July 6, 2026

In a Nutshell

- Housing affordability is an issue for both renters and homeowners, but a much larger share of renters are cost burdened.

- Michigan’s Statewide Housing Plan includes the addition of 75,000 new or renovated housing units, 39,000 of which will be designated as affordable.

- The lowest-income renters may need rent subsidies to afford rent, even in affordable units.

Introduction

Affordable housing has been prevalent in the news the last couple of years and the pandemic has seemed to make some of the housing challenges even worse. Michigan was experiencing an affordable housing shortage prior to the onset of the COVID-19 pandemic in March 2020 due to long periods of low interest rates and a lack of new construction following the Great Recession. Increased home-buying and the eviction moratorium during the pandemic caused housing costs to increase by historic amounts in 2021 making affordability even more of a challenge for some Michiganders.

Michigan’s Statewide Housing Plan, released in June 2022, proposes to add 75,000 new or renovated housing units in the next five years, 39,000 of which will be designated as affordable. The addition of housing stock is essential to keep up with demand for housing, especially in places like Detroit where uninhabitable units are the primary factor driving housing stock and Grand Rapids where rental vacancy rates are historically low. However, housing remains unaffordable for many of Michigan’s renters because demand for rental subsidies is much greater than the supply of subsidies. As the data suggests, low-income households may require rental subsidies in newly constructed affordable housing.

Affordable Housing Overview

Housing affordability is measured by the share of a household’s monthly income needed to meet housing costs, which includes utilities. In general, housing is considered affordable if a household spends no more than 30 percent of its monthly income on housing costs. Households that spend more than 30 percent are considered cost-burdened, and households that pay more than 50 percent of their household income for housing are considered severely cost-burdened. Severely cost burdened households are more likely than other renters to sacrifice food, healthcare, and other necessities to pay for rent and are more likely to experience evictions.

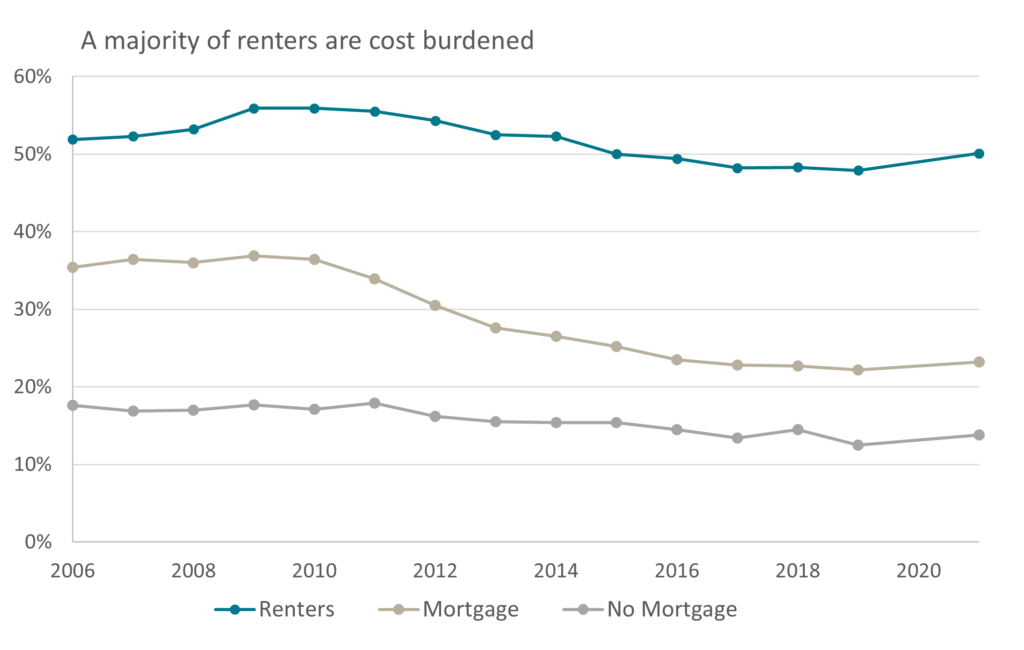

Housing affordability remains an issue for both renters and homeowners in Michigan, but a much larger share of renters are cost burdened. In 2021, the U.S. Census reported that 50.1 percent of renters in Michigan paid more than 30 percent of their household income on housing costs compared to 13.8 percent of homeowners without a mortgage and 23.2 percent of homeowners with a mortgage. Nearly a quarter of all renters experienced severe cost burden, compared to nine percent of owner households with a mortgage and six percent of owner households without a mortgage.

