February 24, 2026

In a Nutshell:

- The fiscal consequences of the Headlee Amendment and Proposal A, Michigan’s two landmark constitutional property tax limitations, continue to challenge local governments that are heavily reliant on property tax revenues.

- Local Governments are supporting a change in law to allow millage rates that were reduced under the Headlee Amendment to be reinstated without voter approval (known as a “Headlee rollup”). They best begin with a review of the original intent of the Headlee Amendment as well as a legal assessment.

- State and local policymakers should launch a deliberate and comprehensive review of Michigan’s local government fiscal system. Establishing a state-level expert-supported commission to examine overall local funding challenges, including the impact of Headlee millage limitations will go a long way to identify durable reforms that benefit both local governments and taxpayers.

Local governments continue to face fiscal consequences of two landmark property tax limitation constitutional amendments without a strategy to address their faults. Of particular interest is the authority to increase millages reduced under the Headlee Amendment to the Michigan Constitution.

The 1978 Headlee Amendment sought to limit accelerating property tax burdens in Michigan. Voters subject to high inflation, accelerating growth in property values, and expanding government services, moved to check local revenue growth by enacting controls on public spending, taxation, and revenue growth. The amendment limits property tax revenue growth in local governments by requiring adjustments to property tax millage rates. However, even with these restrictions, individual property owners remained dissatisfied with their level of tax relief. Fifteen years later, when reforms were adopted to Michigan’s school finance system in Proposal A, voters approved a supplementary limit on the annual growth of the assessed value (the tax base) of each parcel of property.

It would have been difficult to anticipate how these two historical property tax limitations would work in practice and how they have affected local government property tax revenues. New laws, legal opinions, and economic experience may have altered what the original impacts of the Headlee Amendment and Proposal A were expected to be.

If policymakers have the will, taking steps to review legislative intent, examine economic and social impacts, debate various solutions, and revise laws to address what may or may not be working for local government funding now, would build trust from taxpayers and avoid potentially costly litigation.

Reinstating Headlee Rollups

On the horizon is an often-debated arcane issue of discontent with Article IX, Section 31 of the Michigan Constitution (part of the Headlee Amendment). While complex, it is one to which local government officials and watchful taxpayers alike pay attention.

Local government advocates wish to pursue changes to a sometimes-significant aspect of the law dealing with millage rate calculations. The component in most dispute is to allow what is known as a “Headlee rollup.” A “rollup”refers to when local governments can raise a previously reduced millage rate (that had been subject to a rollback) without additional voter authorization.

Consider this example. County A was levying its maximum authorized millage rate of five mills ($5 of tax for every $1,000 of taxable value) in Year 1. Its property tax base of $100,000 grew greater than the 5 percent inflation to $120,000 in Year 2. The county would have to reduce its millage rate by 0.625 to 4.375 mills. The automatic rate reduction limits County A to an inflationary annual increase in government-wide property tax revenues using its higher tax base in Year 2.

If the tax base grows at the rate of inflation in Year 3, County A has lived within the intent of Section 31 of the Headlee Amendment. But what if the tax base grows slower than the rate of inflation? From the initial implementation of the Headlee Amendment (1980) to 1993, local governments were able to reinstate millages that had been reduced from levels originally authorized to still yield inflationary annual increases.

Expanding on the example above, County A would not be able to collect 5 percent more in property tax revenues in Year 3, if inflation was 5 percent and the value of its property tax base remained at $120,000. To collect the allowable inflationary increase in government-wide property tax revenues, County A would have to raise (rollup) its millage rate by 0.219 mills. The increased millage rate in Year 3 of 4.375 would still be lower than County A’s former maximum authorized millage rate of 5 mills.

That ability to roll up, or reinstate, millages ended with enactment of 1993 PA 145. The formula to calculate millage reductions was changed to prevent any automatic (non-voter-approved) rollups in the previously voter-approved millage rate. Although a local government could seek approval from voters for a new millage or a “Headlee override” – a vote of the residents to return the rolled-back tax rate to the previously authorized rate, this elimination of Headlee rollups has exasperated local government officials as this added another challenge to managing property tax revenue.

The reinstatement of Headlee millage rollups continues to be a policy priority for many local government officials. They suggest that allowing Headlee rollups will help them better manage their property tax revenues. Moreover, because the repeal of the tax rollup mechanism was accomplished through a statutory amendment, advocates contend that a simple repeal of that prohibition in the General Property Tax Act could reinstate rollups. The proposed amendment to the General Property Tax Act would change the millage reduction formula amended in the 1993 statute.

