July 28, 2026

In a nutshell:

- In FY2024, Detroit will resume payments to its two pension funds.

- The city will make payments of $135 million annually for the next ten years before the amount increases to $154 million as pension reserves are exhausted and the Grand Bargain expires.

- Challenges for the city lay ahead with an uncertain amortization schedule, projections of a mismatch between revenues and expenditures beginning in FY2029, and the expiration of Grand Bargain money.

Introduction

It’s been almost ten years since the City of Detroit filed for the largest municipal bankruptcy in American history. Part of the bankruptcy agreement included a plan for the city to fund its retiree pensions – a significant share of the city’s debt burden. To regain its fiscal footing, the agreement provided the city budget with a reprieve from making annual pension payments. That pause comes to an end soon.

City officials are currently in the process of developing the Fiscal Year (FY)2024 budget, a budget that will have to incorporate these pension payments.

As the city prepares its spending plan and its long-term budget forecasts, there are potential challenges to consider as it resumes these legacy pension payments. They include uncertainty surrounding how long the city will have to pay down its pension debts, a developing, but relatively small, mismatch between revenues and expenditures, and the expiration of Grand Bargain money.

Background

It was June 2013, and the city was in a dire financial situation facing significant debt burdens estimated as high as $18 billion. The city could not pay for many basic city services and was at risk of seeing one of its most valued assets used to pay off creditors (i.e., art in the Detroit Institute of Arts (DIA)). About half of the city’s liabilities were worker-related, including pension-related obligations and retiree health benefits. Retirees had much to lose as pensions were at risk of being cut.

On December 10, 2014, the city exited bankruptcy with the adoption of the Eighth Amended Plan for the Adjustment of Debts of the City of Detroit (the “Plan of Adjustment” (POA)) – otherwise referred to as the bankruptcy agreement. The POA provided a plan for the city to restructure its debt obligations. It relieved the city of $7 billion in debt and saved DIA artwork from a forced sale.

Part of Detroit’s historic POA included a debt-cutting plan and a nine-year break from dealing with most of the pension-related debt. Instead, those pension costs were met through contributions from private parties and the State of Michigan as part of an agreement commonly referred to as the “Grand Bargain.“

The “Grand Bargain” was an unprecedented collaborative effort that yielded $820 million worth of donations to make payments into the city’s pension plans on the city’s behalf. The city’s philanthropic community contributed $370 million, the State of Michigan contributed $350 million, and the DIA committed an additional $100 million.

Grand Bargain support allowed the city to avoid pension contributions for several years. During that time, the city put money aside in reserves to lessen the burden on the General Fund once payments resume. The POA calls for payments to resume in FY2024.

Implications for the Budget

City officials are beginning to put together the FY2024 budget to be submitted to city council in March. The budget will have to resume annual contributions to its General Retirement System (GRS) and the Police and Fire Retirement System (PFRS) pension funds from the General Fund.

The new fiscal year begins on July 1, with the city responsible for making yearly contributions of $135 million – nearly 12 percent of the General Fund budget. That payment amount could change based on a pending court ruling from a motion filed by the city to restore the amortization period defined by the POA. Pension payments will be made using a mix of reserves and General Fund revenues.

However, city reserves and the Grand Bargain money will only last for a few years. The city projects that pension payments will remain at $135 million per year until FY2035. In FY2035, money from the Grand Bargain expires and payments will be made exclusively from the General Fund and remaining reserve balance. This will cause pension payments from the city’s General Fund to jump to $154 million per year.

While pension payments will be a significant new addition to the budget, city officials have prepared well for this moment. Budget surpluses and growing reserves have put the city in a good position to resume payments.

