June 9, 2026

In a Nutshell

- A change in Louisiana state law to provide for the super-priority of remediation liens allowed New Orleans’ to remediate thousands of blighted properties after Hurricane Katrina.

- The blight status of many properties was the result of a policy decision that awarded higher rebuilding grant amounts to White homeowners than Black homeowners.

- New research raises important equity concerns that should be considered if Michigan were to provide for the super-priority status of remediation liens.

Our January paper, Coordinating the Authority and Resources to Remediate Blight, examined many of the legal and financial tools available in Michigan to address blight. The research also provided a high-level look at some of the tools available in other states to deal with blighted properties, including New Orleans’ unique blight foreclosure process. The city successfully remediated tens of thousands of blighted properties in the decade following Hurricane Katrina, aided by a state law that allowed the city to use the real and perceived threat of foreclosure to administer code enforcement fines to create incentives for property owners to clean up their properties.

As Michigan considers policies to equip communities with new and expanded tools to eliminate blight, it should be noted that New Orleans’ blight foreclosure program is a powerful tool that comes with many benefits, but also some negatives. This blog takes a deeper dive into the New Orleans experience and some of the results of the city’s blight remediation efforts, including the impact of the use of “blight liens” on the sale price of a home with blight violations.

Code Enforcement Fines

One of the issues our paper identified as a shortcoming in Michigan’s blight remediation toolbox is the lack of teeth in the law to force property owners to clean up their properties. Local communities grant code enforcement officers the authority to fine individuals infringing on community ordinances dealing with property maintenance, zoning violations, and illegal dumping. If there is no remedy, the local government can bring the owner of the blighted property to court. From there, sometimes an agreement can be made about how and when a blighted property is to be improved. At other times, an agreement can be reached for the owner to sell the property on the condition that the next owner would be contractually obligated to demolish or renovate the blighted property. If an agreement is not met and the court agrees that the property is both violating the community’s ordinance and the owner of the property is noncompliant, then punitive measures (e.g., fines) can be enforced.

However, code enforcement as a blight elimination tool is only effective insofar as property owners are responsive to the threat of fees and/or the loss of their property. If property has been abandoned, the tool is not as effective as the property owner has relinquished their interest in the property.

Recent coverage of the high profile efforts to enforce blight remediation on the property being developed for a new Perfecting Church in Detroit illustrates the shallow teeth in the law. Despite the issuance of fines and orders for access by city inspectors, it has required action in the courts to encourage actions.

Louisiana Gave Blight Enforcement Laws Teeth

Blighted property was an issue before Hurricane Katrina ravaged New Orleans in 2005. Like other legacy cities, New Orleans was already struggling with population decline and a shrinking economy before the storm hit. The city’s population had dropped 20 percent since its peak in 1960. While the U.S. economy was growing from 1990 to 2000, New Orleans lost 2.3 percent of its jobs.

The number of blighted properties grew with the city’s shrinking population, reaching more than 26,000 properties before the hurricane. Blight was difficult for the city to address partly because of title issues stemming from “heir property” (i.e., property passed down over generations outside of the formal titling process). Without a clear title proving a homeowner owns the property, productive use of land can be difficult. The owner has little incentive to maintain their property or address blight, which increases the owners’ vulnerability to land loss. The blight eventually decreases property values for the surrounding community. Title issues also made assembling and rehabbing blighted properties expensive and difficult for developers and the city.

Hurricane Katrina

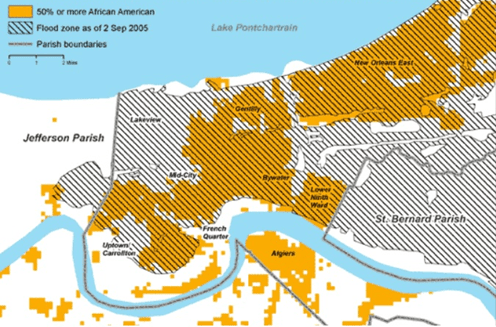

Hurricane Katrina and the subsequent flooding damaged 134,000 housing units, which was about 70 percent of the city’s occupied residential units. Decades of racial discrimination, redlining, and policy decisions that segregated residents and created unequal economic opportunity meant that almost all of the extreme-poverty neighborhoods were predominantly black. These neighborhoods were also the most likely to be damaged by Katrina. As shown in the map below, a majority of black neighborhoods were flooded after the hurricane.

Racial Characteristics of Areas Flooded by Hurricane Katrina

Source: EarthData

Rebuilding New Orleans

To help with rebuilding efforts, the federal government appropriated billions of dollars for recovery in Louisiana. Through the Road Home program, homeowners were eligible to receive up to $150,000 in compensation, and could pursue one of three options: (1) they could remain in their homes and apply the compensation toward rebuilding, (2) they could convey their damaged properties to the state and relocate to another residence in Louisiana, or (3) they could convey their properties to the state and relocate to another state. Over 85 percent of applicants chose to remain and rebuild.

