July 6, 2026

In a nutshell:

- Twenty-four Michigan cities levy an income tax, which supplements property tax and state revenue sharing and, on average, produces one-third of general-fund revenue.

- In a recession like the one we’re in now, income-tax revenues will fall (as unemployment rises), which will have an impact on local services.

- Idiosyncrasies of the city income tax and municipal finances mean that the COVID-19 recession will cause starker revenue losses and budget implications for cities than the state income tax will for the state.

The 2020 COVID-19 recession touches people and institutions alike, and local governments are no exception. They are incurring new costs – as operations change to keep workers and the public safe – while revenues decline, related to reductions in economic activity. While property taxes remain stable in the near term, city income tax revenues are another matter entirely.

About the tax

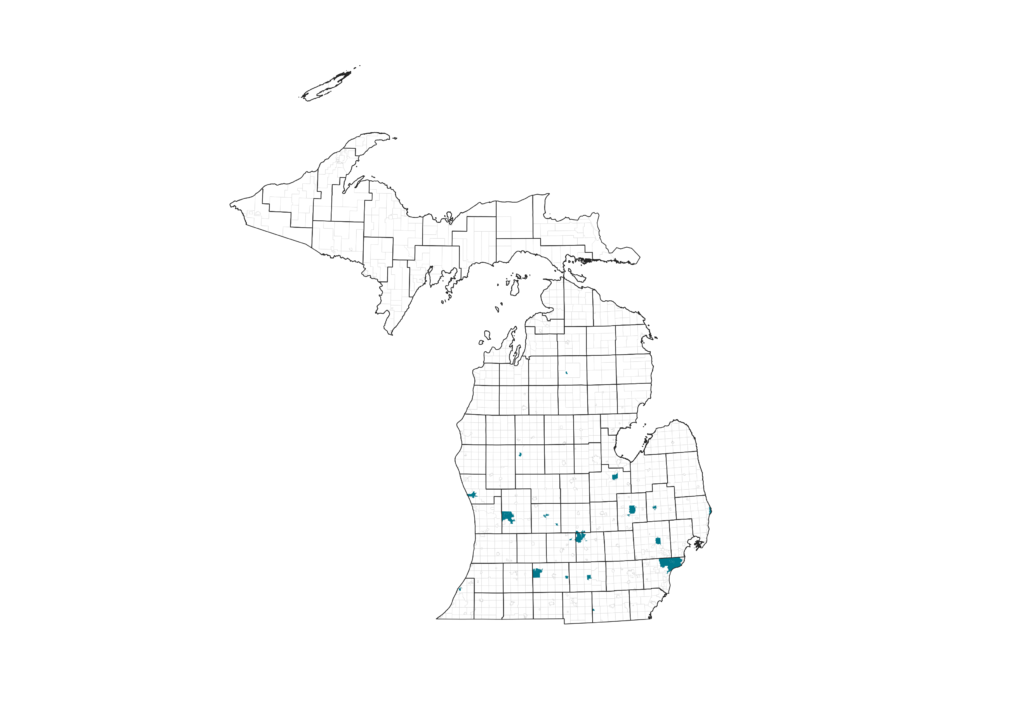

Any one of Michigan’s 276 cities may levy an income tax, under an ordinance approved by a city’s legislative body and with voter approval. The map below highlights the 24 cities that currently levy an income tax; they range in size from very small (Hudson) to the state’s largest city (Detroit). Fifteen percent of the population lives in a city that levies the tax.

The tax is a direct tax on income for residents, including salaries, net profits, investments, and other income.

For nonresidents, it is a direct tax on earnings related to work or business activities conducted in the city.

For corporations, it is a direct tax on income earned in the city with allocation based on property, sales, and payroll.

State law sets the tax rate at 1.0 percent on residents and corporations and 0.5 percent on nonresidents. Some cities are allowed to levy higher rates, but the nonresident rate cannot exceed one-half of the resident rate. For most, the revenue generated is deposited into the city’s general fund; a portion of Detroit’s city income tax revenue is earmarked for the city’s police budget.

