July 28, 2026

In a nutshell

- For the 11th year in a row, the City of Detroit’s General Fund revenues exceeded expenditures.

- Income tax revenue has consistently exceeded expectations but year-over-year increases are likely to moderate.

- The city spent less than planned in FY2023, in part, these lower expenditures are the result of fewer employees than desired.

Just before December ended, the City of Detroit published its Fiscal Year (FY)2023 basic financial statements. (The city’s fiscal year runs from July 1 to June 30.) Basic financial statements—the balance sheet, income statement, and cash flow statement—provide information to elected officials, public administrators, citizens, and creditors. The city’s FY2023 basic financial statements confirm the city’s recovery from bankruptcy and the partial success of the second comeback that it and other cities have had to pull off to recover from the COVID-19 pandemic. There are also indications that revenues will flatten and that annual surpluses—a turnaround from chronic deficits incurred pre-bankruptcy—may partially be explained by an inability to attract and retain employees.

This research note focuses on a few areas, chosen for salience, that speak to the city’s continued ability to service its citizens and its debts. In brief, this research note analyzes annual surpluses and the balance of the city’s General Fund (the city’s primary “account”), income tax revenue, and employee attraction and retention.

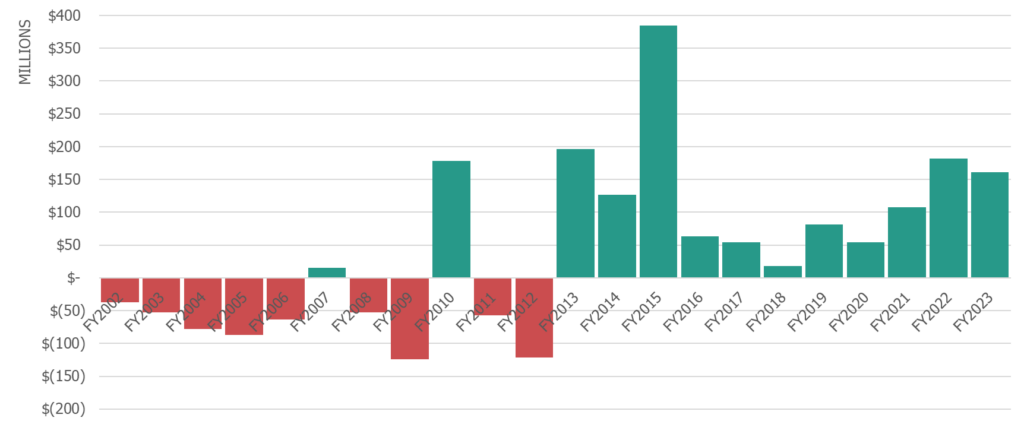

A streak of post-bankruptcy annual surpluses remains unbroken

Cities are not businesses. But if Detroit were a business, it would be profitable. For the 11th fiscal year in a row, General Fund revenues exceeded expenditures. The city reported a $161.2 million annual surplus on its income statement.

Chart 1

City of Detroit General Fund surpluses and deficits, FY2002–FY2023

Source: City of Detroit’s Annual Comprehensive Financial Reports

Generally, the city has retained these “profits” rather than spend them in the fiscal year that follows. The General Fund accumulated surplus or fund balance—the result of annual surpluses saved up—equaled $1.2 billion at the end of FY2023. Essentially fund balance equals assets minus liabilities, i.e., the public sector equivalent of net worth. In the city’s case, a substantial part of this net worth is restricted.

