July 28, 2026

In a nutshell

- Municipal bonds can be thought of as loans that investors make to governments, similar to a mortgage from a bank that a homebuyer might have.

- Bonding allows governments to borrow to cover the costs of infrastructure construction.

- As of December 31, 2020, Detroit has approximately $1.98 billion worth of gross direct bonded debt equating to debt of about $3,105 per resident.

Government levies taxes on income, property and the purchases of citizens to pay for public services. However, the cost of the construction for safe and reliable infrastructure and equipment often exceeds annual general tax collections. As an alternative to a “pay-as-you-go” financing strategy, bonding allows governments to borrow to cover the costs of infrastructure construction.

In this blog, we introduce the concept of municipal bonding and set the stage for a series of blogs that will examine Detroit’s bonded debt and debt limit. Our intended purpose is to begin to analyze what Detroit’s debt situation is as we approach the end of the city’s Plan of Adjustment in 2023.

Background

A bond is a loan from an investor to a borrower such as a company or government. The borrower uses the money to fund a major investment and the investor receives interest on the investment. There are different types of bonds all of which can be structured in many ways. Municipal bonds can be thought of as loans that investors make to governments, similar to a mortgage from a bank that a homebuyer might have.

Municipal bonds are issued to finance capital expenditures, such as installing water and sewer lines or road and bridge construction. Terms of a bond include the amount borrowed, interest rate, and the maturity date of the debt. The city’s bonding authority is granted under the Detroit city charter (Article VIII, Chapter 5) through the Home Rule City Act (MCL 117.5f(2)).

General Obligation and Revenue Bonds

Municipal bonds are typically structured either as general obligation bonds (GO) or revenue bonds. The difference between these two bonds are the repayment methods. A GO bond is backed by the credit and taxing power of a city rather than a dedicated revenue stream. They have the “full faith and credit” of the city, meaning the debt is backed by the city’s power to levy taxes to make all required payments. The amount of taxation available by a particular GO bond may be specified as either limited tax or unlimited tax general obligation bonds. Both classes of GO bonds are subject to a statutory limitation on the amount of debt a local government may have outstanding at any one time.

Unlimited tax general obligation bonds must be approved by the voters and are repaid from property taxes levied specifically for that purpose. Michigan’s Unlimited Tax Election Act indicates that unlimited tax pledges may be imposed without regard to any property tax limitation. An example of such a voter-authorized bond that was passed by Detroiters in 2020 is Proposal N that received voter approval to remediate blight.

Limited tax general obligation bonds do not require voter approval. They are repaid out of the general fund of a city. Some of Detroit’s limited tax debt has been secured by specific general fund revenues such as state aid. This is essentially money borrowed for operations that has an annual cost that is paid out of the general fund. These bonds are generally supported by the full faith and credit of the city and the debt service becomes the first obligation in the city budget diminishing funding available for services such as police and fire protection, public health, public lighting, parks and recreation, and other services.

Revenue bonds are issued to fund public projects with dedicated revenue streams. Rather than repaying these bonds from dedicated property taxes or the general fund, they are supported by revenues from that revenue stream, such as water fees or state highway distributions.

How Much Debt Does Detroit Have?

The amounts in the chart below include the principal outstanding on limited and unlimited tax general obligation bonds, as well as, debts incurred from revenue bonds and other projects. The amounts that will be paid on those liabilities will also include interest and could include other costs as well.

