March 25, 2025

In a nutshell:

- Royal Oak Township provides an example of how the design of Michigan’s municipal finance system has allowed certain local governments to use ad valorem special assessments to live beyond their property tax revenue raising means.

- Royal Oak Township’s overuse of ad valorem special assessments is largely a byproduct of the fiscal constraints placed upon it and similar communities by Michigan’s municipal finance system. Township officials literally have no other revenue-raising options.

- Local governments in Michigan may need us to review how state law governs city incorporation and annexation and how local services are funded and provided.

The design of Michigan’s municipal finance system has allowed certain local governments to use ad valorem special assessments to live beyond their property tax revenue raising means. Their use continues to raise concerns with citizens that are forced to pay them alongside their ad valorem property taxes, as well as with other local units that feel their selective use is unfair. Regardless of these very real concerns, the use of ad valorem special assessments has only grown statewide.

Ad valorem special assessments and Royal Oak Township

One particular government — Royal Oak Township — has relied heavily on ad valorem special assessments to fund services. In 2020, Royal Oak Township levied four ad valorem special assessments that combined to raise much more revenue than their general operating property tax. In 2021, however, the township did not levy any ad valorem special assessments. A review of budget documents and the township’s tax base shows how important these ad valorem special assessments have been to keep the township operating and providing services.

The township cannot increase the general property tax due to tax limitations. It has no other taxing options other than reinstating these ad valorem special assessments, which are levied on the same tax base as the property tax. The problem with these special assessments is that while technically legal, they push the boundaries of what is and is not a tax. They skirt the property tax limitations in state law and strain the property tax base and taxpayers’ ability to pay.

Royal Oak Township: Caught in a bad system

Royal Oak Township has long been the poster child for the overuse of ad valorem special assessments. But, the township’s overuse of these assessments is largely a byproduct of the fiscal constraints placed upon it and similar communities under the state’s municipal finance system.

While the Charter Township Act limits the township tax rate to 10 mills with voter approval, Royal Oak Township was levying a total of 20.75 mills in four ad valorem special assessments, as well as 13.1 mills in general property taxes for a total millage rate of 33.9 mills (a mill is $1 of tax for every $1,000 of taxable value). These special assessments were levied to fund garbage and disposal services (4.0 mills), fire services (13.0 mills), parks and recreation (1.25 mills), and street lights (2.5 mills).

Not only is this total tax rate above the 10 mills authorized to charter townships, it is higher than the 20 mill rate authorized to cities in the Home Rule City Act. Not surprisingly, the very high combined property tax burden has caused some consternation for property owners. The question is how did Royal Oak Township find itself in the situation where it is levying prohibitively high ad valorem special assessments to fund basic services that few people would consider to be unnecessary.

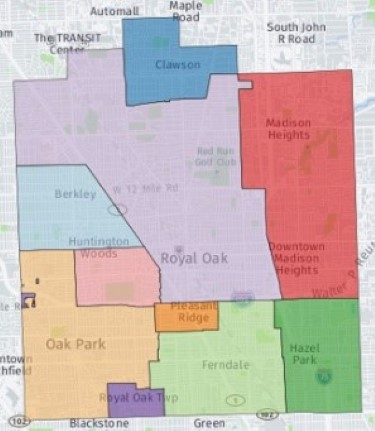

We can start by looking at the geography and demographics of the township. Royal Oak Township started out as a 36-square-mile township in Oakland County. Its footprint began to shrink in 1921 when parts of the township were incorporated as cities. Today, what remains is a 0.55-square-mile township. It became a charter township in 1972, which made annexation and incorporation harder for the surrounding cities. By this time, it was already the smallest charter township in the state and left with little land area or tax base (see Map 1). The township had 2,374 residents as of 2020. The population has dropped steadily since 1930 as the township lost more and more of its population to surrounding cities.

Map 1

Royal Oak Charter Township and Surrounding Cities

Today, Michigan’s State Boundary Commission provides guidelines for municipal incorporation, annexation, and consolidation. However, the state law delineating this commission and its responsibilities was passed in 1968 after much of the incorporation around Royal Oak Township happened. It’s clear by looking at the little tax base remaining in Royal Oak Township that we might want to review the state process that has allowed for the creation of communities like Royal Oak following incorporation and annexation – very small, land-locked, with a very low tax base.

Financial problems for Royal Oak Township

Royal Oak Township was placed under a state-appointed emergency financial manager in part because of its inability to fund services from a depleted tax base. The 2014 consent agreement between the state and township explicitly states that the township must reauthorize its special assessment millage. In this light, state officials have perpetuated the township’s use of the special assessment band-aids.

Royal Oak Township officials took the special assessment band-aid that was handed to them from the state. They cannot raise tax revenues through any source other than property values. Their last best option was raising funds through ad valorem special assessments and they have been doing that for years. However, when special assessment rates get as high as they were in Royal Oak Township, taxpayers begin to take notice.

This has led to the township’s most recent financial problems. In 2021, Royal Oak Township levied zero mills in ad valorem special assessments; its 2021 property tax rate remained at 13.1 mills. The question is how is the township paying for services (e.g., fire and street lights) previously funded through special assessments? According to the budget document, they are relying on fund balances and interfund transfers. This is a stop-gap measure, but not a long-term solution.

Township officials told me that they were advised that the special assessment districts were not set up correctly originally so they are going through the process with legal counsel to re-form these districts with public hearings in order to continue to provide these services to residents. The plan is to reinstate these ad valorem special assessments because, the truth is, township officials have no other options available under the municipal finance system.

Local Governments Need a Better Solution than Special Assessment Band-Aids

While the Research Council has been arguing against the use of ad valorem special assessments for years (most recently in a 2019 report as follow up to a follow-up to a 1997 report, which was a follow-up to a 1983 report), we have also stated that many local governments find themselves in a tough financial situation with no good options to raise revenues. Local governments in Michigan, especially those in urban or suburban areas that are already fully developed, need a municipal finance system that allows them to capture revenues that reflect their economy and provide the services their residents desire. While Royal Oak Township may be a poster child for the misuse of ad valorem special assessments, it is also a prime example of a local government that is without any good options in our municipal finance system.

Our research shows that property tax limitations effectively prevent local governments from growing their tax base through any means other than new development. This leaves built-out, land-locked suburban communities like Royal Oak Township with few options to raise revenues. With a few exceptions (e.g., income taxes for cities and some small tourism-related taxes for select counties), the state does not generally allow local governments in Michigan to levy local-option taxes. Truth be told, communities like Royal Oak Township would probably lack strong income or sales tax bases as well, but options would relieve pressure on the property tax base and certainly reduce the need for ad-valorem special assessments to fund critical public services.

In addition to local tax options, communities like Royal Oak Township may need us to review how state law governs city incorporation and annexation and how local services are funded and provided. Without major reforms to the municipal finance system, ad valorem special assessments are a last line of revenues for desperate local governments.

Permission to reprint this blog post in whole or in part is hereby granted, provided that the Citizens Research Council of Michigan is properly cited.