February 7, 2024

In a nutshell

- The City of Detroit has had more cash on hand in recent fiscal years than at almost any point in the decade before bankruptcy.

- State law requires the city to maintain budget reserves of at least five percent of General Fund expenditures; it is projected to have $150 million in reserve by the end of Fiscal Year (FY)2024, approximately 11 percent.

- Cash on hand is an important part of the city’s financial health and should be closely monitored.

Last week, Moody’s Investor Service bumped the City of Detroit’s credit rating up to Ba1 with a positive outlook from Ba2. It is the second bump up from the company post-bankruptcy.

Governments receive scores on their creditworthiness like people and businesses. Generally, the better the credit rating a government receives, the lower the interest rate will be when it borrows money. With its latest report, Moody’s has essentially informed the municipal bond market that Detroit is a more reliable payer and therefore its debt is a safer asset than previously considered.

The Moody’s report cites several positive indicators for the upgrade, including projected revenue increases, improved budgetary and financial practices, expanded economic development, and lastly the city’s restricted and unrestricted cash reserves. The latter indicator, the substantial increase in the city’s cash on hand, is an important and underreported aspect of the city’s financial turnaround.

Cash and liquidity

Cash is an important element of a city’s financial health because cash is used to pay its bills. Cash is what workers receive on pay day, what bondholders expect to be repaid for loans extended to the city, and what vendors receive after delivering goods and services. Cash is needed for liquidity—a financier’s term for the ability to pay bills as they become due.

If sources of cash, such as tax receipts, come at lesser amounts and/or slower than anticipated, current cash balances must be sufficient so that the city may pay its bills until the next influx. One financial metric intended to capture this idea is “days of cash on hand,” basically the number of days the city will be able to operate using its cash reserves only. While somewhat fantastical, the financial metric asks and answers, “what if disaster struck and current cash inflows ceased, for how many days could the entity continue to operate?”

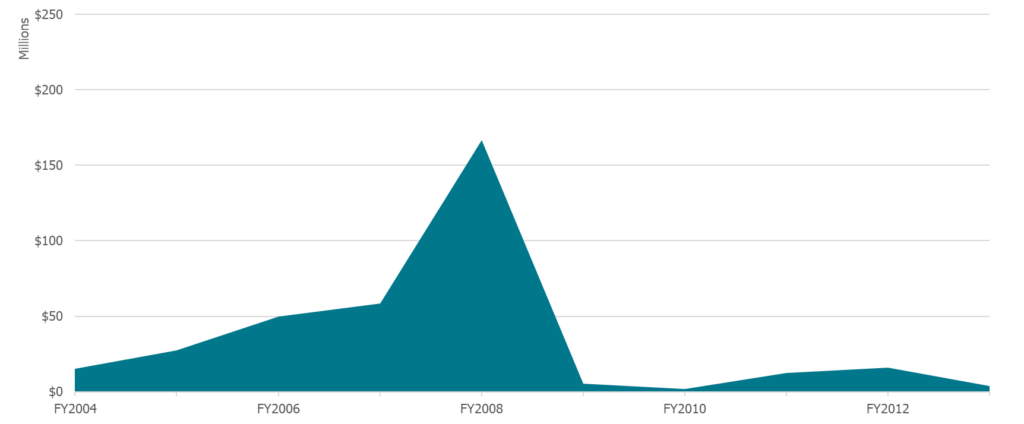

At the end of Fiscal Year (FY)2013, the city’s General Fund had $3.7 million in cash on hand: not even two days’ worth of expenditures. Shortly after the close of the fiscal year, on July 18th, the city filed for bankruptcy under Chapter 9 of the Bankruptcy Code (see Chart 1).

Chart 1

City of Detroit General Fund Cash on Hand, FY2004–FY2013

Source: City of Detroit, Annual Comprehensive Financial Reports, FY2004–FY2013

To be bankrupt under Chapter 9 of the Bankruptcy Code, a debtor must be unable “to pay debts as they become due.” City resources were consumed by payments to bondholders and retirees for pension and other post-employment benefits and in 2013, Detroit had hardly any cash on hand for public services. Even without a formal declaration from a bankruptcy court, for all intents and purposes, the city was bankrupt.

