July 28, 2026

In a Nutshell

- Preliminary health insurance rate filings with the State of Michigan signal that health insurance premiums could see a double-digit increase in 2025.

- Public schools operate under a 2011 state law that caps how much a school district pays for employee health insurance. This “hard cap” will increase by just two-tenths of a percentage point in 2025; this leaves school employees with higher out-of-pocket insurance expenses because employer contributions are capped.

- Additional out-of-pocket costs are likely to eat into the recent salary gains of the average Michigan public school teacher.

Inflation may be cooling, but health insurance premiums are on the rise.

On average, health insurers participating in Michigan’s small group market next year are seeking an 11.2 percent increase in insurance policy premiums. Similarly, insurers in the individual market, including policies sold through the Affordable Care Act’s health insurance exchange, are requesting a 10.5 percent bump in premiums for 2025. If approved by the state, these would be the largest increases in health insurance premiums since 2018.

While K-12 public schools don’t participate in either of these insurance markets, Michigan school districts are likely to see similar rate hikes this fall when insurers share their 2025 plans and pricing with the state’s nearly-900 traditional public, charter public, and intermediate school districts. And, just as private sector employers facing skyrocketing insurance rates will have to determine how to manage these spending pressures and share the increased health insurance cost burdens with their employees, public school districts will have to do the same.

But, unlike the private sector, public schools must comply with a 2011 state law that caps how much a school district pays for employee health insurance. For 2025, this employer cap is scheduled to increase only two-tenths of one percent (0.2 percent), meaning that school employees will shoulder nearly all of the projected increase in health insurance premiums next year. Absent a change in state policy to shift more of the increased health insurance costs to employers, school employees will be paying more out-of-pocket for their current plans. And, these additional out-of-pocket costs are likely to eat into the recent salary gains of the average Michigan public school teacher.

State Budget Challenges lead to Mandated Health Insurance Cost-Sharing for Public Employers

First, a bit of background.

During the lean state budget years following the Great Recession and, in part, to accommodate then-Governor Rick Snyder’s 2011 state tax restructuring plan, state policymakers agreed to an across-the-board $470 per-pupil foundation allowance reduction to balance the Fiscal Year (FY)2012 School Aid Budget. Acknowledging this historic education funding cut and in an attempt to ameliorate its impacts on school budgets, lawmakers enacted several reforms aimed at easing several concurrent spending pressures facing public schools. This included various reforms to the teacher retirement system, as well as mandating minimum levels of employee cost sharing for health insurance.

Specifically, Public Act (PA) 152 of 2011 created the Publicly Funded Health Insurance Contribution Act to limit the amount that public employers (state and local governments) can pay toward employee medical benefit plans. Effective January 1, 2012, PA 152 established annual employer contribution limits or “hard caps”, based on the type of coverage selected by its public employees. For 2012, public employers could pay no more than $5,000 for single person coverage, $11,000 for individual plus spouse coverage, and $15,000 for family coverage. Any annual medical plan costs above the employer’s hard cap limit is the responsibility of the employee. (Note: As an alternative to the hard cap requirement, PA 152 allows a public employer, upon a vote of its governing body, to comply with a requirement that it pay no more than 80 percent of the total annual costs of all the medical benefit plans it offers, leaving employees to pick up the remaining 20 percent. The State of Michigan has chosen to comply with this requirement.)

The hard cap amounts are adjusted annually based on changes in the medical care component of the United States consumer price index (CPI). The State Treasurer calculates the annual cap adjustment and maximum employer contribution by April 1 for the next calendar year. This provides insurers and employers time to negotiate plan design and pricing for employee health insurance offerings presented during “open enrollment” periods in the fall and that take effect January 1.

Notably, PA 152 allows a local government (county, city, village, township, etc.), with a two-thirds vote of its governing body, to exempt itself from the minimum cost-sharing mandates, both the hard cap limit and the 80/20 cost-share requirement. A separate vote is required each year a unit of government chooses to exempt itself. While several local governments have voted to exempt themselves, the law does not provide public schools with the exemption option. Thus, public school employers/employees have been subject to either the hard cap or 80/20 cost-share requirement since 2012. (Note: A recent survey of traditional K-12 school districts revealed that more than four of five districts currently use the hard cap to comply with PA 152 requirements.)

