July 6, 2026

Update (3/17/23): Following the publication of this blog, the Michigan House passed its own legislation (House Bill 4039 and 4137) exempting delivery and installation charges from Sales and Use Taxes. The House-passed bills, however, incorporate an important change from the bills introduced in the Senate by removing the exemption for charges related to utility sales (e.g., electricity, natural gas). That change reduces the GF/GP revenue loss from the estimated $250 million (as cited in the blog) to around $60 million. There are indications that this change reflects the final agreement on the legislation. This development means that Executive Budget spending proposals will need to be pared by back around $400 million, rather than $600 million.

In a Nutshell

- The Governor recently signed legislation implementing major elements of her income tax reform proposals; but lack of “immediate effect” means her $180 tax rebate proposal won’t happen.

- That same lack of “immediate effect” also means an income tax rate cut is likely on its way.

- That rate cut and another pending sales and use tax exemption will put a dent into the revenue available to fund the Governor’s budget proposals; we estimate at least $600 million of her proposed budget investments could get crowded out of the final FY2024 budget to bring planned spending in line with estimated revenue.

State policymakers began crafting next year’s budget with the comfort of surplus resources that provided the ability to finance both tax relief and tackle spending priorities. A month into the process, the long-term revenue outlook is a little murkier and it appears that ambitions for some spending priorities will have to be scaled back; and a once-forgotten provision triggering an income tax rate rollback is the linchpin for all of this uncertainty.

Two weeks ago, the Research Council presented its annual webinar analyzing the Governor’s Fiscal Year (FY)2024 budget request; but as of that morning, a major question mark remained regarding the implementation of major new tax policy proposals. House Bill 4001 – which contained elements of the Governor’s tax plan including a large tax cut for many retirees; an expanded state Earned Income Tax Credit; and the redirection of Corporate Income Tax revenue for new economic and community development purposes – had already been approved by both chambers of the legislature.

However, rather than sending the bill to the Governor for her signature, the legislature was still holding it. The major hitch was the bill had not been granted “immediate effect” by the legislature. As such, the bill would not legally take effect until 90 days after the end of the 2023 legislative session – which could be as late as March 2024. Granting a bill immediate effect – and thus avoiding the wait – requires the support of two-thirds of the members of each chamber.

And immediate effect was critically important to another key element of the bill: a redirection of $800 million in Corporate Income Tax (CIT) collected in FY2022 to help finance one-time income tax rebates of $180 per taxpayer household. Beyond paying for the tax rebates, that $800 million fund shift from the state’s General Fund also had a secondary impact: it would cancel out an automatic income tax rate cut that otherwise appears to be on the horizon.

Within twelve hours of our webinar, however, the picture had become at least a little clearer. Democratic leadership in the legislature punted on immediate effect and sent the bill to the Governor without it; and Governor Whitmer then signed the bill into law on March 7.

So, what does this all mean now for the income tax rate cut and the $180 rebates? And how will this development affect revenue available to fund the FY2024 state budget? Here is what you should know as budget deliberations move forward.

An Income Tax Rate Cut is Coming… Probably

Way back in 2015, the then-Republican controlled legislature approved a series of bills designed to generate an additional $1.2 billion in annual road funding. One of those bills dedicated $600 million in annual income tax revenue to road work. Another bill added an income tax rate “trigger” formula that effectively reduces the income tax rate whenever state General Fund revenue grows sufficiently faster than the general inflation rate.

Back in January, the two nonpartisan legislative fiscal agencies issued revenue forecasts that indicated that unusually strong FY2022 General Fund growth would effectuate this trigger, likely bringing the income tax rate from its current 4.25 percent down to something around 4.05 percent. As noted above, the Governor’s proposed CIT fund shift to cover tax rebate costs, by reducing FY2022 General Fund/General Purpose (GF/GP), would have effectively shut down the triggered rate cut. But for the fund shift to work, those provisions would need to become law before the state closes its financial books on FY2022.

