July 6, 2026

In a nutshell:

- Local governments are dependent on property tax revenues, but Michigan taxpayers have adopted multiple tax limitations over the years due to a growing property tax burden. These limitations have led to revenues that are more stable and predictable for local governments, but they have also restrained growth.

- The problem with over-reliance on the property tax is that it captures only a narrow segment of economic activity and is insufficient alone to fund all local government services. An ideal tax structure produces revenue sufficient to provide services, with components that respond to economic growth, like sales and income taxes, and components that are stable through economic fluctuations, like the property tax.

- More than simply changes to property tax limitations, Michigan local governments need a more diversified tax structure that allows local governments to access revenues connected to their economy combined with efforts to provide services more efficiently at a regional level.

Taxpayers across the country have adopted property tax limitations in their states that take one of three different forms:

- A rate limit creates an upper bound on the tax rate that a governmental unit can levy.

- An assessment limit restricts how much a taxpayer’s property value can increase year-to-year.

- A levy limit restricts how much a jurisdiction’s tax revenue can grow, generally expressed in year-over-year terms.

Michigan taxpayers have adopted all three types of limitations. Rate limits are written into the Constitution and state law. The Headlee Amendment of 1978 included a levy limit and Proposal A of 1994 included an assessment limit. See my last blog for details on these different limits and how they impact the Michigan property taxpayer.

Property Taxes in Michigan

Michigan local governments are heavily dependent on the property tax to fund services, and this can lead to the tax being particularly burdensome to taxpayers. Michigan is one of 11 states where residents paid more than 1.5 percent of their home value in property taxes; most states averaged between 0.5 and 1.5 percent.

Property taxes are so important in Michigan because they are the main local-source revenue option for all types of local governments. Twenty-four cities levy income taxes to supplement their property taxes and counties levy some small taxes (e.g., real estate transfer and tourism-related), but for the rest of Michigan’s local governments, property taxes are their sole source of tax revenue. This heavy dependence on property tax revenue creates friction as local government officials view with disfavor any attempt to limit that revenue, at the same time taxpayers view the property tax as unduly burdensome.

Criteria for Evaluating Effective Tax Policy

Effective tax policy is evaluated differently for taxpayers than for local governments. As we learned a few weeks ago, effective tax policy for taxpayers provides limits on the growth in tax burdens, predictability in year-to-year tax bills, an easily understandable process, and equity across similarly situated taxpayers. Michigan’s tax limitations have been successful at limiting tax burdens and providing predictability, but they have created a process that can be difficult to understand and that lessens equity among taxpayers.

Effective tax policy for local government provides:

- Revenues that can grow with the local economy

- Revenues that are stable and predictable

- The ability to minimize the downside risk associated with declining property values

It is no easy feat to find a scenario where tax limitations work to constrain growth in the tax burden for taxpayers while also providing stable revenues that reflect the local economy. The tax limitations help local governments to know what their revenues will be with more certainty than having tax revenues that respond directly to market growth or decline every year.

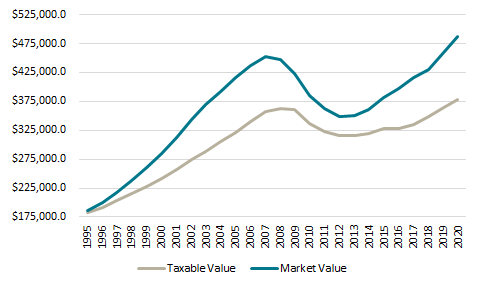

Chart: Statewide Market Value and Taxable Value, 1995 to 2020 (Dollars in Millions)

Proposal A’s assessment limit helps to minimize the downside risk because it provides local governments with a reservoir of potential revenue that can continue to grow even if property values start declining like they did during the Great Recession (see Chart). This helps to explain why the Great Recession did not have as much of an impact outside of Southeast Michigan; communities had enough of a gap between their taxable value and market value that revenues could keep growing and protect local governments from the large drops experienced in market value. The depth by which the recession depressed property values in Southeast Michigan was so great as to erase the gap and push down taxable value as well.

If tax revenues are not growing (or are even declining as they did during the Great Recession), local government budgets cannot be immediately decreased to reflect lower revenue levels. During times of fiscal hardship, less property tax burden is good for taxpayers, but it can be difficult for local government budgets to adjust quickly to declining revenues.

Property Tax Alone Insufficient

The property tax is and always has been the primary tax revenue source for local governments in Michigan. The limitations that have been adopted have restrained property tax revenue growth, but they have also increased predictability and stability for local government budgets and have limited the rate of yearly growth for taxpayers.

Whether or not the property tax with limitations provides adequate revenue is subjective. What is clear is that local revenues are not connected to the local economy in the same way that state revenues are connected to the state economy. The local property tax captures only a narrow segment of economic activity. Many communities are expanding and/or experiencing economic growth as we emerge from the COVID-induced recession, but the economic recovery evident with bustling downtowns and job growth does not translate into growing revenue streams for local governments.

A tax structure with options to add sales and income taxes would better achieve a more ideal tax structure. Each can raise significant revenues on its own. Diversity would allow for growth and stability. Sales (and use) taxes capture the economic activity that defines many regions. Northern counties would benefit from tourism activity and urban counties from the retail trade. Income taxes capture the economic strength of each county. It rewards successful business attraction and community development.

Diversify Local Revenue Sources and Regionalize Service Provision

An ideal tax structure produces revenue sufficient to provide services, with components that respond to economic growth and components that are stable through the economic fluctuations. It does not create administrative burdens and does not disrupt economic choices. Property taxes provide a stable revenue source, especially in Michigan with the modified acquisition value system, but they are burdensome because they are the primary revenue source for all types of local governments and they are restrained from responding to economic growth by Michigan’s tax limitations.

Many other states afford their local units of government several tax options – general and selective sales, income, transportation, various tourism, and others – to capture economic activity and to create diverse revenue streams. Michigan allows cities to levy a local income tax and allows Detroit and some counties to levy certain other local taxes, but otherwise restricts local governments from levying diverse taxes. Providing local governments with more access to local-option taxes can be part of the solution to the problems inherent in the local government finance structure.

One problem with increasing tax options at the local level is that it can increase economic competition between local governments. Few local governments would want to be the first to levy a sales or income tax lest it cause an outmigration of business and/or cause changes in purchasing habits. One option to avoid this is for state policymakers to consider reforming the state’s revenue sharing program as a remedy to the woes of the property tax system.

Revenue sharing was originally adopted in place of allowing for local-option revenues. It served to provide local governments with revenues from diverse sources while centralizing the revenue raising function at the state level. This system works well when it is fully funded. The problems arise when the state faces budget shortfalls, as it has repeatedly since 2000, and cuts funding to local governments to meet its own funding needs.

A diversified tax structure with or without state revenue sharing is not a panacea but could be combined with other reforms, like regionalizing service provision, to improve the local finance system. Building off the idea of regionalizing services, any new local revenues should be authorized at a regional level to promote regional governance and tax base sharing.

Conclusion

None of these options alone – providing access to more local-option taxes, providing more services at the regional level, reforming statutory revenue sharing – will fix Michigan’s broken municipal finance system. Taken together, they may provide a foundation for a more stable finance system that provides services efficiently and effectively and allows local governments to access revenues connected to their economy. These options can also be combined with changes to limitations in the current property tax system.