City income tax revenue trends

Cities, like other Michigan local governments, rely heavily on local property taxes. Our assessment suggests that property tax revenues are not sufficient to support local budgets and are disconnected from the local economy. These revenues are supplemented with state revenue sharing, which has been cut substantially over the years. Problems with these sources have led to calls to allow local governments in Michigan to levy more types of taxes (e.g., income, sales, gas, etc.). But so far, the state has largely limited this option to city income taxes.

While property taxes are generally stable (one major exception: the Great Recession), income taxes grow with the economy and diversify city revenue sources and tax dependence. Their downside is the reverse: Since income taxes are more connected to the economy, they are more sensitive to the business cycle than property taxes and more likely to fall during recessions.

We can see this happening now. Already, more than a quarter of Michigan’s workforce has filed unemployment claims and payroll employment declined by 26 percent in the second quarter of 2020. Cities that rely on income taxes could experience deep financial pain.

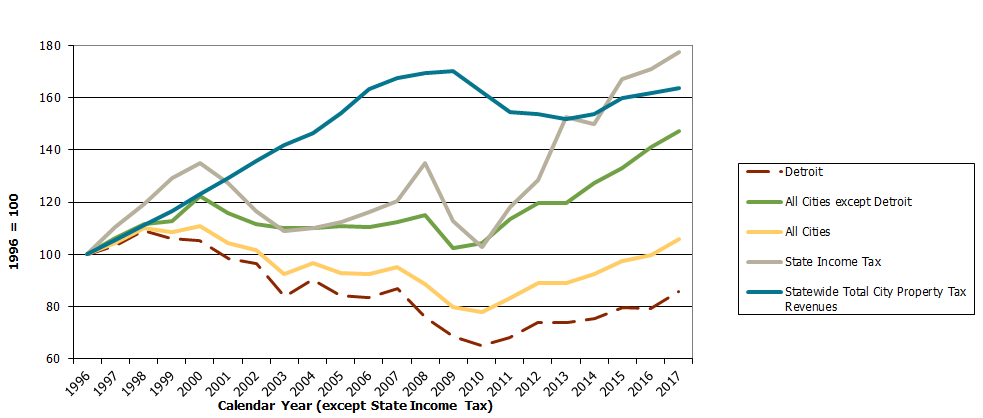

It helps to look at revenue trends over time. The chart below shows state and city income tax revenue growth as well as city property tax revenue growth statewide. City and state income taxes largely fell from 2000 to 2010 due to Michigan’s single state recession and the immediately succeeding Great Recession. The period of economic expansion that began around 2010 saw city income tax revenue grow faster than property tax revenue, but much more slowly than state income tax revenue.

Income and Property Tax Revenue Growth, 1996-2017

Source: Citizens Research Council of Michigan, Outline of the Michigan Tax System; Michigan Department of Treasury

Why the mismatch between state and city? Because income taxes in Michigan are often levied by the state’s struggling cities. The local data captures population out-migration and economic losses in core cities. For example, when we pull Detroit out of the equation, we can see growth improves for the other income tax cities.

If we take a close look at total general fund revenue generated (see table below), we find that these cities get approximately 16 percent of their revenue from the property tax, 34 percent from the income tax, and 19 percent from state revenue sharing.

2018 City General Fund Revenue in Income Tax Cities

| City | 2018 Population | 2018 City Revenue | % from Property Tax | % from Income Tax | % from State Revenue Sharing |

