July 27, 2026

In a nutshell

- Every March, the Mayor of Detroit proposes to City Council a budget for the upcoming fiscal year and a forward-looking four-year financial plan. Council may amend the mayor’s proposal before adopting the budget.

- The budget process is informed by a comprehensive planning process that gathers and evaluates priorities from departmental, procurement, grant, staffing, technology, capital, long-term financial, and community insights.

- Detroit’s budget process is unique in the sense that it involves an extra step of review by the Financial Review Commission (FRC) before the new fiscal year begins on the first of July.

Detroit’s Annual Budget Process

The Mayor of Detroit oversees preparation of the city’s annual budget, covering administrative departments, service delivery operations and policy priorities. Every March, the mayor proposes an annual budget and a four-year financial plan to the Detroit City Council. Council may amend the mayor’s proposal before adopting the budget.

On March 7, Mayor Duggan proposed his FY2023 budget and the four-year financial plan (FY2023-FY2026) to council, setting off a weeks-long process that will eventually lead to council approval of the budget. The state-appointed Financial Review Commission (FRC) is required to review the budget before it takes effect.

Between March 7 and April 14, the city council held budget hearings that informed revisions or amendments to the budget based on departmental, agency, and community input. On April 14, city council voted on the budget and on April 21 the mayor will approve or veto all or parts of the budget. The enacted budget is then sent to the Financial Review Commission on May 7 to be reviewed before the new fiscal year begins on July 1, 2022.

It is important to note that the specific dates of when city council votes on the budget, when the mayor approves or vetoes the budget, and when the budget is sent to the FRC differ year to year. However, these steps in the budget process occur around the same time each year, as summarized in the timeline presented here.

The budget process is informed by a comprehensive planning process which includes various parties and interests. The final budget is developed by evaluating considerations and priorities from departmental, procurement, grant, staffing, technology, capital, long-term financial, and community insights.

Key Documents and Legal Requirements

Two primary documents describe city government financial operations. The budget is a planning document that is adopted before the start of the fiscal year. It is based on the department structure and includes projections of revenues and appropriations for expenditures for each department and item funded by the city.

The Comprehensive Annual Financial Report (CAFR), required under state law, reports actual revenues and expenses and must be published within six months of the fiscal year end. The CAFR reports the actual financial result of the fiscal year activities – whether there is a surplus or deficit in each fund, where resources came from and for what purpose they were used. If there is a deficit in any fund, state law requires that a deficit elimination plan be developed and submitted to the Michigan Department of Treasury.

As a condition of the 2014 bankruptcy’s Grand Bargain, state law requires Detroit to implement fiscally responsible practices. That includes facilitating independent biannual revenue estimating conferences designed to establish a data-driven fiscal foundation for revenue estimates that are used for subsequent budget decisions. These conferences provide city officials with information to make decisions that will keep the city solvent and help maintain balanced budgets. This practice has empowered the City of Detroit to project informed and conservative economic forecasts that inform the development of the budget and the city’s four-year financial plan.

Appropriations are a central part of the city budget. An appropriation is an authorization to spend money from designated funds. The city’s funds include the general fund, enterprise funds, grant funds, and other restricted funds which are used for specific purposes. City council approves the amount for each appropriation to cover the 12-month fiscal year, and is responsible for approving appropriation changes if they become necessary. The budget is ultimately a list of those authorized amounts.

Once a budget is adopted, the sum of the approved appropriations is used as a baseline to develop the four-year financial plan. The purpose of the four-year financial plan is to provide forecasts showing expected future spending amounts against the projected revenues available.

A handful of requirements are imposed by state law and local ordinance on the budget. First, the total estimated expenditures may not exceed the total estimated revenues, including any available unappropriated surplus . Also, the city must adopt a financial plan covering the upcoming fiscal year and the next three fiscal years that include elements established by law, projecting balanced revenues and expenditures for each year .

The city’s financial plan should rely upon revenue projections based upon reasonable and appropriate assumptions which are estimated through statutorily prescribed revenue estimating conferences that establish forecasts of anticipated revenues. Lastly, the city’s CFO must certify that the city’s annual budget complies with the Uniform Budgeting and Accounting Act.

Role of the Financial Review Commission

Detroit’s budget process is unique because it involves an extra step of review before the new fiscal year begins on July 1. This extra step of review is provided by the Financial Review Commission (FRC) that was created in 2014 to monitor city compliance with the Plan of Adjustment, providing oversight of city financial activities.

The Plan of Adjustment represented a critical step toward the city’s rehabilitation and recovery from a decades-long downward spiral. The plan provided relief of up to $18 billion in secured and unsecured debt, and offered recoveries for the city’s creditors while simultaneously allowing for meaningful and necessary investment in the city.

The FRC is responsible for oversight of the City of Detroit, the School District for the City of Detroit (DPS), and the Detroit Public Schools Community District (DPSCD). For each governmental entity, the FRC ensures that it is meeting statutory requirements, reviews their budgets, and establishes programs and requirements for prudent fiscal management.

The FRC’s oversight of the city will last no less than 13 years. As the city met certain criteria, however, the nature of the oversight has been scaled back. In 2018, the City of Detroit was relieved of direct state financial oversight from the Financial Review Commission as the panel granted the city its first waiver of active oversight, marking the end of direct state oversight of Detroit’s finances and management. This direct oversight gave the FRC the power to veto city budgets and certain contracts, serving as a check on the mayor and city council.