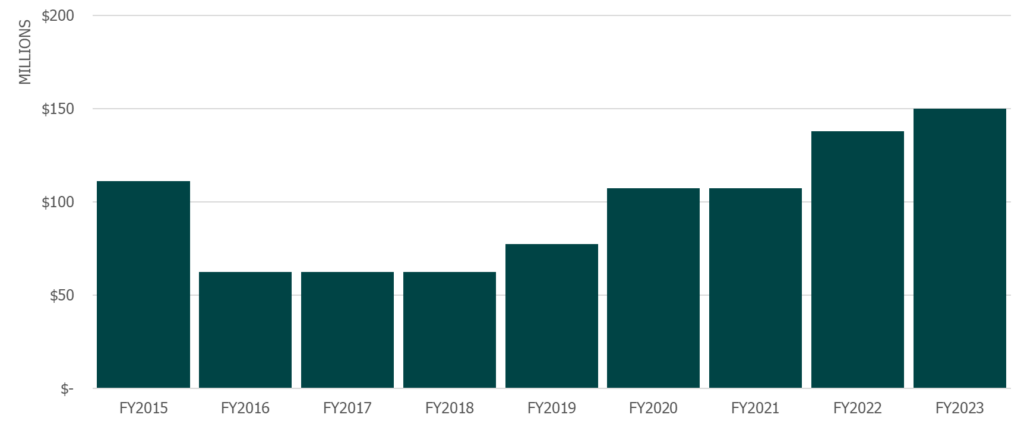

For example, the city’s budget reserve had a reported balance of $150 million. The city is required by state law to maintain a budget reserve equal to five percent of projected General Fund expenditures, a threshold it had already achieved and exceeded. In FY2022, the budget reserve had a reported balance of $138 million, or 13.1 percent of projected General Fund expenditures. In FY2023, another $12 million was deposited. As of the FY2024 budget, the budget reserve equaled 11.4 percent of projected General Fund expenditures. (The city saved more, but also spent more, which is why even with the added deposit budget reserves declined relative to projected General Fund expenditures).

Chart 2

City of Detroit General Fund budget reserve balances, FY2015–FY2023

Source: City of Detroit’s Annual Comprehensive Financial Reports

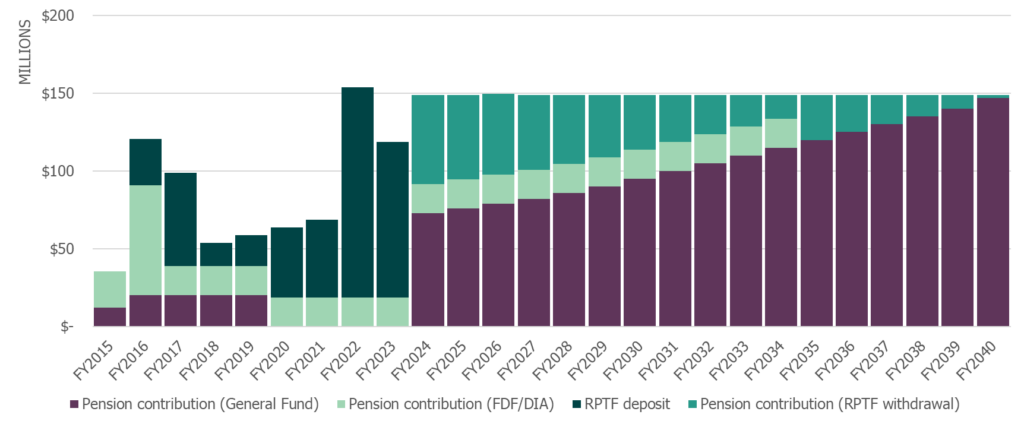

In addition to deposits made to the budget reserve, the city made a $100 million deposit to its Retiree Protection Trust Fund (RPTF). The RPTF is an irrevocable trust created in preparation for the need to make pension fund contributions paused in bankruptcy and scheduled to resume in FY2024. FY2024 is the first fiscal year in a decade that the city will have to make actuarially determined contributions to two pension plans that were closed in bankruptcy. It is well-prepared to do so. (“Closed” means that the pension plan is closed off to new employees and benefits are frozen and attendant pension liabilities—the actuarial value of contractual promises to provide employees income in retirement—are also frozen.)

The RPTF has a balance of $465.4 million. An initial withdrawal of $57 million is scheduled in FY2024 to offset a projected pension fund contribution of $148.7 million. (A victory in federal court last year means that the pension fund contribution may be less than what was projected.) Like the budget reserve that is intended to protect the city from economic downturns and disasters, the RPTF is intended to protect the city from spikes in pension costs. The city’s pension fund contribution is, in part, a function of investment returns: the more money earned from invested pension fund assets, the less is demanded from the city. If pension fund assets earn a return less than expected (6.75 percent annually) or incur losses, more is demanded from the city so that promised benefits may be paid out to retirees on time and in full.

Chart 3

City of Detroit Pension contributions and RPTF deposits and withdrawals, FY2015–FY2040

Source: City of Detroit’s Annual Comprehensive Financial Reports

As the market moves up and down, so too will the city’s pension fund contributions. The RPTF provides the city with means to smooth its contributions out across the amortization window. Absent the RPTF, additional pension fund contributions would draw resources away from current services.

To some extent, the city’s preparedness for spikes in pension costs is understated. While the budget reserve is intended to help the city weather economic downturns and disasters, it can be used to make pension fund contributions. If the balances of the budget reserve and RPTF are combined, the city has $615.4 million available to make pension fund contributions. Further, this tabulation may still understate the resources available because it excludes the unrestricted portion of the General Fund accumulated surplus.

Even in the nascence of the COVID-19 pandemic and a recession that looked to be deeper than the “Great Recession,” the city did not draw down its budget reserve. It instead relied on the unrestricted portion of the General Fund accumulated surplus. In FY2023, the unrestricted fund balance amounted to $146.1 million. The unrestricted fund balance has exceeded $100 million since FY2016.