Premium Increases will Require More Out-of-Pocket from School Employees

Changes in medical care prices typically outpace growth of prices in the broader economy. However, starting in 2021, prices for many non-medical goods and services began increasing rapidly, outpacing the growth in medical prices. This recent divergence, in tandem with the year-lagged data used to compute the medical component of the CPI, is reflected in the very small increase in the PA 152 hard cap limit calculated for 2025.

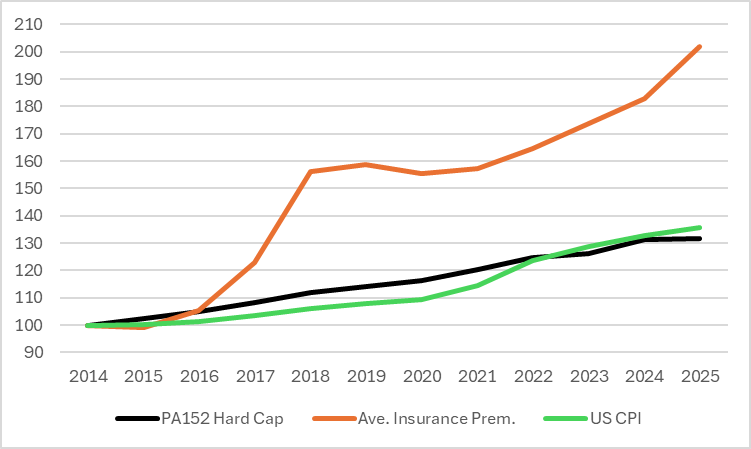

For the 12-month period ending February 2024, medical prices increased just 0.2 percent compared to the previous 12 months. This is the smallest annual increase to the PA 152 hard cap limit to date and follows a 4.1 percent increase for 2024 medical plans. The chart below tracks the growth in the average price of unsubsidized health insurance premiums in Michigan’s individual/family market since 2014 compared to changes in the general price index (US CPI) and PA 152 hard cap limit since the state mandated health insurance cost sharing for public school employees.

Growth in Ave. Michigan Health Insurance Premium, General Prices, and PA152 Hard Cap Since 2014

Source: ACAsignups.net; healthinsurance.org; Michigan Department of Treasury; Consensus Revenue Estimate Conference reports

Over the 11-year period, the average premium price for Michigan health insurance has doubled. This price escalation dwarfs the growth in general prices as measured by CPI (36 percent) and the 32 percent rise in the PA 152 hard cap. Also worth noting, between 2019 and 2025, general prices are estimated to increase by 18.7 percent while the PA 152 hard cap will increase about one-half that amount (9.7 percent). Since 2016, the growth in average insurance premiums has been nearly triple that of the PA 152 hard cap.

The bottom line is that there has been a growing disconnect between the average health insurance premium price in Michigan and PA 152’s inflation adjustment factor. This is explained, in part, by the fact that the adjustment factor (medical CPI) is pegged to prices of a much broader basket of medical goods and services beyond health insurance premiums. Further, the health insurance component represents just seven percent of the overall medical CPI index and there is research to suggest it is a poor measure of actual premium pricing in the health insurance market.

Returning to the law’s prospective impacts for 2025. The miniscule rise in the medical prices during the most recent 12-month period means that school districts, in order to comply with the PA 152 hard cap, can only increase their portion of annual health insurance premiums by two-tenths of one percent next year. Based on current-year employer contribution limits, this equates to a $15 change for a single coverage plan ($7,203 to $7,718) and a $42 change for a family coverage plan ($21,008 to $21,050).

Any 2025 insurance premium increase above these paltry amounts would fall to school employees to pick up. For perspective, last year’s 4.1 percent increase in the employer hard cap limit (for plans effective beginning January 1, 2024) allowed school districts to contribute an additional $364 for a single coverage plan and $828 for a family coverage plan in 2024.