Percent of Cost Burdened Renters and Homeowners

Source: American Community Survey 2010-2021 1-year estimates

Rent burdens vary by community. In Saginaw, for example, over 50 percent of renters are cost burdened. In Allegan and Branch counties, just over 31 percent of renters are cost burdened.

Severe Rent Burden Impacts Lowest Income Households

The most severely rent burdened usually also have extremely low incomes. Of the renters that pay more than 50 percent of their income on housing, 72 percent had household incomes of less than $20,000 a year. For a household earning $20,000, the maximum affordable rent using the 30 percent standard is $500 per month. Units at this price are scarce: only 11 percent of all vacant units in Michigan and fewer than 10 percent of occupied units rented at that rate or less.

At the root of the affordable housing issue is that the cost of building and maintaining housing is more expensive than low-income households can afford. Nationally, the average operating cost of a rental unit is just over $439 per month, excluding mortgage and other debt-related expenses. In 2021, the Housing Michigan Coalition provided sample project costs for various residential buildings. For example, a new traditional single-family home costs around $300,000 and a suburban apartment complex with 40 units costs north of $7 million, with units commanding $1,000 per month in rent.

Tax Credits Do Not Always Make Units Affordable

The mismatch between what renters can afford and what can be feasibly built is often addressed by granting federal tax credits to developers to lower the cost of developments in exchange for a certain amount of housing being reserved for low-income tenants.

The federal Low Income Housing Tax Credit (LIHTC) program administered by the Michigan State Housing Development Authority (MSHDA) provides property owners with a federal income tax credit for up to 10 years. The credit rate stays constant throughout the 10-year period, but varies across LIHTC developments depending on when construction occurred and the prevailing interest rate at that time. Since developers need upfront financing to complete construction, they typically sell their tax credits to outside investors (like financial institutions) in exchange for equity financing. The equity reduces the financing developers would otherwise have to secure and allows tax credit properties to offer more affordable rents.

There are two types of LIHTC credits: a nine percent credit that is generally reserved for new construction and a four percent credit that is generally used for rehabilitation projects using at least 50 percent in federally tax-exempt bond financing. The nine percent credit is intended to subsidize up to 70 percent of the low-income unit costs in a project and the four percent credit is intended to subsidize up to 30 percent of the low-income units in a project. To receive the tax credit, the owner must reserve either: 1) 20 percent of the units for residents whose incomes do not exceed 50 percent of area median income (AMI); or 2) 40 percent of the units for residents whose incomes do not exceed 60 percent of AMI. Area median income is determined by the U.S. Department of Housing and Urban Development (HUD).

The amount of rent the owner can charge low-income tenants is not based on the tenant’s actual income. Instead, the maximum rent for those units can be 30 percent of the AMI for the imputed (not actual) family size. Family size is imputed based on the number of bedrooms in the unit. The imputed family size for units with at least one separate bedroom is 1.5 per bedroom. For units without a separate bedroom, the imputed family size is 1. For example, the maximum allowable rent for a two bedroom unit is calculated based on the imputed household size of three persons (1.5 persons for each of the bedrooms). If 50 percent of the AMI for the imputed household size of three is $20,000, for example, the maximum allowable monthly rent for a two bedroom unit will be $500, regardless of the actual household income or family size.

Since maximum rents in LIHTC properties are not based on actual household income, many tenants in tax credit affordable units also rely on rental subsidies. In Michigan in 2019, just over 60 percent of tenants in tax credit properties surveyed received some type of rental assistance. While the LIHTC program has made units affordable for some renters, over 26 percent of tenants living in Michigan’s LIHTC units are still paying more than 30 percent of their income on rent.

Michigan’s Affordable Housing Laws

Michigan’s affordable housing strategy has included tax abatement tools for local governments to encourage the development of affordable workforce housing. Workforce housing is affordable to households earning between 60 to 120 percent AMI.