Budget Surpluses and Growing Reserves

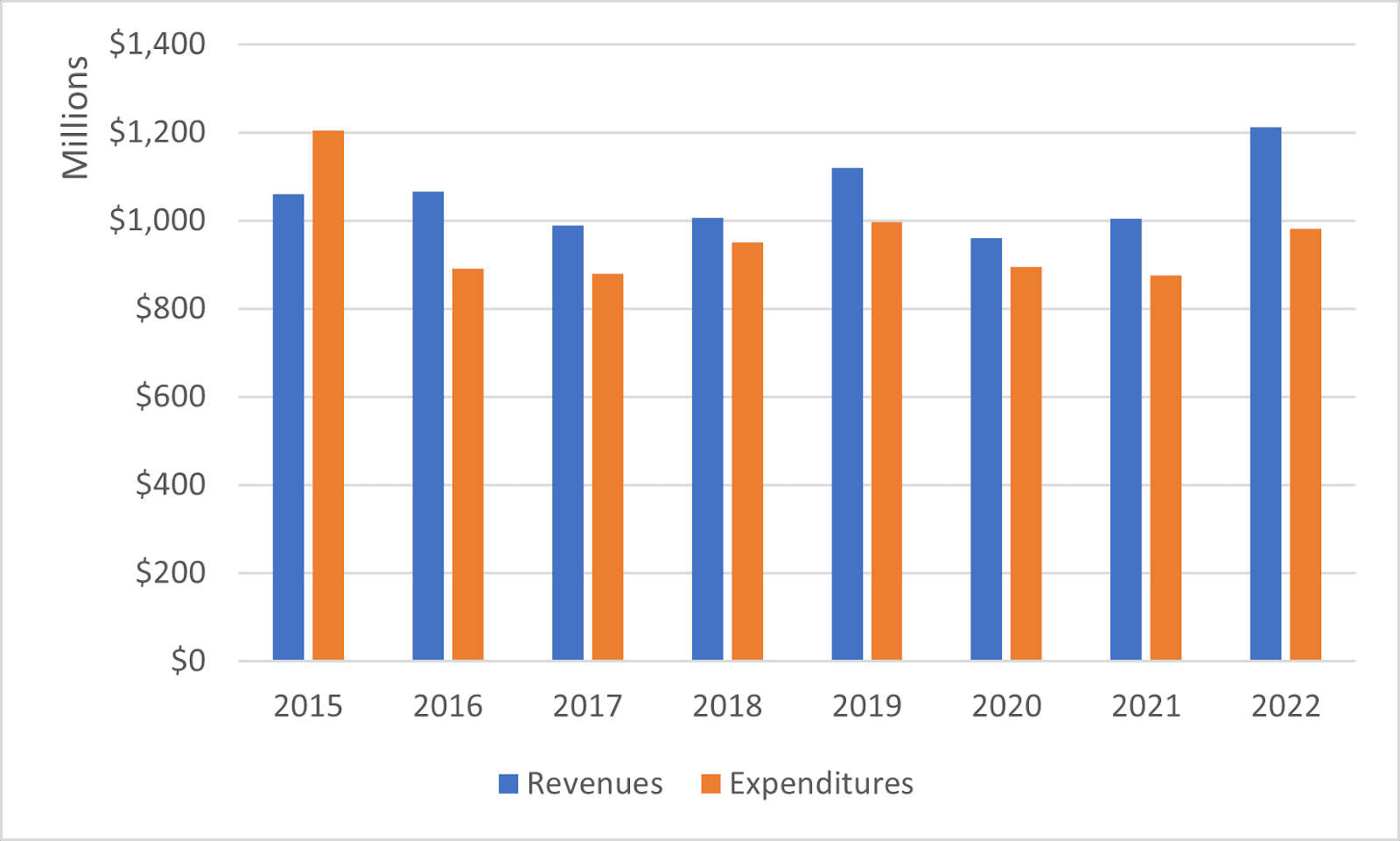

Since its exit from bankruptcy, the city has operated with balanced budgets. General Fund revenues have exceeded expenditures, resulting in budget surpluses each of the last seven years (see chart below).

City of Detroit’s Annual Revenues and Expenditures, FY2015 to FY2022

These surpluses have helped the city grow its unassigned fund balance. In FY2015, the city’s unassigned fund balance was $71 million and has since grown to $230 million in FY2022. As the city continues to adopt balanced budgets, it has used one-time surpluses to increase reserves that will be important once pension contributions resume.

These reserves have been set aside in the Retiree Protection Fund (RPF) to prepare for the upcoming return to actuarially-based funding of its pension obligations. The RPF was created in 2017 to function as a savings account to help cushion the blow of the pension cliff dedicating hundreds of millions of dollars to tackle the upcoming pension payments.

In FY2023, the city initially deposited $135 million into its RPF and then increased it by $90 million using one-time surplus funds. By the time the city resumes legacy pension contributions, the RPF will have a total of $460 million to help absorb the new costs (see chart below).

