April 7, 2026

In a Nutshell:

- Special education services are funded by intermediate school districts primarily with dedicated local property tax revenues, the amounts of which vary considerably.

- The State of Michigan provides financial aid to low-wealth districts to help equalize their tax base and augment the revenue generated by these dedicated taxes.

- A new legislative proposal to provide districts with supplemental payments would work at cross purposes of existing state efforts to equalize funding for students with disabilities across the state.

Over the past decade, report after report after report has identified a number of major challenges inherent in Michigan’s system for funding special education services to nearly 200,000 students with disabilities (13 percent of the statewide public school student body). One key observation from each of these reports is the fact that the system generates massive per-pupil funding/revenue disparities depending on the intermediate school district in which a student resides.

Now comes a funding proposal championed by the House of Representatives that would exacerbate existing per-pupil funding disparities. The proposed $20 million appropriation would provide up to three times more state funding to higher-taxing districts ($150 per pupil) than lower-taxing districts ($50 per pupil). For example, an intermediate district that is able to generate $500 in local tax dollars per student would be eligible for up to $150 per student in state aid payments, but a district raising only $350 from its local tax would receive $50 per student from the state. Districts taxing at their statutory cap, but raise no more $500 per student from the dedicated special education millage, would be eligible for a $150 per-pupil payment from the state.

Surprise, surprise! A property tax-driven funding model produces inequities

First, let’s get this fact out of the way – special education finances are very complex. Complexity surrounds everything from where the money comes from and how it is distributed across K-12 districts to what these public dollars can/cannot be used for and how spending is tracked. Needless to say, policy discussions on the subject can get “down in the weeds” very quickly. Here, we highlight how the system’s reliance on local property wealth drives systemic per-student funding differences and why this is an important state policy issue.

It’s important because the State of Michigan has plenary power over public education generally and because both state and federal law guarantee that students with disabilities will receive a free and appropriate public education. Despite these powers and mandates, reliance on locally-levied property taxes means that a student with a disability attending school in one corner of the state may not get the same funding as a student with a similar disability in another corner of the state. As a result, service levels vary from district to district and result in systemic inequities.

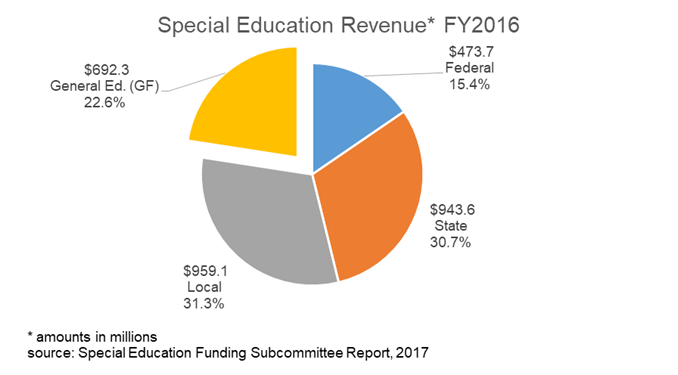

Similar to funding for general K-12 education, special education services are financed by a variety of revenue sources, including federal, state, and local dollars. But, unlike the general K-12 education funding model where state-level resources dominate, special education remains a predominantly locally-financed service. Specifically, locally-approved, dedicated property taxes play the largest role, accounting for nearly one-third of the total public contribution statewide.

Because of the large role played by property taxes and the significant differences in property wealth (tax bases) across the state, the amount of special education property tax revenue generated by intermediate school districts (ISDs) varies substantially. In 2018, the yield from a one-mill special education tax levy across each of the 56 ISD taxing jurisdictions varied from $600 per student (highest) to $142 per student (lowest). These property wealth variances are amplified by the fact that districts tax themselves at different rates (which are capped by state law). Factoring in the different ISD tax rates charged, 2018 special education millages yielded from $1,725 per student (highest) to $600 per student (lowest).

The state has recognized the effects that property wealth/rate disparities can have on the ISD tax levies and how these differences directly contribute to per-pupil inequities across the state. To address this issue, the state created a dedicated pot of money ($40 million in FY2021) to provide “millage equalization” payments to augment the local tax revenue generated from its current tax base and authorized rate.

The amount of state aid effectively limits the degree of tax base equalization and, therefore, the number of districts that receive payment. For FY2021, payments under Section 56 of the State School Aid Act only equalized ISD tax bases up to $209,000 taxable value per student, well below the statewide average of $252,000 per student. With this limited funding, only 13 ISDs qualify for state aid and 60 percent of the funds go to one district.

Legislative proposal would stifle current equalization efforts

It is well understood that the amount of annual funding provided for Section 56 payments limits the extent to which the State of Michigan is able to equalize ISD tax bases. In addition to the constraints associated with limited state dollars, equalization advocates will have another headwind to contend with if a new appropriation proposal supported by the House of Representatives becomes law. This new program would work at cross purposes of the existing Section 56 payments. Instead of providing more state dollars to those districts with low property wealth, the new program (Sec. 56(6) of the FY2022 School Aid Budget) is structured to send more state dollars to those districts that raise more money from their local dedicated special education tax. The program threatens to exacerbate existing and growing per-pupil funding inequities across the state.

This is how the proposed $20 million appropriation would operate. The state would provide supplemental payments to ISDs based on the amount of revenue raised through their local special education millage. For districts raising between $350 and $400 per student from the tax, the state would guarantee each receives at least $400 per student. That means, for a district that raises exactly $350 per student, the state would provide an additional $50 for every student enrolled in the constituent K-12 school districts within the ISD. For an ISD generating $399 per student in tax proceeds, the state payment would be additional $1 per student.

At the other end of the spectrum, for districts raising between $500 and $650 per student from their local tax, the state would guarantee each receives at least $650 per student in combined local tax and state aid. Generally, these are wealthier districts or districts taxing at relatively higher rates, or both. For this “tier” of districts, the maximum state payment would be $150 per pupil (i.e., for a district generating $500 per student). This is three times the maximum payment ($50 per student) a low-wealth district could receive (i.e., for a district generating $350 per student).

Within the various “tiers” of districts (e.g., $350/$400 per student, $400/$500 per student, and $500/$650 per student), funding equalization appears to be the policy goal and the payment mechanics are aligned accordingly. However, when the maximum payment amounts across “tiers” are analyzed, it is clear that equalization is not the policy goal. In fact, the payment structure operates in way to stifle the existing Section 56 millage equalization payments.

Michigan policymakers should be applauded for bringing attention to the long-standing special education funding inequities across the state. However, the House of Representative’s proposed policy prescription fails to address a major funding equity problem with the state’s special education financing system. As we have illuminated here, it actually works at cross purposes with existing, long-term efforts to “equalize” local special education millages and reduce per-pupil funding gaps. It is unclear what policy objective the House is seeking to achieve with its proposed $20 million appropriation.