In bankruptcy, the city broke contracts with creditors. City liabilities were restructured to free up cash flow. The city’s foray into bankruptcy court, as evidenced by the city’s cash hoard, did successfully resolve some, yet not all, of the city’s financial problems.

Post-bankruptcy cash hoard

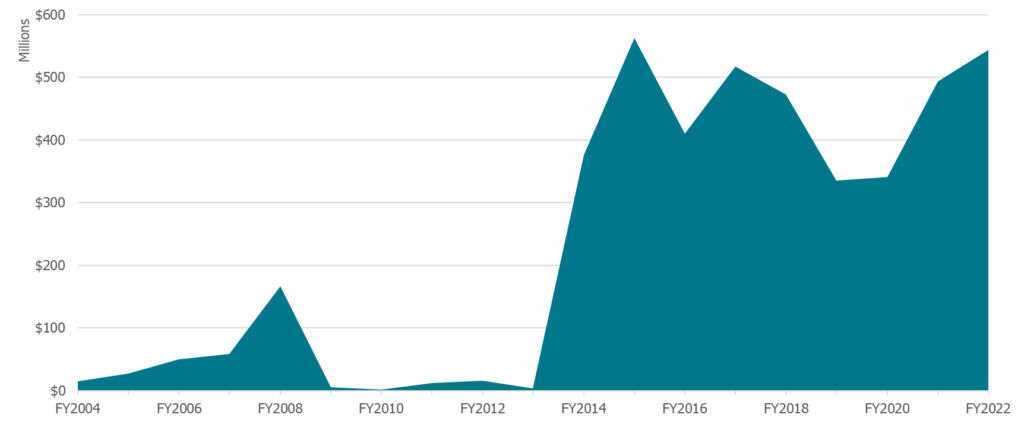

Post-bankruptcy the city has had more cash on hand than at any point in recent history. The pre-bankruptcy spike in cash on hand in FY2009, which was partially attributable to $75.2 million in debt proceeds, is merely a blip when compared to the cash accrued post-bankruptcy as shown in Chart 2. In FY2022, the city ended the year with $544.3 million in unrestricted cash on hand, or 202 days’ worth of expenditures.

Chart 2

City of Detroit General Fund Cash on Hand, FY2013–FY2022

Source: City of Detroit, Annual Comprehensive Financial Reports, FY2004–FY2022

For the most part, the city’s current cash balance is the consequence of annual budget surpluses carried forward. The city has spent this cash on capital projects and other public investments, and it has deposited money into two rainy-day type funds. One, is the budget reserve, a pool of money the city is mandated to maintain under state law. The other is the Retiree Protection Fund (RPF), established in 2017 to make previously paused pension payments that resume in FY2024.

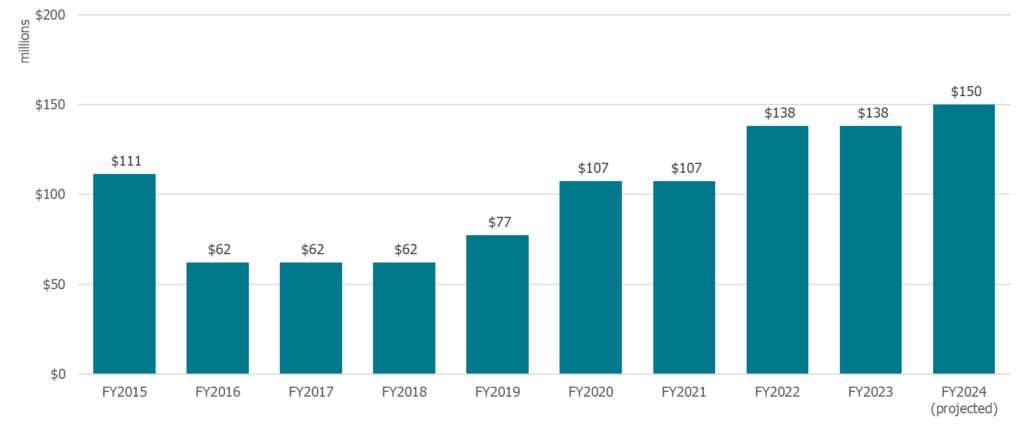

State law requires the city maintain a budget reserve equal to five percent of General Fund expenditures. Since FY2016, the balance of the city’s budget reserve, as shown in Chart 3, has trended upward.