The Attainable Housing Facilities Act provides tax abatements to owners of rental properties with four or less units that have been rehabilitated or are newly built in an attainable housing district. If the property is rehabilitated, owners must spend at least $5,000 to bring it into conformance with minimum local building code standards for occupancy. Under the Act, the property is exempt from ad valorem property taxes, except for the land, and instead is subject to an attainable housing facilities tax that is calculated at half of the statewide average tax rate on commercial, industrial, and utility property, as determined by the state board of assessors. To receive the tax abatement, the property can consist of no more than four units, and at least 30 percent of the units have to be rented to a household with a combined annual income of 120 percent or less of the county median income. Additionally, the rent cannot exceed 30 percent of the household’s “modified household income,” as defined in the Act. The exemption lasts from one to 12 years, as determined by the local government. The Residential Housing Facilities Act is similar, but applies to rentals with four or more units and requires an investment of at least $50,000.

A 2022 amendment to the Neighborhood Enterprise Zone Act allows any city, village, or township to designate neighborhood enterprise zones (NEZ), but only if the zone is adjacent to existing development, can use existing infrastructure, has access to water and sewer services, and contains five or more residential units per acre. A 2022 amendment to the State Housing Development Authority Act allows local units of government to offer payment in lieu of tax (PILOT) agreements for residential development or rehabilitation.

The new tax abatement tools, similar in concept to the LIHTC model, improve the LIHTC model because rent is capped at 30 percent of the household’s actual income rather than a set amount based on the county-wide AMI. This should keep rents affordable to qualifying households. However, for many households with incomes at 120 percent AMI, housing is already affordable. For example, in Kent county, where Grand Rapids is located, the 120 percent AMI for a two-person household is $85,920. The average two-bedroom rent in Grand Rapids in December 2022 was $1,133, much less than the household’s maximum affordable housing costs of $2,148. Households making 60 percent AMI are closer to the edge of affordability. The 60 percent AMI for a two-person household in Kent county is $42,960, putting the household’s maximum affordable housing cost at $1,074. The average two-bedroom rent in Grand Rapids in December 2022 is unaffordable to these households. Even though the one-bedroom average rent of $918 is technically affordable, high utility bills could push the household over the affordability edge. Further, a one-bedroom unit may not be appropriate for all two-person households.

The new tax abatements may encourage the development of rental housing leading to lower prices as housing stock increases. It remains to be seen if the tax abatements make rental developments feasible for households making 60 percent AMI or less.

Demand for Rent Subsidies is Greater than Supply

Rental subsidies, provided through the federal Housing Choice Voucher (HCV) program, is the main way affordability is addressed for the lowest-income households. One benefit of the voucher program is that the rental subsidy is based on the household’s actual income, so a family generally pays no more than 30 percent of its income on rent. The voucher is successful at providing affordable housing to the lowest income households because housing authorities are required to provide at least 75 percent of its voucher to rental applicants with “extremely low-incomes,” defined as an income that does not exceed 30 percent of the area median income. Median income levels are published by HUD and vary by location and household size. For example, the extremely low-income limit for a one-person household in both Kent County and Wayne County is $18,800 compared to $13,550 in Branch County. Notably, income limits are only used for eligibility at admission to the program, and participants continue to receive a subsidy as their incomes increase. The subsidy generally declines by 30 dollars for every 100 dollars added in income. Once the voucher subsidy is at zero for six months, the family is no longer eligible for the program.

Unfortunately, the demand for rental subsidies greatly outpaces the supply. According to estimates by MSHDA, the state housing authority with 28,000 housing vouchers, approximately 64,000 households are on the HCV waiting list. Thousands of other households might qualify, but the waiting lists are closed.

Conclusion

Michigan has an affordable housing problem. The plan to add 75,000 new or rehabilitated housing units to increase the overall supply of housing should help reduce some of the price increases experienced as a result of home buying and demographic trends. The question is if building 39,000 affordable housing units would be effective at alleviating housing affordability issues in Michigan. As the data indicates, Michigan’s most severely burdened households are unlikely to afford rent without rent subsidies, even in affordable units created through tax credits. The new tax abatement tools require rents to be affordable based on actual household income; it remains to be seen if developments with rents affordable to the lowest-income households are feasible. Tackling affordable housing may require policymakers to consider policies that make rent more affordable for the lowest-income renters.