August 11, 2026

In a Nutshell

- Michigan has improved its cash position since the Great Recession; it is the strongest it has been in decades

- State’s strong cash position will help officials manage through budget challenges over the next couple years

- To avoid creating long-term fiscal problems, policymakers must guard against relying on budget tactics common in the 2000s

The oft-quoted expression “cash is king” is ubiquitous in the private sector and generally refers to the importance placed on cash flow in assessing the overall fiscal health of a business. But, it is equally important in assessing the health of governments, especially during financial crises. As the national and state economies dip into recession caused by COVID-19, the Research Council has found that the State of Michigan has made major strides to improve its cash holdings and strengthen its cash flow in the years since the Great Recession. The state’s cash position is as strong as it had been in two decades. In the face of reduced state revenue and additional spending pressures arising from the pandemic, maintaining this healthy status is not a given and will depend on policymakers’ fiscal decisions going forward as they prepare state spending plans for the upcoming fiscal year.

The Importance of Cash for Government

Key indicators of a governmental unit’s overall fiscal health, year- and month-end cash balances along with the timing of revenue receipts and expenditures (cash flow), often go unnoticed until a government is unable to pay its bills in a timely fashion. While much attention is given to a government’s ability to maintain a balanced budget, equally important is making sure it has sufficient cash available to meet its obligations when they come due. The credit worthiness of a government is invariably tied to its ability to manage its cash flow effectively and efficiently.

State and local governments’ fiscal health are the most at-risk during economic disruptions. The current recession is no exception – governments face a host of fiscal pressures on both sides of the ledger. As it relates to cash flow, the arithmetic is fairly simple – government revenues fall with a slowdown in economic activity while the demand for and spending on essential services remain fairly constant, or even become elevated. This requires public officials to take action in fairly short order, delaying corrective action(s) only compounds the financial problem (i.e., shorten the amount of time to make changes).

In the immediate-term, governments must take action to make sure they have sufficient cash on hand to meet approved obligations as those bills come due. This primarily means making adjustments to the spending-side of the budget, including reducing spending for personnel, maintenance and capital improvements, and outside contractors. Other options public officials might consider involve delaying vendor payments to the maximum allowable length to help achieve a more favorable balance between cash inflows and outflows.

Governments’ short-term options to raise additional resources are limited. The main strategies involve repurposing general fund reserves intended for special projects that are not of vital importance and dipping into reserves or rainy day funds. Both are one-time strategies that are not sustainable. While increasing general taxes, or even specific fees, are more sustainable strategies, they are less feasible during a recession because the loss of jobs and wages in a contracting economy reduce citizens’ ability to pay higher taxes. Additionally, the time lag between the policy decision to increase a tax rate and the resulting revenues is much greater than when a business decides to increase the price of a good or service.

Building Reserves and Cash Improvements

To weather the current fiscal storm and ensure Michigan state government has the resources to meet its financial obligations when they come due, the state will have to properly manage its cash flow over the coming months and, possibly, years. Fortunately, Michigan’s cash position has improved dramatically over the past 10 years. Going into and throughout the years of the Great Recession, cash was very tight. This limited some of the fiscal responses that state policymakers had at their disposal to deal with effects of the recession.

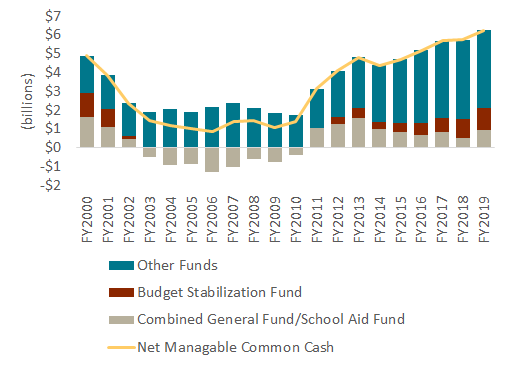

The state accumulated more than $5 billion in Common Cash reserves by the end of FY2016 and now stands at $6.3 billion (see chart). This is a marked improvement since FY2006, when cash holdings were below $1 billion. Since FY2012, the state has been able to maintain year-end cash reserves of at least $4 billion, averaging approximately 23 percent of combined General Fund and School Aid Fund revenue. Revitalization of the Rainy Day Fund contributed to these improvements. The Rainy Day Fund, the state’s savings account, is statutorily protected from use outside of economic downturns. It held over $1 billion in reserves at the end of FY2019, up from close to zero just eight years ago.

Common Cash Balances

Source: Michigan Department of Treasury

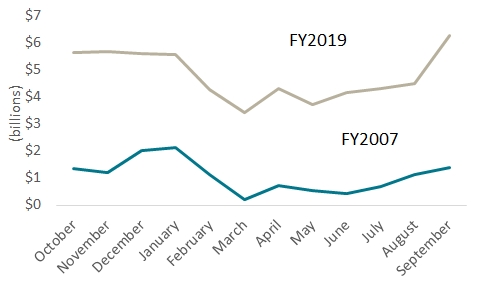

The improvements in the year-end numbers are mirrored in the state’s net monthly cash-on-hand balance (see chart). Twelve years ago, the state’s cash position had deteriorated to the point where it was close to running out of manageable cash to meet its obligations. This fiscal emergency prompted Lansing policymakers to take the extraordinary step to change monthly state aid payments to K-12 school districts. Comparing the FY2007 numbers to FY2019, shows the strides made. Month-end cash balance never dropped below $3 billion in FY2019.

Month-End Common Cash Balances – FY2007 and FY2019

Source: Michigan Department of Treasury

Avoiding Past Mistakes

A major contributing factor to the FY2007 cash crisis was poor management of the state’s budget woes. Over the first decade of the millennium, Michigan struggled with structural deficits and falling state revenue. Through the use of many one-time budget fixes and other unsustainable fiscal practices to achieve balance in the state budget, lawmakers were able to postpone solving a $2 billion annual structural budget deficit in the combined General Fund and School Aid Fund. As a result, the health of the state’s cash position took a backseat and threats were ultimately ignored until the cash position was at risk of going negative.

The current fiscal picture has the potential to create a similar budget focus for policymakers. It would be a myopic approach to maintain budget balance through a series of one-time or non-recurring fiscal interventions. With projected budget deficits nearing one billion dollars for the next two years, a lot of attention will be paid to how the state balances the budget. Finding the right mix between spending cuts/delays, revenue increases, asset sales, use of Rainy Day Fund dollars, and federal assistance will be necessary to maintain structural balance over the long-term without badly damaging the state’s cash position. If not, policymakers run the risk of falling into the same trap the state found itself in throughout much of the 2000s.