To be sure, there is an opportunity cost to this treasure. The city could have used that money to improve services, invest in its infrastructure, or address its various social ills. These excess resources allow the city to weather economic downturns (or pandemics) better than most, however.

In its FY2024–FY2027 Four-Year Financial Plan, annual surpluses are anticipated to turn into annual deficits—planned as the city draws down the RPTF balance. Still, the city is well-positioned to handle unforeseen costs and will be supported by year-over-year increases in revenues, even if those increases are smaller than prior years.

Income tax revenue increases, even more than expected

In FY2023, the city collected $1.3 billion in General Fund revenue—$76.8 million, or 6.3 percent, more than what was collected in FY2022. It also was more than the $1.2 billion projected at its February 2022 Revenue Estimating Conference—projections that provided the basis for the FY2023 budget.

Of the city’s major sources of revenue, the income tax most outperformed expectations. The city collected $408.1 million in income tax revenue—$33.4 million, or 8.9 percent, more than what was projected. Income tax revenue has consistently experienced the most substantial year-over-year increases post-bankruptcy, and an analysis of income tax tells a story about the city’s economy.

Like the homes, offices, and factories that make up the property tax base, employment and corporate profits are essentially the base for the city’s income tax. Consequently, when combined with other economic metrics, like the unemployment rate, income tax collections may be used as a shorthand basis by which to appraise the city’s economy.

In February 2020, immediately before COVID-19 shut down the world, the city projected it would collect $1.7 billion in income tax revenue across FY2020–FY2024. Income tax collections trickled into the treasury in FY2020. Instead of the $329.8 million in expected income tax revenue, $290 million was collected—$39.8 million less. FY2021 income tax collections also underperformed expectations set in February of 2020. It was not until FY2022 that income tax collections returned to historical trends, and exceeded those expectations set in February of 2020. FY2023 income tax collections further confirm the return to historical trends.

Even with the return to historical trends, once projected year-over-year increases in income tax revenues are adjusted for inflation, it may be that increases moderate. In April of 2023, the city’s unemployment rate fell to 4.2 percent—the lowest unemployment rate recorded since the dataset was launched in 1990. However, the unemployment rate has increased over the past few months, and as of November of 2023 (the most recent data available), the preliminary estimate is an 8.2 percent unemployment rate. The unemployment rate does not, in and of itself, forecast doom.

Income tax paid by non-residents who work within the city are the primary payers, and the city’s unemployment rate does not reflect their fortunes. Still, increases in the unemployment rate are worrisome. The monthly financial reports produced by the city may also provide a means to monitor the city’s economy. Between FY2018 and FY2023, the city collected a mean of $28.2 million in income tax revenue per month. If monthly income tax collections are measured relative to revenue projections, typically 39 percent of projected revenue was collected by November. In its November financial report from the previous year (the most recent monthly financial report available), $24.9 million was collected, $143.4 million year-to-date, or 37 percent relative to what was projected—only minimally below the mean.

If income tax collections fall short of expectations, the city has another four major sources of revenue to rely on. Equally, if total revenue falls short of expectations, it is likely that the city will underspend. The city’s personnel costs are the most expensive line item, and the actual number of people employed by the city has been less than what was allotted for in recent city budgets.

Fewer employees who demand a paycheck means lower personnel costs

In FY2023, the city appropriated resources to support 10,513 FTE (full-time equivalents). Based on the FY2023 basic financial statements, the city had 9,805 FTE. The number of FTE in FY2023 is a marked increase from FY2013, when scarce resources forced the city to lay off employees. In FY2013, the city had 8,912 FTE, which was a sharp reduction from the 16,949 FTE employed by the city in FY2004. So while the city’s workforce has recovered from bankruptcy, it is still below earlier years.

On a per capita basis, the diminishment of the city’s workforce is less pronounced, as the city’s population also fell. A decade ago, the city had a population of 706,663 (based on the 2013 American Community Survey). At that time, for every 1,000 residents, the city had 14 FTE. In 2022 (the most recent population estimates available), the city had 636,787 people and 17 FTE per 1,000 people. So, there are more public servants to serve the public in absolute and relative terms. Yet, the city has fewer employees than it would ostensibly prefer, and that may constrain personnel costs.

Conclusion

The city’s FY2023 basic financial statements confirm a continued recovery from bankruptcy and the COVID-19 pandemic. It collected more in revenue than what was projected and spent less than it had planned. The latter may represent an inability to retain and attract workers rather than prudence. Consistent annual surpluses are a positive development but may indicate an operational flaw and future analyses should determine not just whether the city ran an annual surplus or a deficit but examine why.