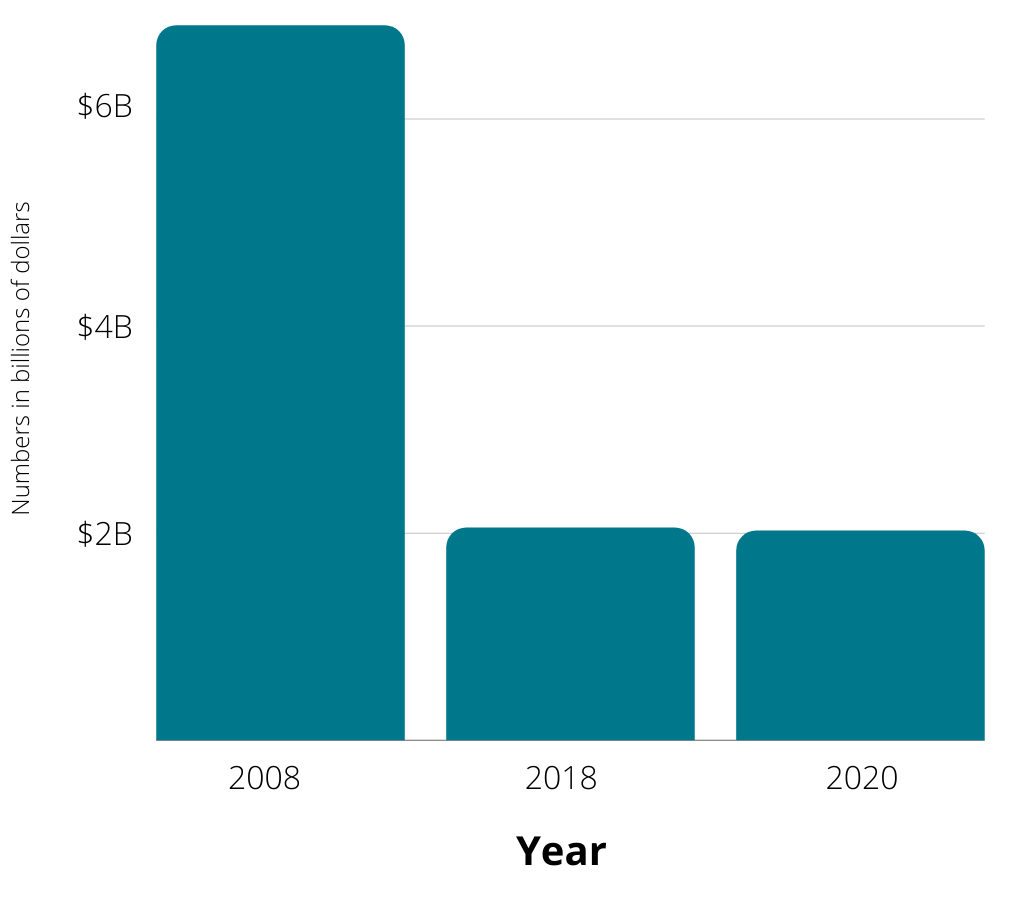

Detroit’s Gross Direct Bonded Debt, 2008, 2018, and 2020

Source: Munios Reports – Detroit OCFO Treasury Office

As of December 31, 2020, Detroit had $1.98 billion worth of gross direct bonded debt. Calculating the amount of debt per capita in Detroit is tricky because the population continues to decline. In 2020, this equates to about $3,105 per resident. In December 2018, Detroit had approximately $2 billion worth of gross direct bonded debt that equated to about $2,972 per resident. This is a stark difference to 2008 when the city’s gross direct bonded debt was $6.9 billion equating to about $7,509 per resident. Payments on the vast majority of the debt will be spread out decades into the future.

These figures represent the debt Detroiter’s bear in exchange for making improvements to their city. Analyzing the debt per capita for each year, we see that changes in population plays an important role in determining how much city debt residents bear. A continuing decline in population places a huge burden on Detroit taxpayers to pay back the debt burden of a city that continues to lose its tax base.

In recent years, the city has taken actions to reduce recurring debt service and eliminate the prior debt cliff through a repurchase and refunding transaction. A debt cliff refers to a critical imbalance in government’s revenues versus obligations, creating a looming budget deficit shortfall.

What is Detroit Indebted For?

The city is responsible for maintaining a large inventory of capital assets including roads, parks, public safety facilities, municipal buildings, libraries, etc. While the city has taken on more debt recently, it has done so with the intent to improve these capital assets.

