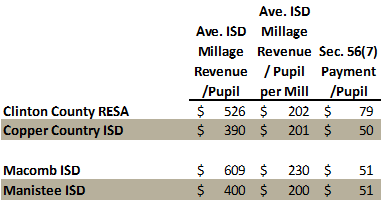

Estimated Section 56(7) Allocations for FY2022

In the first instance, Clinton County RESA already generates one-third more in local ISD millage revenue per pupil ($526) than Copper Country ISD ($390). This difference is explained, in part, by Clinton’s higher tax effort; Clinton County RESA levies 2.6 mills while Copper Country levies 1.9 mills. Scaling the levies on a per-mill basis reveals that both ISDs generate basically the same revenue per pupil – $202. However, because of the way that the new Section 56(7) is structured, the formula provides Clinton County RESA with a much larger per-pupil allocation ($79) than Copper Country ISD ($50). Clinton’s per-pupil funding advantage is amplified by the additional state aid.

A similar result can be seen when comparing Macomb ISD and Manistee ISD allocations under the new formula. Here Macomb ISD, despite generating substantially more money per pupil both in the aggregate ($609) and on a per-mill basis ($230), will receive the same amount of state funding ($51) as Manistee ISD. Despite Macomb’s ability to generate more local revenue from its special education millage (both because of its greater property wealth and its higher tax effort) Section 56(7) will provide it with the same per-pupil funding as Manistee. In the end, the new formula does nothing to better equalize the per-pupil funding differentials arising from the two ISD tax levies.

Michigan policymakers should be applauded for bringing attention to the long-standing per-pupil funding inequities across the state. The education of students with disabilities doesn’t always receive the public policy attention it deserves. This has often been the case during the current global pandemic. Even more. However, the new program funded in the FY2022 School Aid Budget fails to address inequities associated with the reliance on ISD millages to fund special education services to students with disabilities. As we have highlighted here, it actually works at cross purposes with existing, long-term efforts to “equalize” local special education millages and reduce per-pupil funding gaps. It is unclear what policy objective the new $34 million appropriation is seeking to achieve.

Footnotes:

- The Section 56(7) allocation formula has two equalization “tiers” based on the three-year average per-pupil revenue generated per-mill via the ISD special education millage; 1) an ISD generating less than $251 per-pupil provided that the district is levying at least 46.2 percent but less than 60 percent of its maximum millage rate, and 2) an ISD generating less than $281 per-pupil provided that the district is levying at least 60 percent of its maximum millage rate. The primary flaw, from an equalization perspective, is the fact that districts in the “higher” tier are already generating more local revenue than those in the “lower” tier. Any state equalization payment to these “higher” tier districts will exacerbate existing per-pupil revenue inequities.

- We also note that Wayne RESA, the largest ISD in the state, would be prohibited from receiving any payments under new Section 56(7) because of an existing statutory limitation placed on the total amount of state millage equalization funding the district is allowed to receive (Section 56(5)). We understand that this was not the intent of the Michigan Legislature, but, nonetheless, it is a controlling statutory provision.

Permission to reprint this blog post in whole or in part is hereby granted, provided that the Citizens Research Council of Michigan is properly cited.