July 27, 2026

In a nutshell

- Detroit could reduce its reliance on property tax revenue and increase its reliance on income tax revenue to finance city operations.

- Further reliance on income tax revenue will increase revenue volatility.

- Additional revenue volatility may be addressed by healthy reserves.

In my last post, I laid out the possibility that the City of Detroit could cut its property tax rate and increase its reliance on income tax revenues to finance operations. Current property tax rates are a deterrent to homeownership and development and property tax revenue, as a share of total General Fund revenue, has declined in importance post-bankruptcy. Income tax revenue on the other hand has increased in importance post-bankruptcy and is, in part, what has enabled the city to run surpluses each fiscal year since (FY)2013. These surpluses can facilitate a shift away from reliance on property tax revenue to income tax revenue.

The city publishes monthly financial reports, and in June, issued a preliminary estimate of a $130.1 million year-end surplus for FY2023 (the city operates on a July 1 to June 30 fiscal year). Because a shift toward reliance on income tax revenue would add volatility to total anticipated revenue, and therefore threaten the sustainability of services financed by that revenue, surplus monies should be deposited into the city’s budget reserve and used to smooth out annual ups and downs.

Challenges associated with revenue volatility

Revenue volatility can threaten service delivery sustainability. Sustainable services, those expenditures that recur each fiscal year, should be matched by revenues that are expected to recur. Otherwise the city will find itself in the untenable position that it was in pre-bankruptcy, when it ran deficits in seven out of the ten fiscal years that preceded bankruptcy. So added volatility in total anticipated revenue could make it difficult to improve, or even plan and maintain, essential services year to year.

Income tax revenue is more volatile than property tax revenue. Income tax revenue more or less rises and falls with the rate of employment and income earned by businesses, residents, and non-residents who work in the city. Property tax revenue is less responsive to year-to-year economic conditions. Property values tend to rise over time—the exception of the Great Recession aside. Even in periods of recession, property values often remain stable, and may even increase. Based on the S&P/Case-Shiller MI-Detroit Home Price Index, home values increased by 2.7 percent in the recession that followed a fall in tech company stocks in the early 2000s, and rose by 0.2 percent in the COVID-19 pandemic recession.

If Detroit’s elected officials decide to cut tax rates to reduce the city’s reliance on property tax revenue to finance operations, then they should also adopt a policy to deal with the added revenue volatility that would accompany further reliance on the income tax. Here California offers some lessons. California has been called a land of boom and bust. In part, that reputation is attributable to the state’s reliance on income tax revenue and consequently the fortunes of its ultra-wealthy residents—Hollywood stars, venture capitalists, and Silicon Valley entrepreneurs.

Between FY2002 and FY2021, income tax revenue comprised 59.9 percent of California’s General Fund revenue. Comparatively, income tax revenue comprised 23.8 percent of Detroit’s General Fund revenue over the same period. California’s General Fund revenue was more volatile in those two decades.

From FY2002 to FY2021, California’s General Fund revenue volatility rate was 8.7 percent. For the purpose of this research note, revenue volatility is measured as the year-over-year increase or decrease in revenue, and specifically defined as the absolute mean of year-over-year fluctuations (without consideration of the direction of the fluctuations, up or down). The maximum year-over year increase was 26.3 percent between FY2020 and FY2021; and the maximum year-over-year decrease was a 13.9 percent drop between FY2008 and FY2009. Income tax revenue was relatively more volatile than General Fund revenue overall. Over the same period, the revenue volatility rate for California’s income tax revenue was 10.2 percent. Income tax revenue experienced its most impressive increase between FY2010 and FY2011 (17.9 percent); and suffered the worst dip between FY2008 and FY2009 (17.6 percent).

The revenue volatility experienced by Detroit was less than that of California. The city’s General Fund revenue volatility rate was 5.6 percent from FY2002 to FY2021. In those two decades, the maximum year-over-year increase (11.4 percent) was smaller than that experienced by California, and the maximum year-over-year decrease (12.4 percent) was smaller too. Detroit’s income tax revenue was less volatile than California’s, but still more volatile than the city’s General Fund revenue overall. Over the two-decade period, the city’s income tax revenue volatility rate was 6.4 percent. The most impressive increase in income tax revenue occurred from FY2019 to FY2020 (16.4 percent), followed by an equally impressive fall from FY2020 to FY2021 (19.5 percent).

