October 29, 2024

A version of this commentary appears in the Detroit News.

In a nutshell

- Real estate markets are red hot in Southeast Michigan and across the state, but this does not generally lead to increased property tax revenue for local governments.

- Farmington Hills provides an example of a city that experienced strong growth in property values prior to the Great Recession (2007-2009). Property values fell substantially during and after the recession and have still not recovered to their pre-recession peaks due in part to tax limitations that restrain growth.

- Farmington Hills has responded to constraints on its tax base by increasing the tax rate through levying multiple dedicated millages. Continually increasing the tax rate is not sustainable; we need to evaluate tax limitations and ensure that they are balanced against the need to properly fund local government.

It is summer tax time. That lovely time of year when property taxpayers get to pay large sums of money to their local treasurer’s office. Unless you’re one of the many that escrow to pay their taxes, this generally means cutting a large check.

We’re wrapping up a summer when real estate markets were red hot. In fact, one Southeast Michigan community, Farmington, was identified as one of the 10 hottest housing markets in the United States. Would it surprise you to know that these hot markets are not reflected in the bottom lines of local governments’ budgets? To better understand why, let’s take a closer look at a different community in Southeast Michigan.

Farmington Hills pre- and post-recession

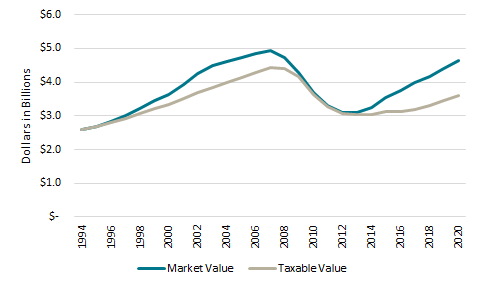

The City of Farmington Hills experienced strong growth in property values prior to the Great Recession (2007 to 2009). From 1994 to 2007, state equalized value, which is equivalent to one half of the market value of all property in the city, grew 4.7 percent per year. Taxable value, which is the value that property tax rates are levied upon, grew 3.9 percent annually. This was fairly robust growth that outpaced the 2.5 percent annual rate of inflation, as measured by the Consumer Price Index (CPI), during this period.

Property values fell substantially as a result of the global financial crises and the Great Recession. This happened in communities across the state, but those in Southeast Michigan were especially hard hit with declining property values. In Farmington Hills from 2007 to 2013, the market value of property fell 38 percent (6.5 percent per year) and dragged down taxable values by 32 percent (5.3 percent per year).

Chart 1

Property Values in Farmington Hills, 1994 to 2020

Source: Michigan Department of Treasury

As Chart 1 shows, property values started growing again after 2013. But for all of the recent growth, market values are still 6.0 percent below the peaks they reached in 2007. What’s worse, the taxable value used for tax purposes is still more than 19 percent below its 2007 peak.

Since bottoming out in 2013, market value has grown 5.3 percent per year, while taxable value has grown just 2.1 percent annually.

Tax limitations restrain growth

Prior to the adoption of Michigan’s major property tax limitations, market values drove increases in a homeowner’s property tax bill causing it to rise substantially from year-to-year. Ever-increasing property tax bills led voters to adopt the Headlee Amendment in 1978. This limitation restricted tax revenue growth on a jurisdiction-wide basis to the rate of inflation. That means that if the existing tax base in Farmington Hills grows faster than inflation, the city’s tax rate must be rolled back for everybody. This created a check on the growth of property tax collections overall, but failed to protect individual property taxpayers from excessive yearly increases driven by escalating tax base assessments.

This failure helped lead to the inclusion of a new tax limitation in Proposal A of 1994. Proposal A targeted the tax base and created a new property valuation system that limits increases in the taxable value of an individual taxpayer’s property to the lesser of inflation or five percent. Also, when property is sold, it “pops back up” to market value and annual changes are capped once again with the new owner.

These overlapping tax limitations have created a system where the only real estate change that matters is new development. The taxable value that governments levy property taxes on, is able to grow in one of three ways: 1) appreciation of existing property, 2) uncapping taxable value when properties are sold, and 3) new construction..