To illustrate the impact on employees, assume health insurance premiums within the public K-12 education market rise eight percent next year, generally following the trend observed in other markets. An average family coverage plan that is priced at $24,000 this year will increase to $25,920 for 2025. Because the PA 152 hard cap only allows employers to pick up $42 of the illustrated $1,920 premium increase, all else being equal, employees will experience increased out-of-pocket costs of $1,878. This increase would be in addition to the $2,992 insurance cost they are currently paying ($24,000 less $21,008 hard cap limit) for their family coverage. This represents a year-over-year increase in their health insurance cost-share of 63 percent (from $2,992 to $4,870).

Higher Out-of-Pocket Costs and Inflation Erode Salary Gains

These additional out-of-pocket costs will further erode the moderate wage increases many school employees have received since the pandemic. Increases that followed a period of generally stagnant average teacher salaries in the Mitten State.

The average public school teacher salary between 2010 and 2018 hovered between $62,000 and $63,000. Our previous research showed how, despite moderate growth in per-pupil spending during this period, rising financing obligations for legacy debts tied to the school employees’ retirement system contributed to little change in employee salaries. These retirement spending pressures effectively crowded out school funding available for teacher salaries for several years. Factoring in the general rise in prices during the pre-pandemic period, the average teacher salary lost roughly 10 percent of its purchasing power due to inflation.

While we don’t yet have 2024 salary data, over the previous four-year period (2019 to 2023) the average teacher salary is up 7.8 percent from $62,170 to $67,012, with much of this growth occurring between 2022 and 2023. From an employee perspective, this moderate bump in the statewide average is welcomed news given the previous trend of stagnate salary growth, but it also came during a period of high prices.

It is worth noting why salaries are up. First, the school budgets have benefited from very strong state revenue growth in recent years and the massive amount of federal pandemic relief pouring into public schools. In addition to healthy annual bumps to the general per-pupil foundation allowance (21 percent between FY2020 and FY2024), policymakers have appropriated over $1 billion for new categorical programs to address K-12 education labor shortages, including through employee compensation measures. This includes several new state-funded programs that directly finance increased teacher pay within certain local districts. Generally, flush public K-12 school budgets in recent years have allowed district leaders to budget resources to address stagnant average teacher salaries, reversing a long-standing trend that placed Michigan‘s teacher salary growth near-last in the nation.

These gains, however, have come at a time of high inflation; while the average salary grew 7.8 percent from 2019 to 2023, inflation over the period rose 21 percent. And, looking forward, the financial effects of the PA 152 cost-share requirements in 2025 will further erode the purchasing power of teachers’ increased take-home pay.

Amending select provisions of the PA 152 cost-share requirements could provide school employees relief from future additional out-of-pocket costs. A few possible policy changes to reduce employee costs include: re-setting the statutory base employer amounts to better reflect current premium prices in the K-12 education health insurance market; raising the employer/employee cost-share distribution from 80/20 to 90/10; and changing how the employer hard cap limit is annually adjusted to allow employer contributions to grow at a different rate.

As with all policy changes dealing with public budget constraints, each of these examples will involve trade offs. Most directly, any reduction to the amount of out-of-pocket insurance contributions paid by employees will result in employers assuming additional funding responsibilities. And, these new financial obligations do not come with additional state or local revenues. Faced with finite budget resources, districts that have to spend more for employee health insurance will have fewer resources to pay for other employee compensation items.

Enacting any legislative changes in time to materially impact the 2024-25 school budgets may be a challenge. Most school districts may be well into their employee benefit “open enrollment” period by the time Michigan lawmakers return from their summer break and are able to agree to a policy solution and get it signed into law by the governor. The reality is that 2025 medical plans being prepared for school open enrollment windows will have to reflect health insurance plan designs and the employer/employee contributions under the current PA 152 requirements. Even with a statutory change this fall, gaining the political votes required to give the legislation immediate effect may be elusive. If the policy does not take effect until March 2025, it can’t provide immediate relief to school employees.