June 9, 2026

In a Nutshell:

- More than 40 percent of adults in the United States have some form of debt resulting from unpaid medical bills.

- Existing efforts – such as one-off debt forgiveness and minimum federal regulations – do not go far enough to protect people from the negative consequences of medical debt.

- States have laws on financial assistance policies, billing and collection practices, limitations on lawsuits, and reporting related to medical debt, but Michigan has not enacted any of these policies.

Despite improvements in health care coverage over the last 15 years, many people still find themselves uninsured or on a plan with significant out-of-pocket costs. When large medical bills hit, even those with coverage are not always able to pay providers on time, leading patients to fall into medical debt. This debt has negative consequences for patients’ financial, physical, and mental well-being.

Recent efforts to regulate and eliminate medical debt have made headway, but the state can do more to limit the impact of medical debt on patients who are unable to cover the costs of their necessary care.

Medical Debt in the United States

More than 40 percent of adults in the United States have some form of debt resulting from unpaid medical bills. This medical debt can take a variety of forms, such as unpaid bills, payment plans with providers, credit card bills, money owed to a third party who purchased the debt, or money borrowed from friends and family.

Unsurprisingly, people with lower incomes are more likely to have medical debt (57 percent of adults in households making under $40,000 have medical debt), but higher income households are not immune (26 percent of adults in households making more than $90,000 have medical debt). As expected, those under 65 without insurance have higher rates of medical debt (64 percent) than those with insurance (44 percent), but coverage itself clearly does not prevent people from getting behind on medical payments. Black (56 percent) and Hispanic (50 percent) adults are more likely to be affected, but White adults (37 percent) face medical debt as well. The share of adults with medical debt is highest in the south (48 percent), but the Midwest (41 percent) is ahead of the northeast and west regions (both 35 percent).

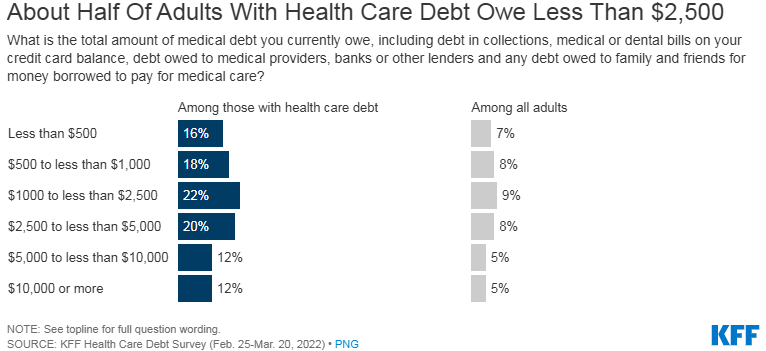

The size of medical debt varies, with 16 percent of people with medical debt owing less than $500 and 56 percent owing less than $2,500 in total medical debt. Twenty percent of people with medical debt own between $2,500 and $5,000, with the remaining 24 percent owing $5,000 or more.

Thirty-three percent of people with medical debt believe they will pay it off within a year, 48 percent believe it will take one to six years, and 18 percent believe they will never pay it off.

Medical debt leads people to cut back on spending and delay purchases, deplete savings, and take second jobs or additional hours, among other efforts to cover the cost. Those with medical debt are often contacted by collection agencies and deal with reductions in credit scores, but medical debt can also lead to legal action, eviction, and bankruptcy. Among those with medical debt, 15 percent of adults said they had been denied care due to their medical debt and 61 percent reported that they skipped or delayed care or medication due to the cost, which has consequences for their physical and mental well-being.

State-level data is not available for the broadest definition of medical debt, but there is state-level data on debt in excess of $250 owed specifically to providers or collection agencies (i.e., excluding debts accumulated using general borrowing tools like credit cards and personal loans, debt owed to family and friends, and any medical debts below $250). The percent of adults with this kind of medical debt in Michigan (9 percent) is above the national average (8 percent), which is similar to Ohio and Wisconsin, but lower than Illinois and Indiana.

The conclusions drawn from the broader definition related to who is more likely to have medical debt, the size of medical debt, and the impact of medical debt all remain present when looking at this narrower definition.

Recent Steps to Address Medical Debt and Their Limitations

While utilizing debt as a way to pay for valuable goods and services is not inherently problematic, medical debt is distinct from other kinds of consumer debt, as medical bills are less discretionary than other kinds of purchases that typically lead to debt, such as mortgages, car loans, and student loans. The primary reason is that medical care is often necessary and time sensitive, meaning that patients cannot necessarily delay expensive care until they can afford it. Similarly, many other purchases that lead to debt allow consumers to select lower cost options (e.g., starter homes, used cars with high mileage, community college), but lower cost medical care is not always an option. Further, patients are usually unable to compare prices and/or determine their out-of-pocket cost ahead of time, so even if the care could be delayed, it would be challenging to make financial decisions about medical care because it is difficult to know how much it will ultimately cost.

