July 22, 2026

In a nutshell

- Property tax assessments look at property and attempt to place fair values on them so that local authorities can tax residents accordingly.

- While no assessment system is perfectly accurate, property owners rely on local government assessors to fairly estimate property value for taxing purposes.

- Detroit is estimated to have overtaxed homeowners by at least $600 million; this has created a misconception among residents that the money is currently being held by local governments and can be returned to taxpayers.

As I was wrapping up an interview on the Urban Interest webcast on Detroit IPTV, host Angela Matthews said something that struck me (starting at 1h:04 min). She asked where the $600 million of tax revenue from the overtaxation of Detroit property owners can be found. She and others hope to identify the government fund currently holding the money and pursue options to return it to those who were overtaxed.

Detroit is estimated to have overtaxed homeowners by at least $600 million over a six year period following the Great Recession. However, this dollar amount is a conservative estimate and it is likely that all Detroit property owners were overtaxed by more. Property values were over-assessed for a number of years with lower-valued homes suffering most from the over taxation.

The financial burden of these over-assessments put thousands of Detroiters at risk of foreclosure. This added to the mistrust and cynicism many Detroiters harbor about city government. Not surprisingly, this has led to public calls to return the $600 million from overtaxation. However, the idea that $600 million is a tangible amount of money sitting in a government account that can be easily returned to Detroiters is a misconception many residents have expressed. As we explain below, some of this confusion arises from the complexities of property taxation and how it works, with a particular focus on the assessment side.

Property Tax Basics

Property tax revenues pay for public safety, infrastructure, libraries, garbage pickup, and other municipal services. City residents also pay property taxes to support other services, delivered by overlapping taxing jurisdictions responsible for K-12 education, community colleges, a variety of county services, and many regional services. The revenue generated from property taxes are distributed to the relevant governmental jurisdictions based on millage rates. It is not revenue that can be “found” and is not sitting in a single government account. Multiple governmental jurisdictions levy Detroit property taxes based on the property value.

Generally, taxes are calculated by applying the tax rate to the tax base. For most taxes, this is a fairly straightforward calculation. Property taxes, however, tend to be a little more complicated. As such, compared to other taxes, it is much harder for an individual property owner to know and understand whether they are being accurately taxed.

To illustrate, consider the calculation of the state sales tax rate. For a $100 purchase of taxable goods, the state six percent sales tax would require an additional $6 from the purchaser. If that charge is higher or lower, the purchaser would be able to instantly identify the error. The same is not true for property taxes because the process by which the value of property is determined is based on various factors used in the assessment process.

Property taxes are levied on an ad valorem basis, meaning that the tax is proportional to the value of the property. But how does one know the value of a parcel of property if it is not currently for sale and people are bidding on it? For properties that have recently been sold, the sale price is usually a reasonable approximation of its market value. However, only a small proportion of the total parcels of property are sold in any given year. For governments levying property taxes, they must rely on estimates of the value of each taxable parcel. This occurs through the assessment process carried out by trained local assessors.

A property assessment tries to place a fair value on each parcel. The Michigan constitution requires the uniform ad valorem taxation of all properties and for the determination of the value to reflect the usual selling price or true cash value. To determine true cash value, the assessor must consider a number of things, including:

- Comparable properties that have sold recently

- Advantages and disadvantages of the location

- Quality of the soil

- Zoning

- Existing use

- Water power and privileges

Further, property is classified as residential, commercial, and industrial (and other minor classifications). The assessment of the various classes of property generally uses one of three methods. The “sales comparison approach”, which compares property to other similar-sized properties in the area that have sold recently, indicating how much the property would fetch if it were to be sold. The “customary mass appraisal approach” has the assessor estimate how much it would cost to build a property at today’s rates. And the “capitalization of income” approach which is usually applied to commercial properties whereby the rental income the property generates is used to calculate its value.

All of these factors are considered by a local assessor to establish the true cash value of a parcel for tax purposes.

The Importance of Accurate Assessments

When local governments conduct assessments accurately, the resulting property taxes are proportional to the value of the property. However, when property assessments are conducted incorrectly, the resulting property tax bill for property owners will also be inaccurate. Properties can be over-assessed (and overtaxed) if the assessed value is higher than the actual market value. Conversely, property can be under-assessed (undertaxed) if the assessed value is lower than the actual market value.

While no assessment system is perfectly accurate, residents rely on local assessors to accurately determine the value of property. When a system results in over-assessment, it creates a financial strain on residents, especially those with the least means to keep up with their tax bills.

Detroit’s over-assessment problems were particularly acute for those least able to afford it. The assessment inaccuracy was found to be regressive; this occurs when low-value homes are assessed at a higher percentage of their true market value than assessments of higher-value homes. This inaccuracy leads to regressive property taxation. One study found that the city’s residential property assessment methodology continues to harm Detroiters in over-assessments and the resultant tax foreclosures of homes from over-assessed properties.