Chart 3

City of Detroit Budget Reserve Balance, FY2015–FY2024

Source: City of Detroit, Annual Comprehensive Financial Report, FY2015–FY2024

Based on the adopted FY2023–FY2027 Four-Year Financial Plan, the city’s budget reserve will have a balance of $150 million by the end of FY2024. At that level, the balance of the budget reserve will be approximately equivalent to 11 percent of General Fund expenditures, over twice what is required by state law.

Separately, the city has insured itself from volatility in pension cost with the RPF. The contractual liabilities attached to Detroit’s pension promises were a part of the $18 billion in total liabilities at the time the city went bankrupt. The city curtailed but did not eliminate these promises. Instead, the two pension funds that supported the planned benefits were closed, benefits to retirees were cut, and the city received a ten-year respite from payments toward those promises.

Pension payments resume in FY2024. By the end of FY2023, the city will have contributed $455 million to the RPF. These assets are invested, and the income earned is estimated to produce another $16 million for the city to withdraw when needed. Put into the words of a former city official, the city “has transformed the POA’s steep pension-funding cliff into a longer, gentler slope…” Chart 4 shows the city’s proposed draw down of RPF assets over the next 10 years.

Chart 4

City of Detroit Retiree Protection Fund Proposed Withdrawal Schedule

Source: City of Detroit, FY2024–FY2027 Four-Year Financial Plan

This planned exhaustion of RPF assets is important to the city’s financial health. As has been documented by the city’s Office of Chief Financial Officer and past posts, the city is on a path to years when projected revenues may not be sufficient to maintain services at their current levels. The use of RPF assets will decrease cash on hand by more than $400 million over the next ten years and it is unlikely that end-of-year budget surpluses will continue to significantly contribute to the balance of cash on hand.

Surpluses, savings, and fiscal rules

City cash balances can be bifurcated into two pools: restricted cash and unrestricted cash. The city’s restricted cash is held within the budget reserve, RPF, and other pools. At the end of FY2022, the city had approximately $229.6 million in unrestricted cash on hand. By the end of FY2024, it will all have been appropriated. How the city has decided to spend both its restricted and unrestricted cash is instructive.

Fiscal rules, those imposed by the state, those imposed by the city on itself, formally and informally, shape how the city makes decisions about how to tax and spend. The state imposed the fiscal rule that the city must maintain a budget reserve no less than five percent of projected General Fund expenditures. The city, with formal adoption by the city council, established the RPF and deposited money in the trust. But informally, the city has typically waited for annual surpluses to be “certified” via audited financial statements before those surpluses are allocated. In other words, if revenues come in above expectations or spending comes in below expectations, the city will wait rather than appropriate the incremental difference.

This informal policy has helped the city match ongoing revenues with ongoing expenditures, a conservative stance toward spending that has been to the city’s benefit. To be sure, there is an opportunity cost to this approach. Rather than use available monies to address problems immediately, the city must wait. But this has helped ensure that annual budget surpluses, that may not reoccur, do not create unfounded expectations for what will be available to spend in the future.

Conclusion

The city’s financial condition has typically been summarized by debt and revenue, surpluses and deficits. But cash is important too. Cash is needed to pay bills on time and in full. The budget reserve, in particular, is insurance that the city can weather an economic downturn, that it can draw down cash if tax receipts fall. Elected officials and citizens should monitor the city’s cash on hand as closely and carefully as other financial metrics.