As a result, many patients have to choose between delaying necessary care or going into debt to receive it. Delaying care until the patient can pay their full out-of-pocket cost without debt would be detrimental to their physical and mental well-being, which would not serve the state’s interests and has turned the policy focus on ways to prevent, eliminate, and reduce the negative consequences of medical debt.

One approach to this problem would be to prevent medical debt through overall health care reform which limits individual health care costs, but this would be a massive undertaking requiring significant tradeoffs and implications across the economy. Short of that, the conversation has turned in two directions: debt forgiveness and restrictions around debt collection and utilization practices, both of which have been implemented to varying degrees.

Given the number of people affected by medical debt in the United States and the overall impact of health care costs, efforts to reduce or limit medical debt are present at every level of government. For instance, the Biden Administration recently proposed a rule, under the authority of the Consumer Financial Protection Bureau, that would require medical debts to be removed from credit reports. This proposed rule follows action from the Administration in 2022 to combat medical debt, which include public information efforts, directives to agencies aimed at making it easier for people with medical debt to access government programs, and investigations into medical debt practices. Over the last three years, private credit rating agencies have agreed to limit the inclusion of certain medical debt on credit reports, which has decreased the number of people whose credit reports contained medical debt collections significantly over the last couple of years, but this agreement is non-binding and could change at any time without further regulation.

Additionally, non-profit organizations and state and local governments have ramped up efforts to provide medical debt relief around the country. Specifically, Michigan included $4.5 million in the FY2024 budget for a grant program administered by a non-profit to “to eliminate medical debt to patients with an income below the federal poverty level with a financial need or who face insolvency.” This grant was designed to go to Undue Medical Debt (formerly known as RIP Medical Debt), which has already partnered with a number of counties in Michigan. Wayne, Oakland, Muskegon, and Kalamazoo counties have established programs utilizing COVID relief money to partner with Undue Medical Debt to pay off medical debts for their residents. These partnerships combine county funds with Undue Medical Debt’s charitable resources to purchase debt from creditors for significantly less than it is worth and forgive it. Data on the amount of debt forgiven to date is not available as some of these agreements are relatively new, but the programs in just those four counties have the potential to eliminate nearly $900 million in debt, according to the counties’ estimates.

Limitations of Existing Efforts

While the existing efforts to address medical debt are worthwhile, there are a few reasons to consider additional actions, particularly at the state level. First, while public-private partnerships to forgive debt are beneficial to the borrowers and relatively low cost for those buying and forgiving the debt, the initial evidence suggests this type of debt relief did not improve average beneficiaries’ finances, access to credit, or their physical or mental health. The study’s author, who partnered with Undue Medical Debt to study the program, thinks that the forgiveness evaluated in the studies was occurring too late for recipients to have been spared the negative consequences of having medical debt. Other research has shown the value of hospital financial assistance programs that target costs earlier in the process. As a result, Undue Medical Debt is attempting to redesign certain aspects of their program. At any rate, it may be the case that while ultimately having the debt forgiven is useful, the experience of being in medical debt is a negative experience that has lasting consequences.

In addition to the potential limitations of medical debt forgiveness as currently implemented, medical debt relief occurs at a moment in time, forgiving a debt from the past but not changing anything about future debt accumulation. This is similar to student loan forgiveness, which helps existing borrowers and has potential economic value, but does not prevent future borrowers from getting into similar situations. Further, these medical debt relief efforts have generally been funded with one-time appropriations. Certainly, there is ongoing funding on the non-profit side, but state and local governments have made individual decisions to fund programs as money has been available. In leaner times, governments may not have the resources to fund these programs, and/or new officials may oppose the effort entirely, leaving the existence of debt relief open to unpredictability.

That being said, there are ways to reduce the impact of medical debt on individuals short of policies that eliminate it in the first place or ultimately forgive it. Specifically, regulating debt collection practices and the ways in which medical debt can affect one’s life are potential policy directions. As noted earlier, the federal government has taken and proposed action in recent years to monitor and regulate practices around medical debt. However, these policies have been either general executive policies, which can be easily modified by future administrations, or administrative rules, which are much more likely to be challenged and blocked following a series of recent U.S. Supreme Court cases that provided federal courts more latitude in reviewing federal regulations. While these policies have merit, it may not be safe to rely on their survival as currently established.

In terms of federal law, protections are relatively limited and are loosely enforced. A U.S. Senate committee recently held a hearing on this issue and several bills introduced in Congress would expand both medical debt forgiveness and laws around medical debt collections and impact, but it does not appear that this legislation is on track to become law in the near future. Consistent with this reality, part of the Biden Administration’s press release about its proposed rule for credit reporting was devoted to highlighting the areas in which states can take action.

State Policy Options on Medical Debt

Given the limitations and unpredictability of federal policies to protect people with medical debt and the limitations of debt forgiveness programs, the role of state regulations around medical debt practices are an important safeguard. Many states have implemented a variety of policies pertaining to medical debt, but Michigan has not enacted any of these policies.

