July 28, 2026

A version of this blog appeared in the editorial section of the Detroit News on June 23, 2021.

In a Nutshell

- Michigan has an additional $3.5 billion in state revenue and $6.5 billion in federal stimulus to work with as policymakers finalize the FY2022 state budget

- While the stimulus dollars come with strings attached, provisions that allow funding to be used to offset revenues loss give policymakers a lot of flexibility

- Estimates suggest Michigan may be able to use $6 billion of the federal funding for revenue loss alone, opening the door to a broader array of uses

As legislative leaders and the Whitmer administration begin meeting to finalize the Fiscal Year (FY)2022 budget, it is clear that Michigan is sitting on an unprecedented reserve of available revenue. Revised forecasts from last month’s revenue conference identified an extra $3.5 billion in state-generated revenue for budget writers to work with. In addition, Michigan awaits another $6.5 billion in one-time federal stimulus from the American Rescue Plan Act (ARPA) enacted in March. The federal funding will be available through the end of calendar year 2024.

Both the administration and legislature have begun laying out proposals to use some of the additional revenue to support new spending, a rainy day fund deposit, and tax relief. For example, Governor Whitmer has laid out plans to spend $664 million to eliminate the per-pupil funding gap between K-12 school districts and another $455 million to expand eligibility and provider capacity for the state’s Great Start Readiness preschool program.

The Republican-controlled legislature is actively considering tax relief options, including a corporate income tax rate reduction and expanded income tax reductions for retirement income. House Appropriations Committee Chair Tom Albert has proposed $595 million to pay the Flint water crisis settlement in full and avoid longer-term debt service costs. The House also approved spending $550 million to replenish the Unemployment Insurance Trust Fund balance, $400 million for water, sewer, and broadband infrastructure; and $385 million deposit to the state’s rainy day fund (Budget Stabilization Fund). On the Senate side, a supplemental introduced on Wednesday would allocate $1.6 billion for bridge repairs and rail crossing improvements.

While revenue is plentiful, the massive influx of federal stimulus comes with some restrictions that would appear to make it harder to achieve some of the items on these wish lists. The U.S. Treasury released additional guidance last month on the use of the ARPA funding, broadly allowing for: (a) assistance to combat the negative health and economic impact of the pandemic; (b) premium pay for essential workers; and (c) water, sewer, and broadband infrastructure projects.

The guidance also includes specific restrictions. For instance, it provides that funding cannot be directly deposited into states’ rainy day funds, and it prohibits using the federal dollars to pay off legal settlements or, as the Research Council lamented in a recent blog, to pay down unfunded pension liabilities.

However, a closer examination of the guidance suggests that state and local governments may still have wide discretion on the use of the funding. In addition to the three spending categories, recipients have discretion to use federal stimulus dollars to replace revenue losses arising from the COVID-19 pandemic. Here, the federal funds can be used to cover general budget needs, even those that fall outside the three main spending categories outlined above.

It also sets a pretty lenient standard in defining “revenue loss”. Treasury’s guidance defines the term as the difference between the amount of actual revenue collected and a calculated baseline amount that grows annually by at least 4.1 percent from levels prior to the pandemic. Michigan now forecasts state revenues rebounding to pre-pandemic levels, but annual growth is projected to be significantly less than 4.1 percent.

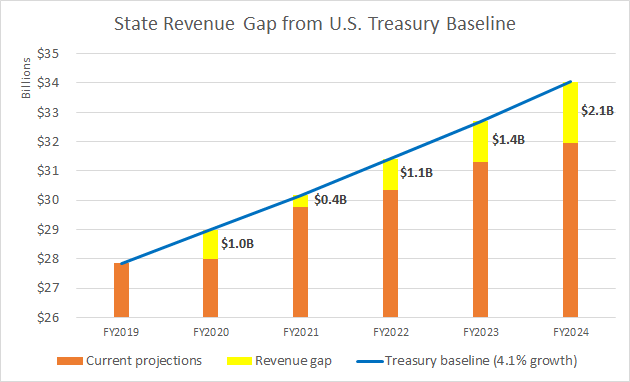

What could this mean for state budget deliberations? The table below estimates how much revenue replacement might be feasible for the State of Michigan. Per the federal guidance, FY2019 is used as the base year for these calculations. Total General Fund/General Purpose (GF/GP), School Aid Fund (SAF), and dedicated Transportation revenue for FY2019 was $27.8 billion. The blue trend line in the table maps out 4.1 percent revenue growth from the FY2019 base. The orange bars display current projections for GF/GP and SAF revenue and the most recently published projections of transportation revenue collections.

The amount of state “revenue loss” (highlighted in yellow) is the difference between the 4.1 percent baseline growth and current state revenue estimates. This approximates the amount of federal stimulus that can be used for discretionary revenue replacement in each future year. In short, we estimate that Michigan will have somewhere around $1 billion in federal stimulus to meet general budget needs this year alone.

Looking at future years, the cumulative estimated revenue gap between FY2021 and FY2024 is about $5 billion. This means that Michigan could use about $6 billion of its $6.5 billion ARPA allocation just to cover state revenue loss from the baseline trend.

It should be noted this analysis only covers a portion of Michigan’s “general revenue” that is applicable to these calculations under the Treasury guidance. The state will need to consider other revenue streams that fall outside the GF/GP, SAF, and transportation forecasts used above. State “general revenue” includes other big dollar items like tuition, room and board, and other charges paid to state universities as well as charges paid to university hospital systems. These other revenues will impact the bottom line “revenue loss” calculation to some degree.

Further, revenue loss under the Treasury process is calculated based on calendar year revenues, while our analysis relies on state fiscal year revenue estimates; this timing difference would also impact final amounts. Still, it appears very likely Michigan will have access to a substantial amount of discretionary federal stimulus revenue, over and above the $3.5 billion state revenue revision.

The magnitude of the potential revenue loss could have important implications for final budget decisions – both the near-term decisions on the FY2022 budget and on future budget decisions. Where federal ARPA dollars cannot be spent directly for certain purposes, they can instead be used for “revenue loss”, effectively freeing up state-generated General Fund revenue to be used for those same purposes. And if these one-time ARPA fund shifts are reserved to cover one-time spending priorities, this can all be done without creating any new long-term structural budget problems. That could create a path for budget “wins” for all sides, allowing state budget writers to make a sizable rainy day fund deposit, pay off the Flint legal settlement, or pay down pension system debt without cutting into discretionary ongoing revenue available for other things like expanded pre-school, tax relief, or the K-12 foundation allowance.

And the added spending flexibility with ARPA dollars that are tied to covering revenue loss means that potential one-time budget needs, like road maintenance and other infrastructure improvements, are back on the table as eligible direct expenses for the federal dollars.

So, despite the general restrictions on spending the new ARPA dollars, the process established to determine eligible revenue loss appears to give Michigan tremendous latitude in spending its $6.5 billion federal allocation and opening up possible avenues for budget writers to pursue a much broader menu of fiscal demands.