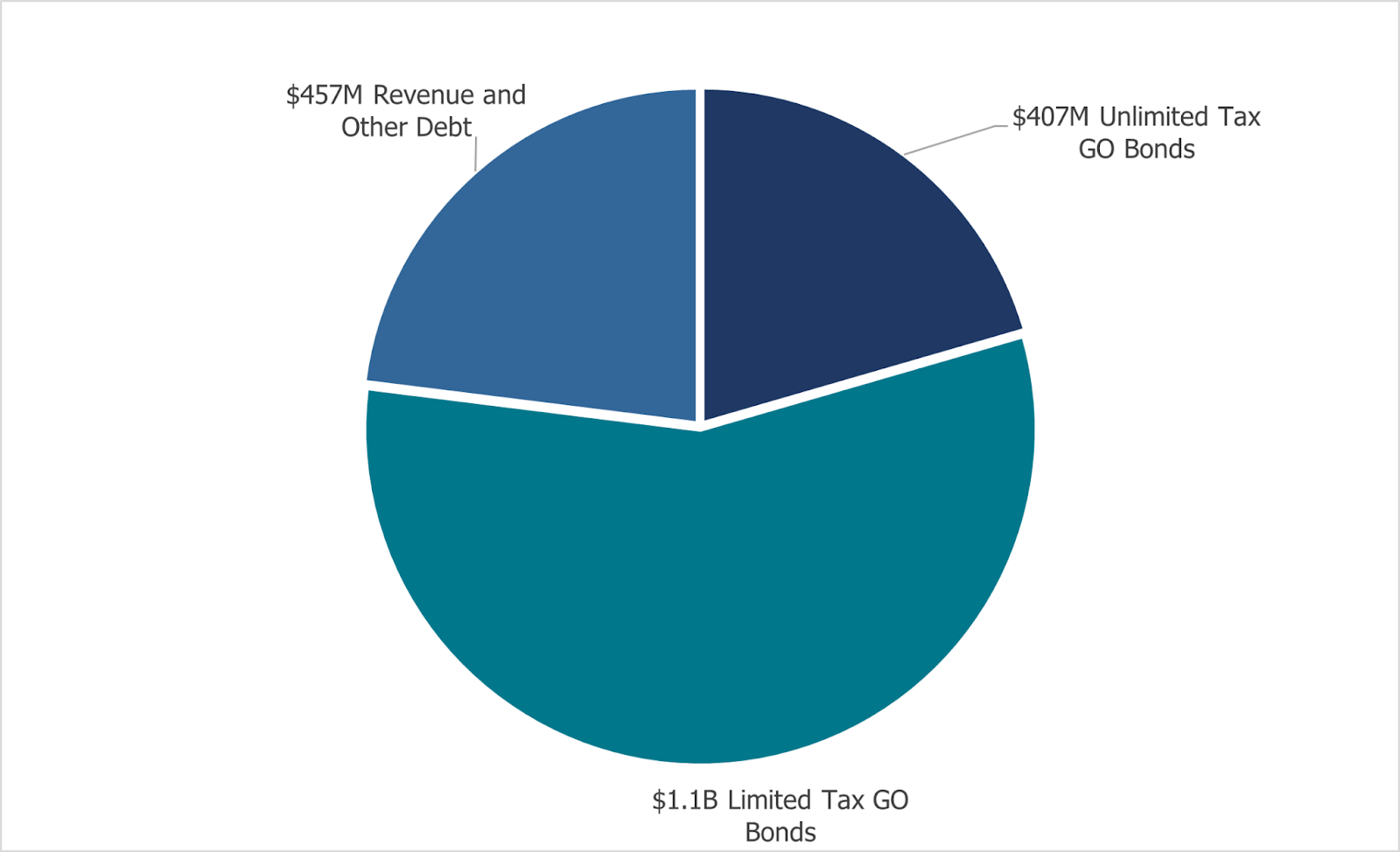

The chart below provides a breakdown of Detroit’s indebtedness which include general obligation bonds, revenue bonds and debt from other projects. In 2020, Detroit had approximately $1.98 billion in gross direct debt made up of $1.5 billion of tax supported debt including unlimited tax and limited tax general obligation bonds. The other $457 million was made up of revenue bonds and debts from other projects. Payments for these debts will come due annually through 2050.

Detroit’s Indebtedness, 2020

Source: Munios Reports – Detroit OCFO Treasury Office

Conclusion

Upon the city’s return to the bond market on its own credit in 2018, the proceeds of the city’s unlimited tax general obligation bonds issued in 2018 and 2020 have supported the capital agenda’s plan for investments in public safety, recreation and museums, economic development, and transportation.

Questions, however, continue to arise about the city’s ability to service its debt considering the unpredictable nature of the post-covid world. Detroit is ostensibly $7 billion less indebted than it was pre-bankruptcy having fewer claims on its limited resource post-bankruptcy. In addition, a number of Detroit’s financial metrics have improved between bankruptcy and now. The city has fewer liabilities to compromise its financial condition, placing it in a more favorable position to pay back what it owes post-bankruptcy.

Permission to reprint this blog post in whole or in part is hereby granted, provided that the Citizens Research Council of Michigan is properly cited.