Even though the city is no longer bound to direct state financial oversight from the FRC, at any time during its tenure, active oversight could be reactivated should the city’s municipal finances sink back into the years of deficits that prompted the financial emergency in 2012. The FRC continues to monitor the city and reviews the waiver annually. By July 1 of each fiscal year, the FRC makes a determination as to whether to renew the waiver for the subsequent year.

Since the creation of the FRC, the panel has not had to intervene or provide any modifications to the city budgets.

Surpluses and Deficits

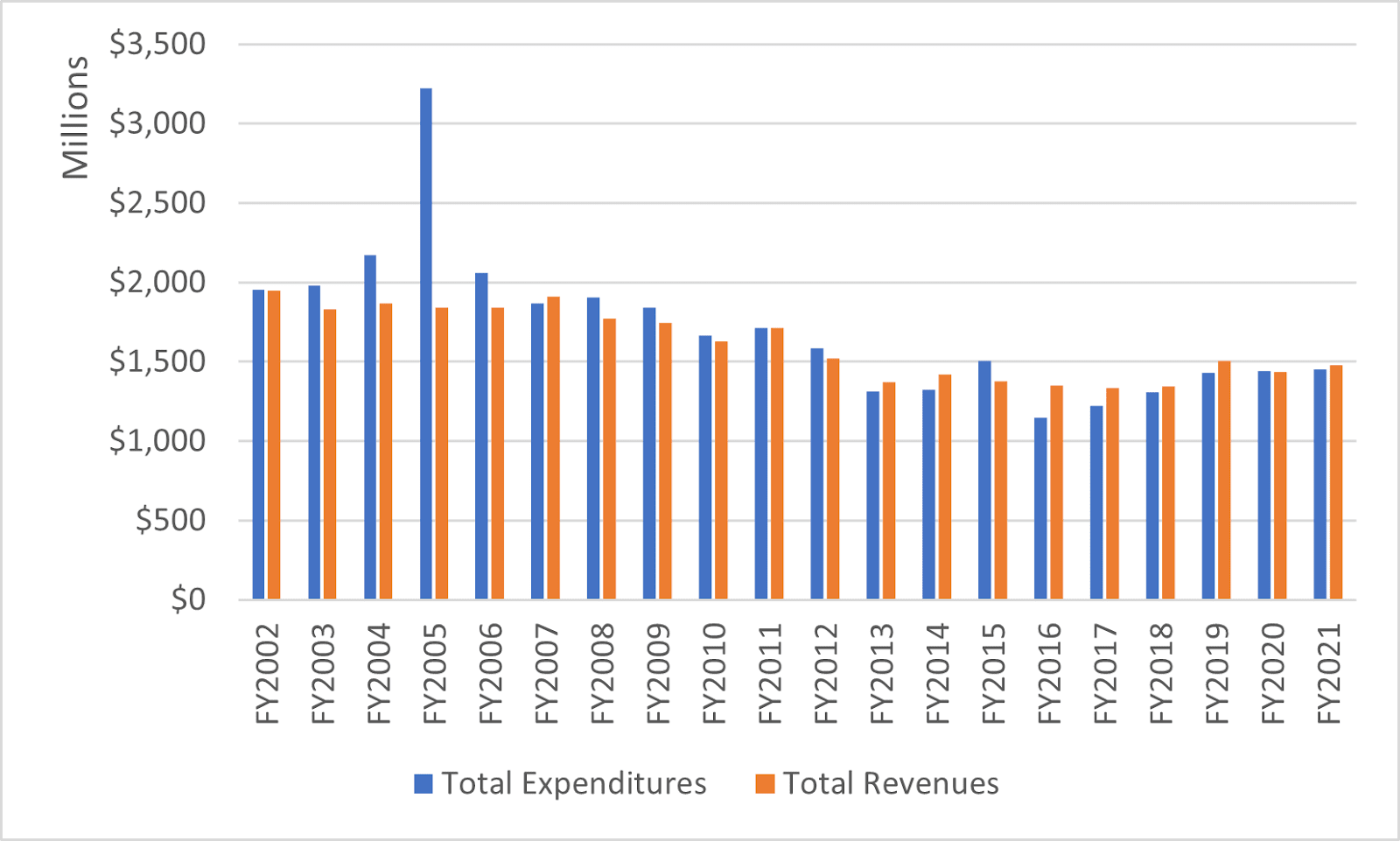

Between FY2002 and FY2012, Detroit’s expenditures often exceeded revenues. From FY2013 to FY2021, the city was generally able to turn around that trend. City revenues were sufficient to cover spending during most of these years with the exception of FY2015 and FY2020. Below is a chart showing Detroit’s total revenue and expenditure trends by fiscal year, highlighting budget surplus and deficits from FY2002 to FY2021.

Detroit’s Total Revenue and Expenditure Trends, FY2002 to FY2021

Source: City of Detroit OCFO – Office of Budget

The city saw the worst operating deficit of almost $1.4 billion in FY2005 due to massive amounts of payments made to the General Retirement System Service and the Police and Fire Retirement System Service Funds.

The FY2023 budget continues a trend the city has started since the Plan of Adjustment in 2014; and that is a sensible balanced budget that is conservative, practical, and responsible. It has been lauded as a “return to normal” budget restoring the pre-pandemic status quo and managing risks with contributions to reserves and spending restraint.

The Citizens Research Council’s Detroit Bureau will be publishing an in-depth budget analysis of Detroit’s FY2023 budget in the coming weeks. Stay tuned for that report.