| Albion** | 8,477 | $4,328,120 | 23.6% | 22.4% | 25.6% |

| Battle Creek | 51,247 | $50,035,818 | 31.3% | 33.4% | 11.6% |

| Benton Harbor* | 9,826 | $7,694,016 | 26.2% | 5.5% | 30.1% |

| Big Rapids* | 10,395 | $8,079,497 | 40.6% | 28.4% | 19.3% |

| Detroit | 672,662 | $1,005,999,069 | 11.8% | 30.8% | 19.9% |

| Flint | 95,943 | $50,936,640 | 9.1% | 30.4% | 29.8% |

| Grand Rapids | 200,217 | $131,146,695 | 10.5% | 62.2% | 13.9% |

| Grayling**+ | 1,838 | $1,665,545 | 52.2% | 0.0% | 12.4% |

| Hamtramck | 21,716 | $17,455,737 | 37.9% | 15.7% | 19.5% |

| Highland Park** | 10,806 | $12,543,287 | 21.9% | 30.3% | 24.5% |

| Hudson**+ | 2,217 | $1,963,609 | 37.2% | 0.0% | 13.0% |

| Ionia* | 10,952 | $5,517,281 | 11.8% | 45.5% | 19.9% |

| Jackson* | 32,605 | $24,794,43 | 33.9% | 36.5% | 18.6% |

| Lansing* | 118,427 | $130,362,534 | 29.5% | 29.5% | 14.5% |

| Lapeer** | 8,621 | $12,218,788 | 23.4% | 26.7% | 6.5% |

| Muskegon | 37,287 | $28,729,919 | 25.9% | 30.5% | 14.5% |

| Muskegon Heights** | 10,731 | $7,185,955 | 30.3% | 13.5% | 21.7% |

| Pontiac* | 59,772 | $35,241,739 | 24.3% | 37.8% | 28.2% |

| Port Huron | 28,927 | $22,843,436 | 29.3% | 28.4% | 19.4% |

| Portland*** | 3,927 | $2,095,367 | 51.1% | 0.0% | 20.4% |

| Saginaw | 48,323 | $33,620,591 | 10.7% | 40.8% | 24.9% |

| Springfield** | 5,203 | $4,093,232 | 34.6% | 24.3% | 17.9% |

| Walker* | 24,880 | $17,827,957 | 10.4% | 66.6% | 11.4% |

| Total | $1,616,379,265 | 15.7% | 33.6% | 19.1% |

Note: East Lansing is omitted from the table because it passed a city income tax in 2019 and did not start levying the tax until 2020.

Source: Comprehensive Annual Financial Reports; U.S. Census Bureau; CRC calculations

* State revenue sharing data includes intergovernmental and/or all state revenue from CAFR and may overstate unrestricted state revenue sharing.

** Data from Michigan Department of Treasury F-65 data as reported to Munetrix

*** Portland has a City Income Tax Fund where the $978,774 in 2018 income tax revenues went to support debt service and general government.

+ These cities use income tax revenue for purposes other than to support their General Fund

Issues that could impact city income tax revenue

As the 2018 data show, income taxes make up approximately one-third of general fund revenue. Given this large share, local services will be impacted because of the current recession as income tax revenues dry up in the short term. The outlook for city income tax collections is worse than that for the state tax. Unemployment insurance benefits are not taxable under a local income tax, but they are for state purposes. Thus, cities will experience greater contraction of their tax bases than the state.

Another challenge presented for cities is the extension of the income tax filing deadline (from April 15 to July 15), which could create cash flow problems. While this extension provides valuable relief to taxpayers, it shifts settlement of tax obligations into a new fiscal year for those cities with a July-to-June fiscal year.

For the 2020 tax year, revenues will be affected by the migration to at-home work during the pandemic. Nonresidents are taxed on the income earned while working in the city; those who have transitioned work to their homes will count less of their income as being earned in the city, which will likely be especially problematic for Detroit, Grand Rapids, and Lansing. If people return to the office later this year, this will be a one-time impact; however, if telecommuting and work-from-home becomes more pervasive, this will have a more permanent effect on city finances.

While the short-term outlook is bleak and will depend on how far income tax revenues fall overall, income-tax cities will benefit from having more diversified revenue sources once the economy begins improving. Unfortunately, we do not know when this economic shutdown will end and how far income tax revenues will fall before that happens.