July 22, 2026

This blog was co-authored by Jill Roof at the Citizens Research Council of Michigan and Miranda Vetter at the University of Michigan. It can be found on the Center for Local, State, and Urban Policy (CLOSUP) at the Ford School of Public Policy, University of Michigan’s Local Government COVID-19 Fiscal Strategy and Resource Guide.

In a nutshell

- Michigan’s unrestricted state revenue sharing programs, both constitutional and statutory, provide cities, villages, and townships funding rather than allow for more local-option taxes. These revenues help to fund local government services that residents rely on.

- Constitutional revenue sharing is distributed based on population and will be impacted by the decline in sales tax revenue. The extent to which the impact is shared over this fiscal year and the next depends on when a local government’s fiscal year ends.

- Methods to distribute statutory revenue sharing funds depend on a formula, and the criteria to receive funds have been modified over the past decade. These payments are conditioned on state appropriations and may be cut to help balance the state budget, as has been done in past recessions. This expected decrease in statutory payments may be permanent as previous reductions have not been restored.

Michigan’s 1,773 cities, villages, and townships (CVTs), rely on unrestricted state revenue sharing payments to supplement locally-raised revenue. Revenue sharing was adopted after certain local taxes were discontinued or preempted by the state. Today, the program consists of constitutional and statutory payments based on statutory formulas and conditioned on annual state appropriations. For some CVTs, revenue sharing comprises a significant portion of their budgets. The economic disruption and state revenue declines caused by COVID-19 will create serious budgetary strain for many local governments and impact their ability to provide services to residents.

Constitutional Revenue Sharing

Since a 1946 amendment to the state Constitution, a portion of state sales tax revenue has been dedicated to local governments to utilize as unrestricted general operating revenue. The 1963 Michigan Constitution provides that 15 percent of sales tax revenue collected at the 4 percent rate (the rate at the time) is distributed to local governments on a per-capita basis. The sales tax rate was raised to 6 percent in 1994 by Proposal A, but the revenue from the additional 2 percent is dedicated to the School Aid Fund. Decennial census rates are used to estimate the population of each city, village and township that receives constitutional payments.