A rainy-day fund makes economic storms less severe

If Detroit reduces the property tax rate in favor of more reliance on income tax revenue, it should undertake measures similar to the California practice to deal with added revenue volatility.

Proposition 58, passed by California voters in 2004, required the state to make annual deposits into a Budget Stabilization Account equal to one to three percent of General Fund revenue until the reserve balance reached $8 billion or five percent of General Fund revenue (whichever was more). It was superseded by Proposition 2 in 2014. Championed by twice-Governor Jerry Brown, Proposition 2 requires the state to annually set aside 1.5 percent of General Fund revenue in addition to excess collections from taxes on capital income. Monies set aside are then split between debt payments and reserve deposits. As of the FY2024 operating budget, $22.3 billion will be held in the Budget Stabilization Account or 10.7 percent of General Fund appropriations.

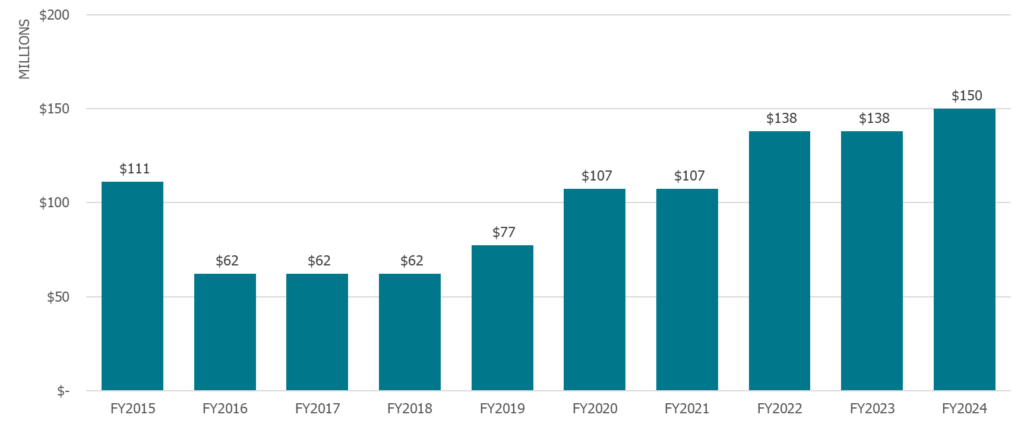

The amount held in California’s reserve is nearly identical—as a proportion of General Fund appropriations—to what is held in Detroit’s reserves. Based on the FY2024 operating budget, the city will have set aside $150 million, or 11 percent of General Fund appropriations. While it would exceed what is already mandated by state law (five percent of General Fund expenditures), the city should use some of the estimated $130.1 million surplus accrued from FY2023 to increase the reserve balance. (See Chart 1)

Chart 1

Actual and Projected Year-End Balances of the City of Detroit’s Budget Reserves, FY2015 to FY2024

Informally, the reserve balance could be affixed to some equivalence of the mean of General Fund expenditures across the city’s multi-year financial plans. For example, across the four fiscal years of the city’s FY2024 to FY2027 financial plan, mean General Fund expenditures equal $1.3 billion. The city could increase the aim to 15 to 20 percent of mean General Fund expenditures. To increase the reserve balance until it is equal to 15 or 20 percent of mean General Fund expenditures, it would require an added $51.4 to $118.6 million. Additional deposits would increase the reserve balance to between $201.4 and $268.6 million.

Why would the city add more money to the reserve when there are current demands on the city’s resources, such as pension contributions, added pay for police officers and bus drivers, and infrastructure improvements? Each deposit to the reserve represents opportunity cost, and the cost is an inability to address citizens’ needs and concerns in the here and now. Reserves secure the city’s financial position, however.

City services, specifically the continuity of those services, are protected by reserves. In the early phase of the COVID-19 pandemic, the city canceled capital projects and temporarily laid off employees to overcome a $116.5 million shortfall between projected and collected revenue. Many of these fiscal maneuvers, detrimental to service delivery sustainability, could potentially be avoided in the future if the city continues to fortify its financial position with reserves.

Conclusion

A shift from reliance on property tax revenue to income tax revenue would make the city’s financial position more subject to the economic cycle of booms and busts. Like California, Detroit may prepare for that added turbulence with additional reserves. Greater reserves protect current services, and provide the city an opportunity to alter how the social contract is financed by Detroiters.