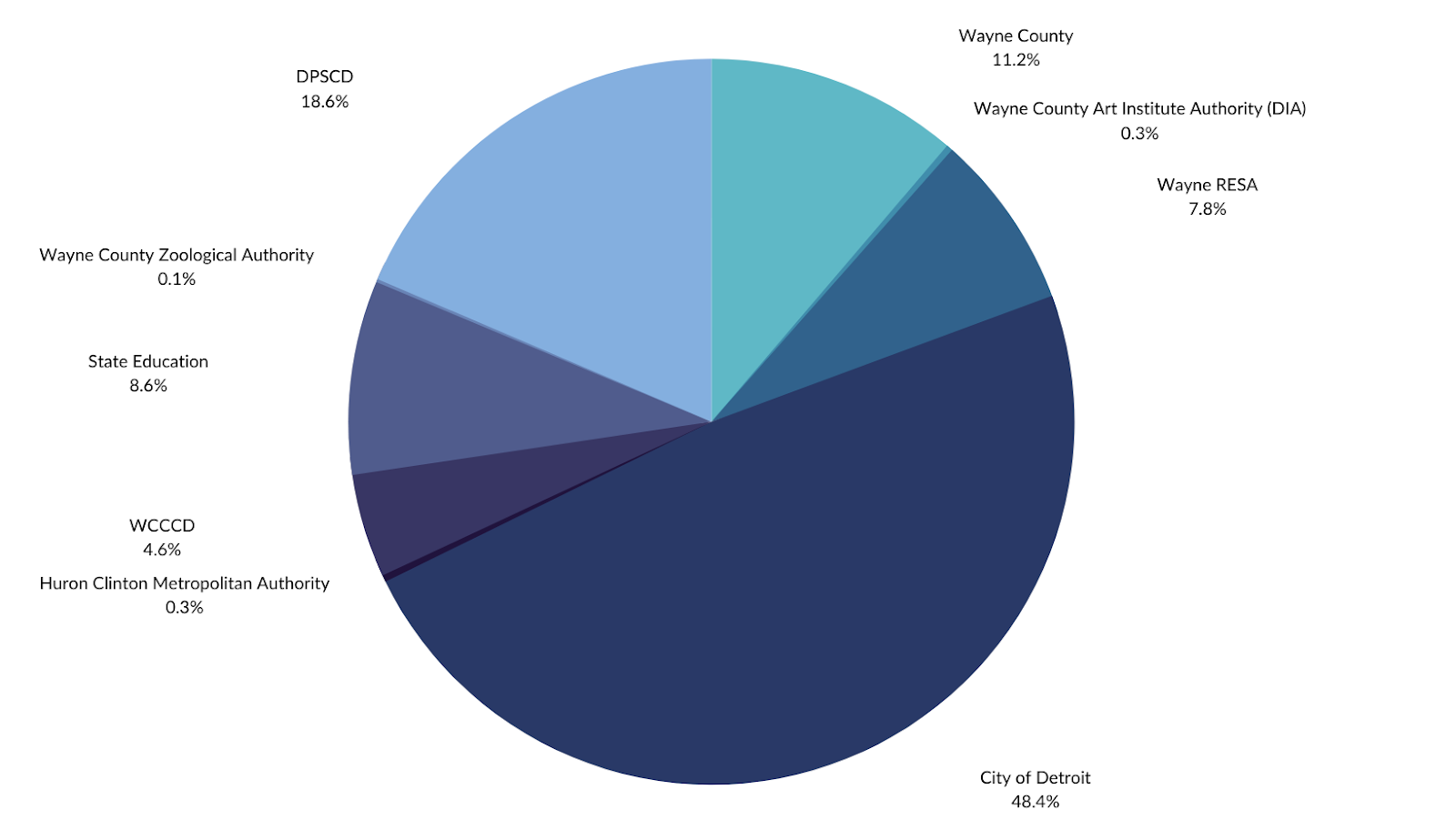

Once the assessor has determined a fair value for the property, it is multiplied by the various state and local tax rates to arrive at the amount of property tax owed. Property owners pay taxes to multiple taxing jurisdictions at various rates. Regardless of the taxing jurisdiction (i.e., tax rate), the same property assessment is used for the tax base. Of the total $600 million in Detroit over-assessments, less than half was levied by the city and the remaining 52 percent was levied by overlapping governmental jurisdictions (see chart).

Detroit Over-Assessed Property Tax Revenue by Taxing Jurisdiction

Source: Detroit OCFO Treasury Office

The estimated $600 million in overtaxation has already been distributed among and spent by the city and the overlapping jurisdictions that levy property taxes on Detroit properties. It is not a tangible amount of money that can be found and returned to Detroiters. Neither the city nor any of the other benefiting jurisdictions have kept the extra tax revenues in escrow. Refunding taxes would require each responsible government to either scale back services to free up funding or increase the tax rate to yield the needed funding. In either case, this approach would result in taxing Detroiters today to compensate those that paid Detroit tax bills in the past.