A word of caution, however. During the period when Headlee rollups occurred, there was significant debate about whether this practice complied with the original intent of the constitutional amendment. Some believed that because voters had initially approved and authorized the maximum property tax rate, that millage rollups merely raised rates within that prior authorization. Others argue that when voters adopted Headlee, they intended that no increase in property tax rates could occur after 1978 without an affirmative vote of the residents. This debate about whether Headlee rollups should occur automatically continues today. While there has been some legal activity, the issue of whether millage rollups can occur without voter approval remains unsettled.

Rate and Revenue Impacts

The issue of reinstating Headlee rollups is not only about whether they were originally intended or not, but it is also about how this provision affects local government finances. The rollup issue remains on the local government policy agenda because it impacts property tax revenue growth. The interactions that occur when both the Headlee Amendment’s revenue and tax limitations and the assessment cap adopted in Proposal A apply are complicated.

In a thorough retrospective examination completed in 2021, the Research Council reviewed how the two property tax limitations affected property assessments, tax rates, and revenue growth. This study found the following:

- In the years after the Great Recession (after 2009), property tax revenues in communities experiencing low property value growth did not keep up with the rate of inflation. The drafters of the Headlee Amendment noted that they intended to keep property tax revenues from existing property from increasing more than the rate of inflation (unless voters approved a rate increase). However, it is not clear whether they intended for a local government to recover rolled back millage rates when property tax revenue growth did not keep pace with inflation.

- The relationship between property tax values and revenue collections is diminished due to the use of “taxable value” for determining property taxes owed on a parcel of property.

- In communities where the property tax base has contracted, local governments have sought tax rate increases to maintain existing revenues and/or to support new services, often leading to higher property tax rates overall.

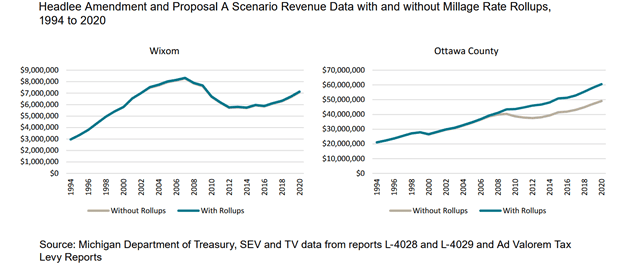

The report analyzed what the impact on property tax revenues for a few communities would have been, had millage rates been rolled up during 1994-2020. The impact differs significantly by community, but it is illustrative. Two charts below illustrate the range of how rollups would have affected two communities: the City of Wixom and the County of Ottawa. In Wixom, rollups would only have increased tax revenues by 0.6 percent since the area’s tax base kept up relatively well with inflation. In Ottawa County, the tax base did not keep pace with inflation. Tax rate rollups would have allowed tax revenue to keep pace with inflation, thus avoiding an 11.2 percent decline in tax revenue.

Overall, had rollups been allowed, local governments would have collected more tax revenues. However, the impact is not as significant as local governments might have anticipated given the impact of the assessment cap adopted during Proposal A. The use of taxable value, rather than state equalized value, which was used prior to 1994, tempers the impact rollups would have had.

Legal Landscape

Local governments have expressed their interest in authorizing Headlee rollups in the future by changing 1993 PA 145. Before taking that step, it would be valuable to revisit the legal journey of Headlee rollups as a statutory fix could be challenged as unconstitutional.

Prior to the adoption of 1993 PA 145, there was no consensus that rollups were within the law. The prosecutor in Macomb County opined in 1991 that the formula adopted in statute (MCL 211,23d) was unconstitutional because it allowed an increase in the tax rate mathematically, without voter approval. He concluded that the language violated Article IX, Sections 25 and 31, of the 1963 Michigan Constitution.

However, following that opinion in 1992, in the case Macomb County Taxpayers Association vs. the Utica Community School District, (File 91-3755-CZ), the Macomb County Circuit Court June 29,1992, ruled in favor of the Utica Community School District as follows:

For these reasons, the Court holds defendant may raise its maximum allowable millage pursuant to the implementation legislation without voter approval and without violating the Headlee Amendment provided the maximum allowable millage levy does not exceed the maximum authorized millage rate.