That’s where the issue of immediate effect for House Bill 4001 became so important. Unlike in the House, Senate rules require record roll call votes on immediate effect. That means 26 of the chamber’s 38 Senators would need to support immediate effect; given the current partisan alignment of the Senate, that would require support from all 20 Democrats and another 6 Republicans. But only the 20 Democratic Senators actually voted in support of immediate effect.

Now that House Bill 4001 has been signed without immediate effect, two things become clearer:

- There will be no $180 one-time rebate checks to Michigan taxpayers this year

- The income tax rate for tax year 2023 will drop… probably to something around 4.05 percent

Still, one hurdle needs to be cleared to make this all official. The state will soon publish its Annual Comprehensive Financial Report to finalize the GF/GP revenue amount that’s used as part of the rate cut calculation. With a final revenue number in hand, the exact size of the rate cut can be determined. In all likelihood, that new rate will be very close to 4.05 percent. Only a major surprise – a significant audit finding or change in accounting rules affecting GF/GP revenue – could have a more substantial impact on size of the rate cut, and this seems unlikely. Typically, the report is published in March, so the issue should be settled in the coming weeks.

Budget Implications of the Income Tax Rate Cut (and Another New Proposal)

As we noted in our webinar analysis, the Governor’s budget proposal includes $1.0 billion in new ongoing GF/GP spending and another $1.9 in one-time spending initiatives for FY2024. Further, her budget proposal assumes around $1.3 billion in GF/GP revenue reductions per year in FY2023, FY2024, and FY2025 related to the exemption of certain retirement and pension income from the State Income Tax; the expansion of the state’s Earned Income Tax Credit; proposed redirections of Corporate Income Tax revenue; and other smaller credits (see our webinar for details). However, her budget does not build in a permanent income tax rate cut, and the Senate Fiscal Agency estimates that cutting the income tax rate from 4.25% to 4.05% will come at the cost of around $430 million in GF/GP revenue in FY2023, and then $650 million per year thereafter.

Further, another tax reduction appears to be on the horizon as the Governor and legislative Republicans have apparently struck a deal to exempt certain delivery and installation charges included in the price of a product from the state’s Sales Tax and Use Tax. The Senate Fiscal Agency estimates that change will reduce GF/GP revenue by around $250 million per year once fully implemented.

