March 24, 2026

In a nutshell:

- Federal tax reform removed Michigan’s personal exemption

- The Legislature wants to restore and increase the exemption

- Budget concerns could create problems

When President Trump signed the Tax Cut and Jobs Act[1] (TCJA) into law, it triggered a series of changes to the federal tax code that have the unintended consequence of altering implementation of the state income tax. Options for addressing these provisions have drawn the attention of Lansing policy makers. While some are relatively minor, others could affect state tax codes to the tune of billions of dollars if left unaddressed. One of the most notable changes in the TCJA reduces the personal exemption to zero, effectively ending it.

At the root of the problem is the fact that Michigan, like most states that levy a personal income tax, uses the federal calculation of Adjusted Gross Income as the starting point for calculating the state personal income tax. Personal exemptions claimed on federal income taxes are carried over to be claimed on state income taxes.

Thus, while elimination of the personal exemption was largely offset by an increase in the standard deduction for federal tax purposes, this change had a significant unintended consequence for Michigan taxpayers. By reducing the exemption to zero, TCJA created some confusion on how state personal income tax exemptions would be administered. Would the changes setting federal exemptions to zero carryover to set state exemptions to zero as well? Will the IRS still record personal exemptions? And if they do, will people still accurately report them? More than 8 million exemptions are claimed each year in Michigan, and the Michigan Department of Treasury reports that this keeps $1.36 billion in the taxpayers’ hands in FY2017.

Ending the personal exemption for Michigan’s personal income tax would increase the state tax burden of a typical family of four by $680. This issue hasn’t gone unnoticed. While the state’s leaders all agree the law must be changed to avoid the unintended tax windfall, the Governor, House, and Senate all have differing ideas on how to fix it. Further, each proposal uses the opportunity the TCJA presents to increase the amount of the state’s personal exemption.

Currently, for each exemption claimed on your federal tax return, $4,000 of income is subtracted from federal Adjusted Gross Income (which serves as the tax base for Michigan tax income tax returns), meaning taxpayers do not pay state taxes on that income. A $4,000 exemption equates to a $170 reduction in income tax liability ($4,000 times the 4.25 percent state tax rate).

For tax years 2017 and 2018, the personal exemption is statutorily set at $4,000. Future exemptions are indexed to inflation from the 2012 base exemption of $3,700 (i.e., the indexing will become effective once the inflation-adjusted exemption exceeds the current $4,000 level). Tax year 2019 is expected to be the first year the inflation-adjusted value is estimated to exceed $4,000. Assuming that inflation stays at about 2 percent per year, the exemption would reach $4,300 in tax year 2021.

The Governor’s proposal would slowly ratchet up the exemption floor from the current $4,000 amount to $4,500 by tax year 2021, a $200 increase in the exemption over current law estimates. The change would reduce the amount of taxes owed by $8.50 per exemption in tax year 2021, or $34 for a family of four.

Legislative leaders have different proposals. They see, the federal tax changes as an opportunity for Michigan to explore additional tax relief.

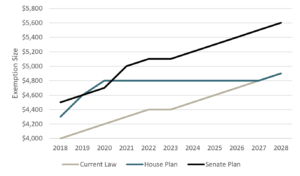

Chart 1 outlines the relative effects of the House and Senate exemption plans, compared to current law estimates.

Chart 1

House and Senate Personal Exemption Plans

Sources: House Fiscal Agency, Senate Fiscal Agency, and calculations done by CRC.

The current House plan would prescribe the exemption amount for tax years 2018 ($4,300), 2019 ($4,600), and 2020 ($4,800), with the amount remaining at $4,800 until the inflation-adjusted amount that currently exists in state law (see above) exceeds this level. Assuming inflation averages 2 percent per year, the personal exemption is likely to remain at $4,800 for almost a decade, as shown in the chart.

For tax year 2021, the House plan represents a $21.25 decrease in taxes per exemption claimed compared to current law, or about $85 for a family of four. In addition, the House plan would add a senior exemption, which would provide a $100 credit for each taxpayer age 62 or older.

As for the state fiscal impact, the House personal exemption plan would reduce income tax revenues by around $50 million in Fiscal Year (FY)2018, $150 million in FY2019, and $170 million in FY2020, compared to what would be collected if the current inflation-adjusted exemption were in place. Beginning in FY2021, the additional cost would decline as the amount of the inflation-adjusted exemption gains ground on the fixed $4,800 amount. By FY2027, there is no fiscal impact. In addition, the senior credit is expected to reduce revenues by $200 million each year starting in FY2019.

The Senate plan operates a little differently. In tax year 2018, the exemption would jump to $4,500 and would set annual $100 increases for tax years 2019 ($4,600) and 2020 ($4,700). In tax year 2021 and beyond, the exemption would be the sum of the inflation-adjusted amount in current law (again, estimated to be $4,300 in tax year 2021) and $700. For tax year 2021, the Senate plan means the $5,000 personal exemption amount would be a $30 decline in taxes owed per exemption, or $120 for a family of four.

Unlike the House plan that maintains the $4,800 exemption floor for a number of years, the Senate plan provides for annual increases in the exemption amount based on the inflation-adjusted exemption. Because the increase in the exemption under the Senate plan is greater than the House plan, the Senate plan would be a lot more costly. It is estimated to reduce state revenue by $150 million in FY2018 and nearly $200 million in FY2021, and more than $200 million each year after.

Governor Snyder and other budget hawks are worried about the costs of the House and Senate plans. And there are legitimate reasons to be concerned about the effect on the budget. A wave of existing and new budget pressures (e.g., business tax credits, the transportation funding package and reimbursements to local governments for personal property tax exemptions) will lay claim to nearly $2 billion of the $10 billion General Fund. Because the majority of income tax revenue goes to the state’s General Fund, any significant reduction related to tax reductions would primarily impact the state’s most vulnerable account. Even a $100 million revenue decline would increase pressure on the General Fund. With the current recovery closing in on the longest in the nation’s history, financial flexibility for a potential downturn is an important consideration.

Beyond the personal exemption issue, a number of possible state effects from the TCJA will affect Michigan directly, including some uncertain changes to the Corporate Income Tax, and a decline in the Earned Income Tax Credit’s growth rate (as Michigan’s EITC is tied to the federal value). While these and other changes won’t have the same magnitude of effect on the state budget as the personal exemption, there are nonetheless important considerations beyond the exemption issue.

[1] The full title of the legislation is “An Act to provide for reconciliation pursuant to titles II and V of the concurrent resolution on the budget for fiscal year 2018”