City of Detroit Retiree Protection Fund, FY2018 to FY2023

Source: City of Detroit

The city plans to make required payments to the pension plans through a combination of increasing payments from the General Fund and the Retiree Protection Fund. The city expects to pay $73 million from the General Fund and $62 million from the RPF in the first year of payments. In FY2025, the city will pay $76 million from the General Fund and $59 million from the RPF. This will continue until the fund is used up.

The city also has bolstered its rainy day fund using its annual surpluses. Rainy day funds are effectively budget reserves that help cities prepare for revenue volatility. In FY2023, the city increased its rainy day fund balance by $31 million to a new total of $138 million, which equates to about 11 percent of the city’s General Fund budget. The city plans to add $15 million in FY2024 and $5 million in FY2025, bringing its total reserves to $158 million.

The rainy day fund will be an important buffer as the city ramps up its spending in future years with the start of pension contributions in FY2024. These reserves prevent the city from taking out of its operating budget to cover unfunded pension liabilities.

Detroit’s Future Outlook

Detroit’s FY2022 Comprehensive Annual Financial Report (CAFR) shows the city’s strong financial position with growing reserves and a budget surplus. City revenue growth has exceeded previous projections and income tax revenues are projected to continue increasing from big development projects and decreasing unemployment rates. Detroit’s unemployment rate hit 6.4 percent in November 2022, its first time below seven percent in 22 years.

With a promising financial outlook, the city seems ready to take on pension payments. However, the city does face challenges as its reprieve from pension payments comes to an end.

Detroit’s first big challenge involves the amortization period for its two pension funds. The funding policy agreed upon in the POA established pension amortization schedules for the PFRS and GRS that call for contributions to cover unfunded pension liabilities to be spread over a 30-year period. Last year, the PFRS Board changed the amortization period to a 20-year period.

The PFRS Board found that the change was the best move to ensure solvency of the pension funds. However, this change in pension funding increases the city’s costs on the front end. Shortening the amortization period for the city will require larger annual contributions upfront, thus impacting the city’s fiscal condition.

On August 3, 2022, the city challenged the resolution by filing a motion with the Bankruptcy Court to enforce the original terms of the POA and restore the 30-year amortization period. On September 9, 2022, the PFRS filed a response, and the Bankruptcy Court is yet to hold a hearing on the matter.

A shorter payment schedule for legacy pensions could impact the city’s ability to spend on services for businesses and residents in the future and the pension systems that serve retirees. If the Bankruptcy Court were to rule in the city’s favor, upfront costs would decrease by $14 million a year creating more of a surplus for the city’s year-end budget.

The next challenge arrives in FY2029 when expenditures in Detroit’s annual budget are projected to begin exceeding revenues. Forecasts early in 2022 projected the city to confront a mismatch between revenues and expenditures beginning in FY2027 unless revenues are increased or expenditures reduced to maintain a balanced budget.

However, with revenues performing better than the city’s baseline forecast, this threat of a mismatch is projected to be delayed by two years. If the amortization schedule were extended back to a 30-year period, the risk of a mismatch might be further delayed. This is good news for Detroit as it buys more time to grow reserves and increase revenues, which will help offset the shortfall in spending once the mismatch between revenues and expenditures comes to be.

Another shift in where the city needs to allocate its resources comes in FY2035 with the expiration of the Grand Bargain money. The Retiree Protection Fund is also projected to be spent by FY2038, at which point legacy pension payments will be made exclusively by city revenues. As contributions from the Grand Bargain and the Retiree Protection Fund cease, the city will have to budget wisely to afford pension payments made exclusively from its General Fund.

The city will have to rely on its tax base to generate enough revenue to pay for its pension plans, debt service, and basic city services. As of now, the city appears to be in good financial health to take on future obligations. It must continue to prioritize growing its tax base and generating enough revenue to accommodate growth in pension costs in the budget.

Conclusion

Detroit’s revenue recovery and updated actuarial valuations have provided additional financial stability for the city, putting it in a favorable position to tackle upcoming legacy pension contributions. However, risks remain with an uncertain amortization schedule, a potential mismatch between revenues and expenditures in FY2029, and the expiration of Grand Bargain money.

Within the next month, the city will publish an updated long-term forecast report for its finances. February’s revenue estimating conference will provide a glimpse of revenue projections over the next four years. These reports will provide a clearer picture of how ready the city is to begin its legacy pension contributions and what the long-term outlook for the city will look like with new financial obligations.