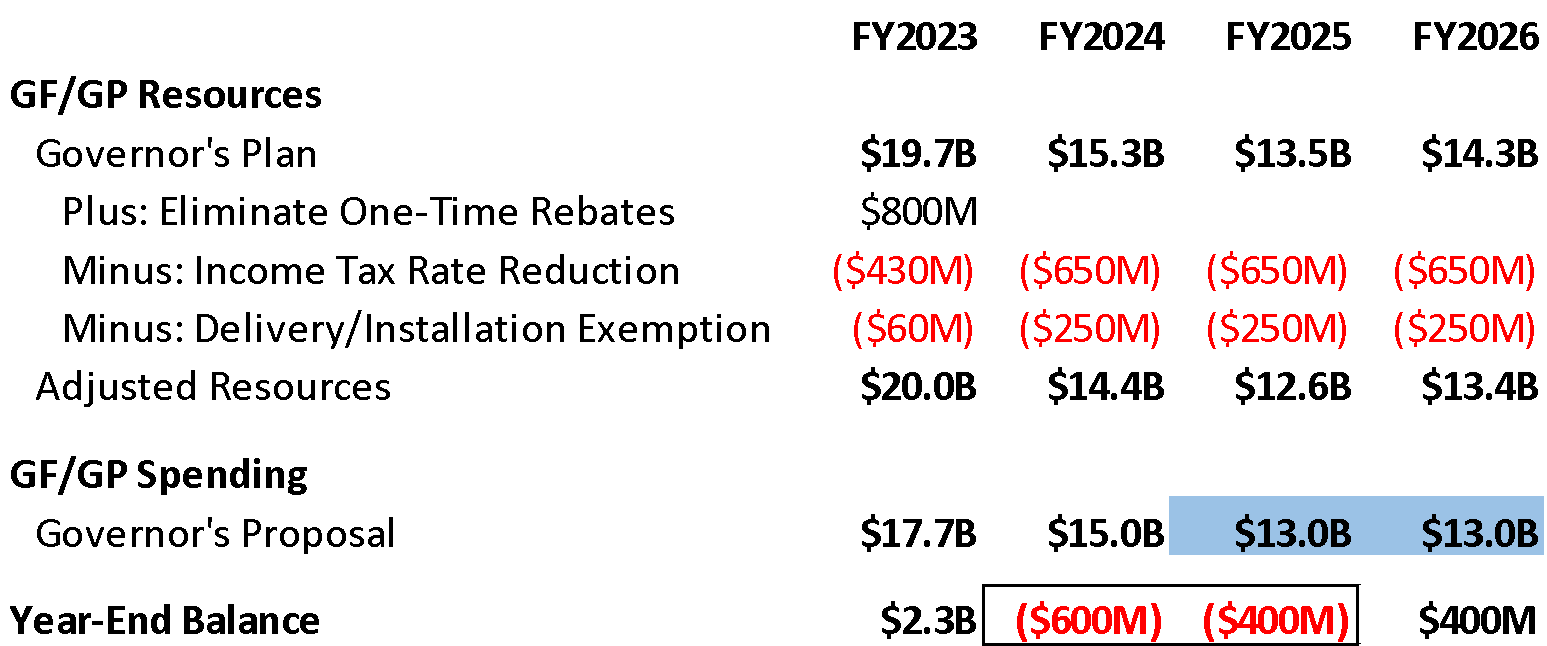

What does that mean for the Governor’s FY2024 budget proposal? In short, it means the Governor’s spending proposal will need to be trimmed back. The table below compares total GF/GP revenue resources with the Governor’s spending proposals. GF/GP resources in this context include annual revenue collections plus any one-time fund balances carried in from the prior year; that explains why resources are higher in FY2023 and FY2024, while substantial fund balance reserves are still in place. In terms of spending, the table shows the Governor’s specific spending proposals for FY2023 and FY2024; for the out-years (shaded in blue) the amounts reflect ongoing GF/GP spending (i.e., one-time spending proposals are removed) that would be needed to maintain her FY2024 budget going forward.

Long-Term GF/GP Budget Outlook With New Tax Reductions

Source: Research Council calculations based on revenue and spending information from House Fiscal Agency and Senate Fiscal Agency; impact of income tax rate reduction and delivery/installation exemption based on Senate Fiscal Agency estimates

While GF/GP resources actually increase in FY2023 with the cancellation of the income tax rebates, the combined impact of the income tax rate reduction and installation/delivery charge exemption reduces resources in the long run. The table shows the end result: GF/GP resources are about $600 million short of the Governor’s $15 billion FY2024 spending proposal, a gap of about four percent.

That means that as the legislature deliberates on the budget, the Governor’s proposal will need to be pared back by at least $600 million. That could come from reducing or eliminating some of her new ongoing or one-time spending initiatives; or it could mean cutting out existing services that are already in the budget. Further, it also means any new spending added by the legislature will have to come out of one of those pots as well. Assuming continuation of current tax policies and spending amounts, it’s not until FY2026 , when most of the Governor’s proposed redirections of Corporate Income Tax revenue expire, that the budget is once again balanced.

Still, in the big picture, ongoing GF/GP spending in the FY2024 budget will be significantly larger than it was in FY2023. Significant room remains to implement many of the Governor’s budget enhancements; but the tax reductions will mean those enhancements will need to be prioritized, with some items being left out of the final budget.

One last note: this analysis assumes the income tax rate cut arising from the trigger is permanent. That certainly seems consistent with the legislative intent back in 2015. However, some legal experts have argued that the statutory language that establishes the income tax rate trigger isn’t clear as to whether triggered rate cuts are ongoing in nature. That’s significant because the budget impact discussed above largely goes away if the income tax rate is cut only for tax year 2023 and then returns to 4.25 percent in 2024.

And that determination won’t necessarily be made until next year, leaving some additional uncertainty on the table.

Stay tuned.