The issue became moot in the courts. While the appeal was being considered in the Michigan Court of Appeals the state legislature amended the General Property Tax Act to disallow Headlee rollups moving forward (July of 1993 – see above).

The 1993 elimination of rollups was not legally challenged as depriving local governments of the ability to carry out actions formerly deemed part of the tax limitations’ intended implementation. However, affirmation of the original intent of the voters to require approval of property tax rate increases has been documented in other venues.

During the same period that policymakers were debating school finance reforms, the Headlee Blue Ribbon Commission was examining any emerging issues resulting from the implementation of the Headlee Amendment. In its 1994 report, the Commission addressed the issue of Headlee rollups directly. The report’s findings emphasized the intent of the original Headlee amendment to permanently limit property taxes.

Findings and Recommendations

The Commission finds that the voters, in adopting the “Headlee” amendment, clearly desired to limit property taxes, permanently reduce that limit when assessments on existing property grow faster than the rate of inflation and require voter approval for any increases above that limit. The allowance of a non-voted “rollup” in the “maximum authorized rate” of property taxation is contrary to the constitution, and section 34d of the General Property Tax Act should prohibit any increase in the maximum authorized rate without a vote of the people. In addition, any ballot question requesting “voter approval” of taxes under the Headlee amendment must be clear about what taxes are actually being authorized. A “renewal” question cannot authorize an increase above the previous maximum authorized rate, as reduced by the Headlee amendment.

The Commission applauds the sections of 1993 PA 145 that prohibit Headlee “rollups” and misleading property tax ballot questions.

(Headlee Blue Ribbon Commission Report, September 1994, page 32)

The Drafters’ Notes to Proposal E of 1978 also addressed this issue, “It does not allow “rolled % back” rates to be increased under any conditions without voter approval.”

From this history, it is clear that there are differing perspectives on the constitutionality of Headlee rollups. From one viewpoint, the millage rollup is recapturing a previously voter-authorized millage rate. From another viewpoint, the millage rollbacks were a legally required check on local government revenue growth, and a rollup without voter approval would allow a local government to increase taxes without express authorization.

Deliberate Examination

A statutory reinstatement of rollups will not get at the fundamental challenges in the state’s current property tax and local government funding system. More should be done to address the dynamics at play.

To avoid what is sure to be a short-sighted pursuit – a legislative fix to reinstate Headlee rollups –policymakers should consider a more impactful path to address local government fiscal concerns about the Headlee Amendment and Proposal A. It is certain that if the state legislature successfully adopted an amendment to the General Property Tax Act allowing local governments to roll up previously authorized millage rates, it would only beg a constitutional challenge. Such a course of action would not only cost local governments valuable time and resources, but it would also erode taxpayer trust. This process would not lead to better local tax and fiscal policy.

A first step to consider is a request for an opinion from the Michigan attorney general on the constitutionality of Headlee rollups prior to any bill introduction. A state legislator could request that the attorney general review whether the law that prohibited Headlee rollups in 1994 concurred with the original intent of the amendment, and of the voters who approved it. A proactive legal review will inform the legislature what specific steps to take should they want to proceed with a statutory amendment.

There is another more thoughtful and comprehensive approach to consider. Given the broad reach and complex legal and economic interrelationships between the different property tax limitations of Headlee Amendment and Proposal A, policymakers could establish a state-level commission to evaluate Michigan’s overall local government finance system.

Having a well-defined, expert-supported state-level commission to deliberate and examine improvements in how Michigan funds its local governments would be a worthwhile effort. And if effective in developing comprehensive changes and updates to local government funding, lead to durable change. The structure of property taxes, revenue sharing, and state aid are complex and the interplay between constitutional and statutory provisions are complicated. Discussion external to a legislative process would be a constructive way to examine what is and is not working, including tax limitations and millage rollups, and a venue where effective recommendations can be offered.

The Research Council has often called for comprehensive municipal finance reform. By addressing local government finance issues deliberately and comprehensively, state and local policymakers will be able to identify and pursue root reforms that will benefit both taxpayers and local governments. Finally, the reforms identified by such a commission could inform proceedings of a future Constitutional Convention should Michigan voters successfully call for one in 2026. Recommendations affecting local government financing and their taxing authority could be addressed during constitutional convention proceedings.

If policymakers consider taking action as suggested above, perhaps the tangled issues of Headlee rollups, the unintended impacts of the Headlee Amendment, Proposal A, and local government fiscal reform could be resolved.