Financial Assistance Policies: Twenty states, including Ohio and Illinois, have laws requiring hospitals to have financial assistance policies, which are policies that establish when and to whom hospitals must provide free or discounted care. States vary in the tools they use to ensure compliance, such as licensure requirements and access to state funding. While the laws vary in terms of how much assistance is provided and to whom, a major part of the value is ensuring that people are connected to resources to reduce costs prior to receiving bills and ultimately going into collections.

Billing and Collections Practices: Federal protections related to billing and collection practices are limited to notifications and waiting periods, but states have taken a variety of measures to regulate those practices. Eight states, including Illinois, require hospitals to offer payment plans. Six of those states set limits on the amount that can be charged monthly and/or the interest rate. Eight states have a general cap on interest for medical debt, with five of those states identifying certain populations who cannot be charged interest on medical debt at all. Fourteen states establish one or more preconditions before a hospital can send a bill to a collections agency, such as notification, screening for financial assistance eligibility, and affirmatively offering a payment plan. Three states prohibit the sale of medical debt, and two others place restrictions on those buying medical debt. Ten states have laws restricting the reporting to or use of medical debt by credit agencies, including outright bans, waiting periods, and restrictions on what amounts can be reported.

Medical Debt Lawsuit Protections: Federal law also offers notification and waiting periods prior to initiating lawsuits for medical debt collection, but states have gone further. Three states have limitations of some form on initiating lawsuits, including an Illinois law that does not allow lawsuits against uninsured people who demonstrate an inability to pay. Eleven states, including Illinois and Ohio, have laws limiting or prohibiting the placement of liens or foreclosures due to medical debt. Twenty-one states have laws which exceed the general federal standard for maximum wage garnishment, while 15 states prohibit wage garnishment for medical debt entirely, for specific populations, or in certain circumstances.

Reporting Requirements: Federal law places certain reporting requirements on non-profit hospitals, including spending on financial assistance, for-profit hospitals are not included. Thirty-two states have some type of additional reporting requirement that includes one or more of financial assistance spending, details about financial assistance program applications and approvals, and medical debt lawsuits.

Making Medical Debt Less Burdensome in Michigan

Given that Michigan has not regulated medical debt at all, policymakers have a wide variety of options to consider when addressing this problem. In terms of financial assistance policies, the state does not necessarily need to require expansive financial assistance policies, but it should require that any hospital that has a financial assistance policy provide information about the program to patients and screen them for eligibility. If support is available to patients, the state should ensure that they are made aware of it and informed whether they qualify before they end up in debt. The research on medical debt forgiveness indicates being in medical debt at all, even if it is ultimately forgiven, has negative consequences. This is a strong argument for making sure people get access to assistance, if they qualify, before they end up in debt unnecessarily. If possible, the goal should be preventing debt from accumulating in the first place, and a law of this nature would make some headway.

Policies in the arena of billing and collection practices, as well medical debt lawsuit protections, could create more stringent protections. While the state plays a role in regulating debt in general, the law should recognize medical debt as a special class of debt that entitles borrowers to greater protections. Medical bills are less discretionary than other kinds of debt, like mortgages, car loans, and student loans, as medical care is often necessary and time sensitive, and patients are unable to compare prices and/or determine their out-of-pocket cost ahead of time. People do not get into medical debt because of unwise financial choices or poor planning, they simply cannot afford important medical care.

The state should institute key protections that prevent medical debt from burdening people who have limited or no ability to pay, while also ensuring tools exist for providers to collect from people who have an ability to pay but are attempting to avoid payment for some reason. One key reform would be requiring providers to offer payment plans with caps on monthly amounts and interest tied to ability to pay. Additionally, collection agencies are much more aggressive than providers themselves in their collection tactics and the state should consider placing limitations on when bills can be sent to collections. Specifically, processes should be in place to ensure that bills only go to collections after the bill has been reviewed to ensure the patient received the full insurance coverage they were entitled to; the provider has made a determination about the patient’s eligibility for an in-house financial assistance; and the provider has made a determination about whether the patient actually has the ability to pay.

Hospitals should not be prohibited from employing outside agencies to collect from people who are truly avoiding their responsibility to pay, but sending collections agencies after patients without more procedural protections is not in the state’s interest. A similar set of protections against lawsuits, where the provider has to make sure the issue is simply an unwillingness to pay before initiating legal action, also makes sense. Caps on wage garnishments also fit into this category – they should not necessarily be prohibited, but they should only be ordered as a way to compel collection from bad actors rather than people who are unable to pay. Finally, a state law that prohibits medical debt from being reported to credit agencies would be a good backstop against changes in federal policy.

Conclusion

Medical debt affects over 40 percent of the population and affects communities that face health disparities to an even larger degree. Efforts to eliminate medical debt have centered around debt forgiveness, which is a useful but limited tool as currently implemented.

Many states, but not Michigan, have implemented protections surrounding medical debt based on the acknowledgement that medical debt is a distinct type of debt where borrowers should have greater protections. These policies include financial assistance requirements, billing and collection regulations, limitations on lawsuits, and reporting requirements. Michigan can chart an effective course by enacting laws that protect people who are unable to pay while also leaving tools in place for providers to recoup costs from individuals who are attempting to avoid payment.