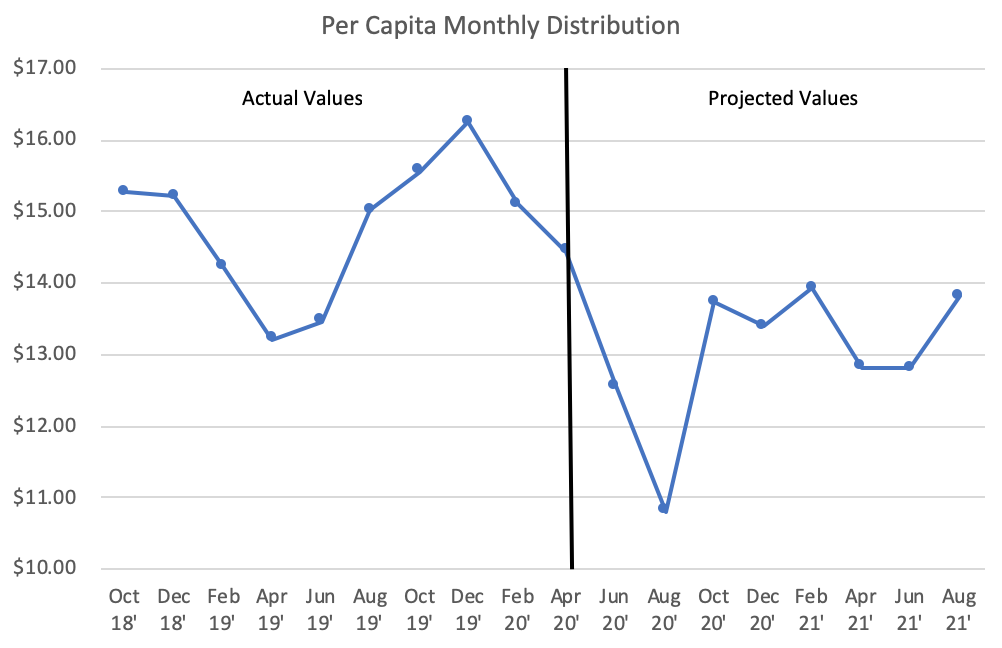

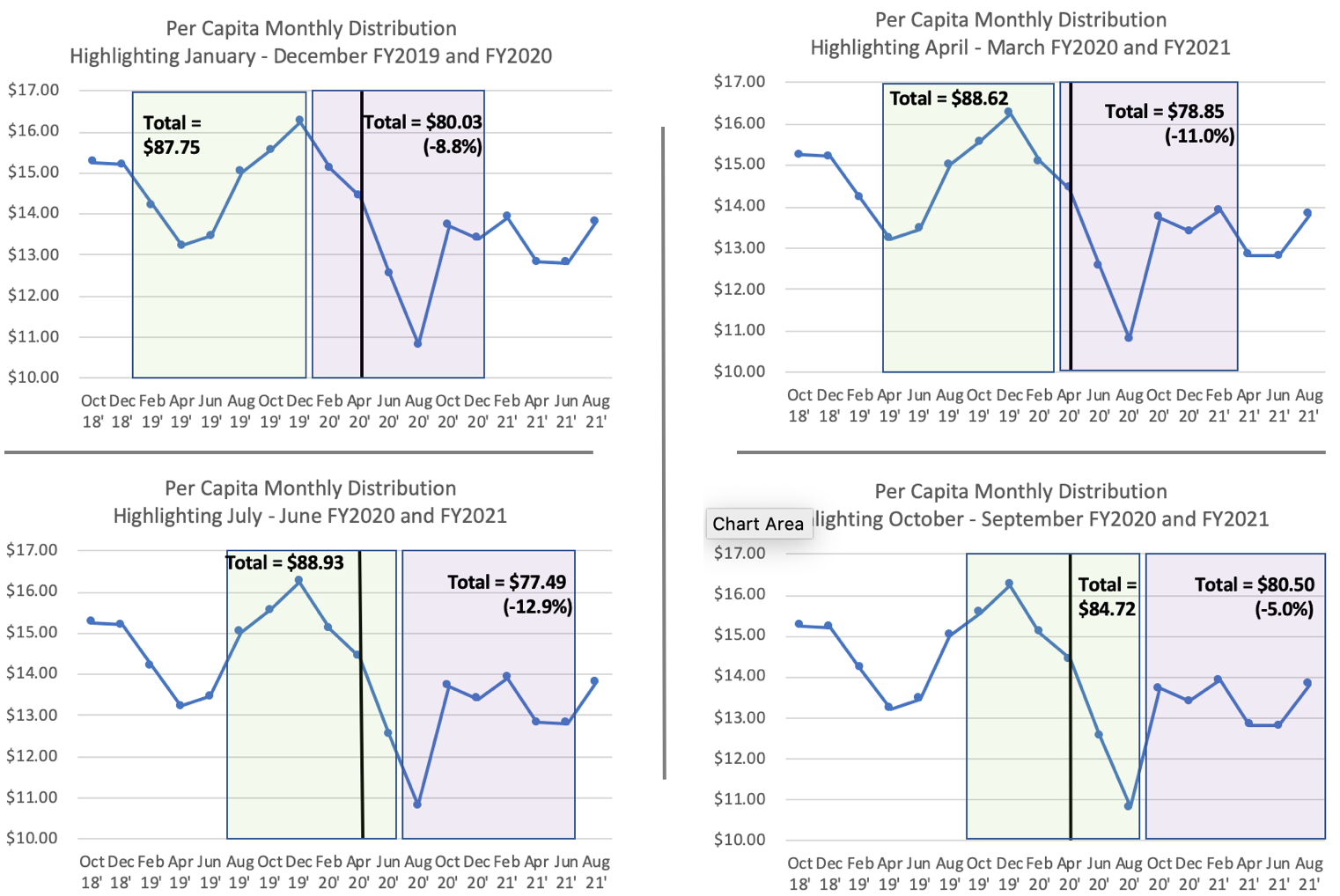

Payments to CVTs are made bimonthly, and the distribution rate is based on sales tax collections from the prior two months. For example, the June 30 payment is based on collections in March and April, the first months to see major declines in revenue. The total per-capita distribution rate for fiscal year FY2019 was approximately $86.40 per resident. The rates for FY2020 and FY2021 are expected to be less because of the decline in sales tax revenue due to the COVID-19 recession.

COVID-19 Related Impact on Constitutional Payments

Constitutional revenue sharing payment estimates depend on projections of sales tax collections for a given state fiscal year. Current estimates reflect a decrease of 11 percent in sales tax revenue for the state’s current fiscal year ending September 30, while total constitutional revenue sharing payments are expected to decrease by 2.2 percent. This difference is caused by the fact that revenue sharing payments lag collections.