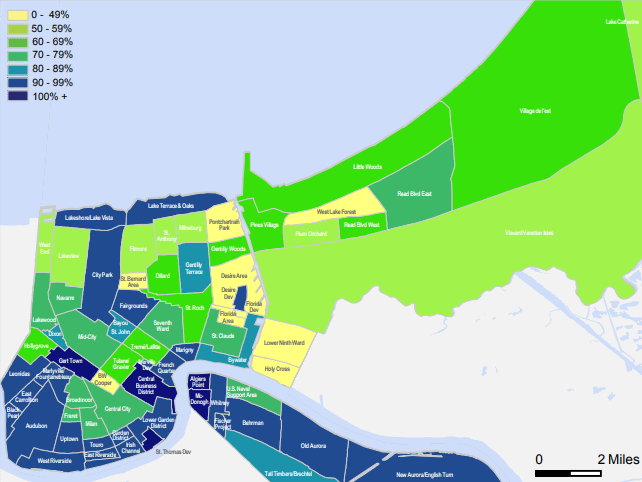

Despite an overwhelming interest in rebuilding, not all neighborhoods recovered at the same pace, as shown in the map below. This disparity can be linked to a federal policy decision to base grant amounts on the home’s pre-storm value or on the cost of repairs, whichever was less. Homes in predominantly white neighborhoods had higher pre-storm home values than homes in predominantly black neighborhoods, so white homeowners received higher grant awards than black homeowners. Reporting by ProPublica found that leaders worried about federal spending and corruption so they settled on pre-storm values as a way to keep the price tag down. Political leaders also considered “shrinking” the city’s footprint by preventing rebuilding in areas vulnerable to flooding. Those areas also happened to be where 80 percent of the city’s black population lived. Ultimately, leaders found shrinking the city to be a non-starter.

Percent of June 2005 Addresses Actively Receiving Mail in June 2009

Source: Brookings

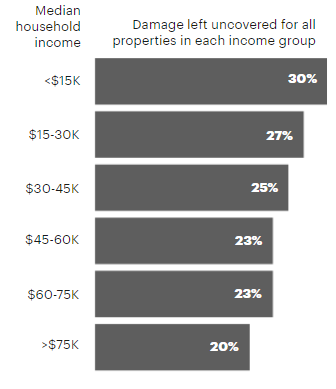

In addition to lower grant amounts, the relatively low pre-hurricane value of some properties meant that they did not qualify for funding sufficient to repair or rebuild the structures. As shown in the figure below, homeowners in neighborhoods with a median income of $15,000 or less had to cover 30 percent of their rebuilding costs after grants, FEMA aid, and insurance. In neighborhoods with median income of more than $75,000, the grant shortfall was only 20 percent.

Median Household Income and Rebuilding Grant Gap

Source: ProPublica

The large presence of heir property also made rebuilding more difficult for some homeowners and contributed to blight. Residents who owned these properties were often unable to receive state and federal aid because they did not have a clear title proving they owned the land outright. Without assistance to rebuild, many homeowners abandoned their properties. These properties represented approximately 5 to 10 percent of the city’s overall blight.

Finally, about half of the blight after the storm was concentrated in neighborhoods that experienced long-term disinvestment. Hurricane Katrina weakened these neighborhoods but blight existed well before the storm.

Blight Foreclosure

Blight in New Orleans recovered to pre-storm levels by 2019. The success of the city’s blight remediation following the storm was largely credited to its blight foreclosure process that was implemented after a Louisiana state law allowed for the super-priority of remediation liens.

Providing super-priority status to remediation liens (making them co-equal with tax liens and above mortgage liens) creates an incentive for owners or lenders to remediate the blight problems with their properties before the local governing body must step in seeking actions to remedy the violations. Local governments that have allowed for blight foreclosure can utilize the fines that result from code enforcement violations as legal leverage to gain possession over blighted properties even if there are no delinquent taxes involved.

This currently is not an option for Michigan counties because the language surrounding foreclosures in state law is narrow. Michigan can only foreclose on a property if delinquent taxes are involved. Code enforcement liens can be issued but they are often classified as inferior liens, which means that a purchaser at a foreclosure sale will have an ownership interest in a property that is heavily encumbered by the first mortgage giving the new owner little equity in the property. This makes blight foreclosure unattractive in Michigan. If, like in New Orleans, the lien that was foreclosed had superior status to all other liens, then the purchaser at the foreclosure sale takes the property free and clear of any other encumbrances, including the first mortgage.

New Orleans’ blight program was successful at getting property owners to remediate blight rather than have it taken by the city. However, there are issues with equity that must be recognized. Properties owned by low-income individuals may become blighted because they lack the resources for maintenance. The threat of blight foreclosure puts these owners at risk for predatory investors and puts the community at risk for gentrification.

Recent research on New Orleans’ blight program focused on homeowners who decide to sell their property to avoid blight foreclosure. The results suggested homeowners wishing to avoid blight foreclosure by selling their homes experience steep discounts compared to the properties’ appraised value. This concept is called the forced sale discount.

Much of the previous research on forced sale discounts studied homes facing mortgage foreclosure or tax foreclosure rather than blight foreclosure. The authors wanted to know if blight liens were a condition that leads to a forced sale discount. Their study compared properties with blight violations to similar properties without and found that the blighted properties sold at a median discount of 17 percent (mean 21 percent). Previous research found that homes sold under duress typically face a market value discount of up to 24 percent, putting the estimates from the New Orleans study in-line.

The effect of blight violations on the sale discount was most apparent in gentrifying neighborhoods (areas with stagnant median incomes, a large but declining black population, and rapidly increasing home sales) and properties resold after the first purchase, raising concerns that blight violations contribute to inequity. The study noted several limitations, including the short study period of four years.

Conclusion

Blight foreclosure was an important tool for New Orleans to remediate blighted property and rebuild the city following Hurricane Katrina. Policy decisions that awarded higher grant amounts to white homeowners than black homeowners contributed to the city’s unequal recovery and eventual blight status of many properties. While new research raises important equity questions, blight prevention and remediation has numerous benefits to neighboring residences and businesses. Given the success of blight foreclosure in New Orleans, it remains a national model for blight remediation.