While the Proposal A tax limitation protects individual taxpayers from substantial yearly appreciation-related increases in their property tax bills, the Headlee Amendment takes it a step further by requiring millage rate rollbacks when properties are sold and revert back to market value. With Proposal A’s limit on increases because of appreciation, the only time property tax revenues from existing property can have more than an inflationary increase is when enough properties are sold and those “pop-ups” cause tax collections jurisdiction-wide to increase greater than inflation. However, this triggers a tax rate rollback for all of the properties in the jurisdiction.

Local governments are left with two options to overcome these strict limitations: encourage new development or increase tax rates within the allowed statutory guideposts. For communities like Farmington Hills and many others in Southeast Michigan, encouraging new development is increasingly becoming a problem because undeveloped land is running scarce.

Why hasn’t the property tax burden changed?

Faced with Michigan’s overlapping tax limitations, the question becomes: why hasn’t the property tax burden decreased?

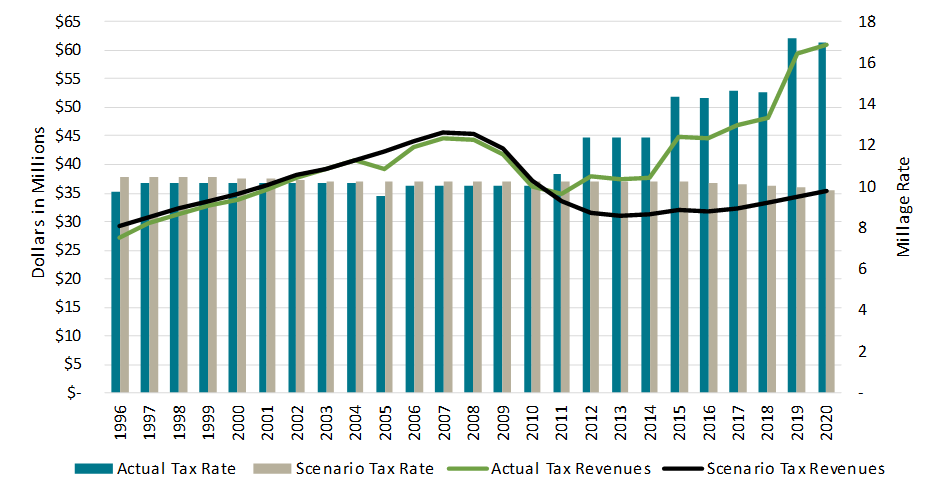

The answer lies in the one thing that local governments still have some control over – tax rates. It appears anecdotally, and Farmington Hills seems to be a good example, that the response of local governments to slow growth in property values and tax revenues has been to increase the tax rate. Chart 2 is taken from our recent report on Michigan’s Overlapping Property Tax Limitations and shows what the property tax limitations would have done to the authorized tax rate (tan bars) and tax revenue (black line) if Farmington Hills was unable to increase tax rates. The city could, and did, increase taxes as reflected by the actual tax rate (blue bars) and tax revenue (green line).

Chart 2

Property Tax Rates and Revenues in Farmington Hills, 1996 to 2020

Source: Michigan Department of Treasury, ad valorem tax reports, L-4028s and L-4029s

As the chart shows, the actual tax rate levied in Farmington Hills went from 9.8 mills in 1996 to 17 mills in 2020. This increased tax rate led revenues to increase 124 percent from $27.3 million in 1996 to $61 million in 2020. In the scenario where the city did not seek voter approval for tax rate increases (and tax rates were in fact rolled back) and growth was based solely on property value and tax limitations, revenues would have increased only 21 percent over the entire 24-year period.

This demonstrates the pressure that is put on the tax rate when the tax base is constrained. Farmington Hills is only one example of a local government that has responded to the strict tax limitations by adjusting its rates. It levied a charter-authorized operating tax and two dedicated mills in 1996. By 2020, the city was still levying the charter-authorized operating tax, but with seven dedicated millages.

This system we’ve created where local governments are increasing their tax revenues through an ever-increasing tax rate is not sustainable. Protections for taxpayers through tax limitations are important, but they must be balanced against the need to properly fund local government. Maybe that is addressed by reviewing the need for multiple tax limitations; maybe it is addressed by allowing local governments to levy more than just property taxes; or maybe it is some combination of these things.

Permission to reprint this blog post in whole or in part is hereby granted, provided that the Citizens Research Council of Michigan is properly cited.