June 3, 2019

June 2019 | Report 407 and Memorandum 1157

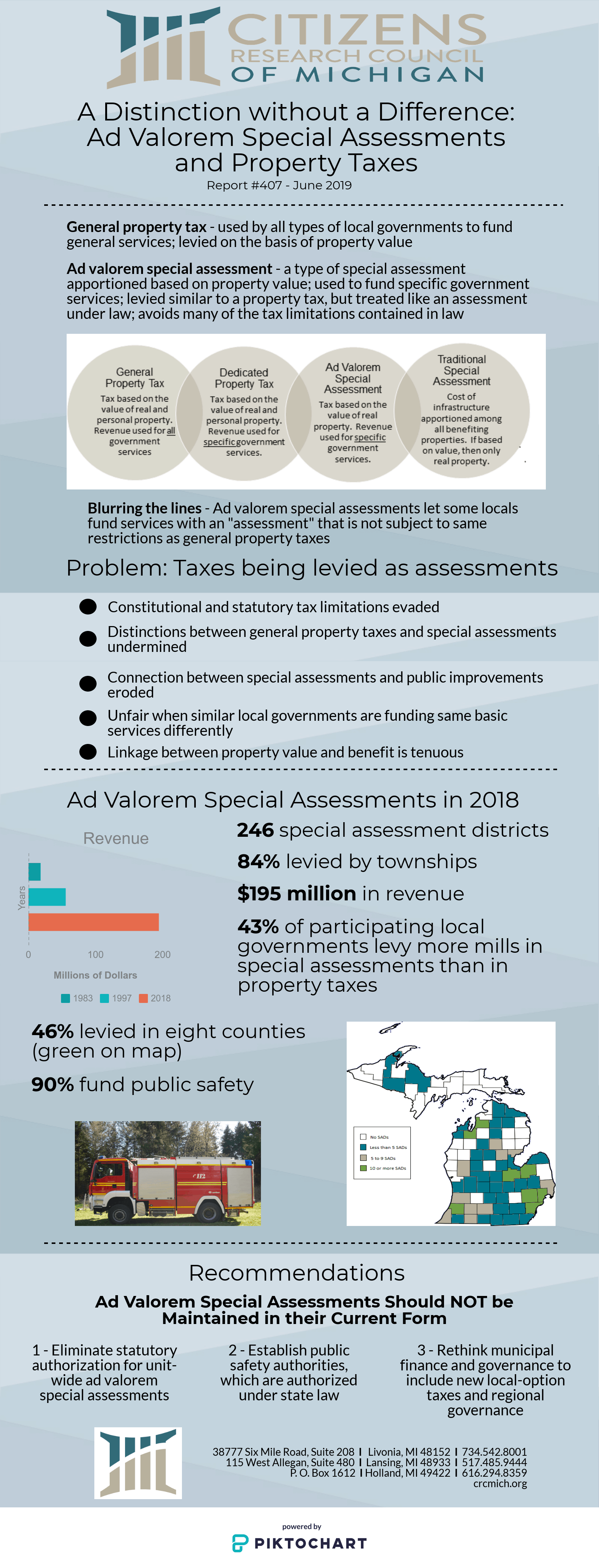

Report – A Distinction without a Difference: Ad Valorem Special Assessments and Property Taxes

- Property taxes are used to fund general services, while special assessments exist to finance infrastructure improvements that benefit a limited number of properties. In recent years, local governments have increasingly turned to ad valorem special assessments to finance general services.

- Ad valorem special assessments are apportioned on property value and levied similar to the general property tax, but they are treated like an assessment and skirt many of the tax limitations contained in law. While their use to finance local government services is technically legal, it undermines the legal and practical distinctions between taxes and special assessments.

- Beside the policy question of whether ad valorem special assessments should be returned to their historic role, their availability to select local governments is unfair to other local governments that are supporting the same general services through property taxes and to taxpayers as their use circumvents tax limitations under state law and distorts the purpose of the special assessment.

- Ad valorem special assessments should not be maintained in their current form. State policymakers should eliminate statutory authorization for all ad valorem special assessments and address the broken municipal finance system so that ad valorem special assessments will no longer be needed. If tax capacity is an issue, local governments should establish emergency service authorities under the process allowed for in state law since the majority of these special assessments fund public safety services.