Determining how the decrease will affect individual CVTs is complicated by the fact that municipalities have different fiscal years. The total amount an individual CVT receives during its fiscal year is dependent on which bi-monthly distributions are included in its fiscal year. Using calculations from SEMCOG, the graph below shows actual per-capita distributions through April 2020 and estimated payments after April based on updated sales tax revenue estimates from the May 15 Consensus Revenue Estimating Conference.

Source: Anderson, Bill. 2020. Blog: “Constitutional Revenue Sharing Reductions: Fiscal Years Matter.” Southeast Michigan Council of Governments (SEMCOG), May 19, 2020.

As the graphs illustrate, the decreased payments will affect locals’ budgets differently depending on when their fiscal year starts. Those starting in July will see the largest decrease in their FY2021 budget, compared to FY2020. CVTs with different fiscal years will see a greater decline in FY2020 and less of one in FY2021.

Additionally, because constitutional revenue sharing is distributed on a per-capita basis, CVTs with large populations will see the largest reductions. The decline will impact those units with low taxable values per capita more heavily because they cannot raise as much revenue through property taxes. Also, some CVTs with small populations rely on revenue sharing as a larger percentage of their budget than larger units that may receive a greater dollar amount.

Statutory Revenue Sharing

Statutory revenue sharing payments are based on a formula contained in state law. Less than half of CVTs receive this funding, and because of the way that cuts have been made, Detroit receives more than half of the total distribution. Since inception, statutory revenue sharing has been modified several times. The name itself has changed multiple times, and is currently known as Cities, Villages, and Townships Revenue Sharing (CVTRS). The statutory distribution formula, as well as sources of funding, have also changed over the years. Today it is funded through sales tax revenues. According to the 1998 statute, full funding would be 75.5 percent of 21.3 percent of the sales tax revenue collected at the 4 percent rate. The formula is designed to take into account the variations in local governments’ service delivery needs, infrastructure maintenance requirements, and revenue raising capacity.

However, statutory revenue sharing payments are dependent on annual state appropriations, and the formula described above was never fully implemented. The chart below shows that the state has consistently underfunded statutory payments relative to the full funding level stipulated in law. The revenue instead has been directed to finance other areas of the state budget. Moreover, since FY2011, payments have been based on a unit’s prior year payment. This means that a local government’s population, taxable property value per capita, and yield equalization from the early 2000s are still a factor in their current payments.

State Revenue Sharing, FY1981-2020 (budgeted)

Source: Michigan Department of Treasury

COVID-19 Related Impact on Statutory Payments

In FY2015, the revenue sharing program was changed in an effort to increase the number of eligible CVTs. The new program, CVTRS, eliminated criteria related to consolidating services and employee compensation as a condition of receiving payments. In FY2020, the criteria were again changed so that CVTs must have received a statutory payment in the previous year and meet requirements related to accountability and transparency in order to be eligible to receive payments. The maximum payment for FY2020 was 102.3 percent of a local unit’s combined CVTRS payments (including supplemental payments) from FY2019.

These payments are subject to appropriation risk. They are not guaranteed like constitutional payments. As the chart above illustrates, the state has a history of not providing the fully funded amount, especially during years when its own budget is under strain. The gap is so large that considering the expected decrease in sales tax revenue, even if a local government receives the maximum payment (102.3 percent of its FY2019 payment), it would still not likely reach the full amount.

Given the current pressure on the state budget, legislators may decide to decrease CVTRS payments by an amount disproportionately greater than the decrease in sales tax collections. It is worth noting that implementing a comprehensive negative supplemental bill this late in the fiscal year would be complicated. The state’s flexibility is limited because the fiscal year is three-quarters over, and making reductions in the budget now may be taking away money that’s already been spent. That being said, the state is working on the FY2021 budget, which is more likely to include additional reductions.

While the impact of the current recession is uncertain and state lawmakers have not yet made decisions on how to balance the current-year and next year’s budgets, previous decisions to balance the budget by cutting revenue sharing have had long lasting impacts. Even with expansion under the current CVTRS program, payments are still lower than they were in the early 2000s. A decision to drastically reduce CVTRS payments this year or next year could potentially have long lasting effects since current payments are dependent on prior year payments.