Michigan is among a few states that rely heavily on the practice of dedicating, or “earmarking”, state tax revenue to specific purposes. While this practice safeguards funding for select public services from changing political climates, earmarking encumbers the ability of state lawmakers to carry out the task most essential to their job responsibilities.

Michigan is among a few states that rely heavily on the practice of dedicating, or “earmarking”, state tax revenue to specific purposes. While this practice safeguards funding for select public services from changing political climates, earmarking encumbers the ability of state lawmakers to carry out the task most essential to their job responsibilities.

A substantial amount of the state’s financial resources are already allocated to specific purposes before Michigan lawmakers begin the annual budgeting process. Of the total $53 billion State of Michigan Fiscal Year 2015 (FY2015) spending plan, almost 42 percent is financed by federal funds that are directed to specific purposes and over which state officials have little or no discretion. While the remainder of the budget is financed by state revenues, including various taxes and fees, a hefty portion is designated for specific functions or programs either by the state constitution or statute.

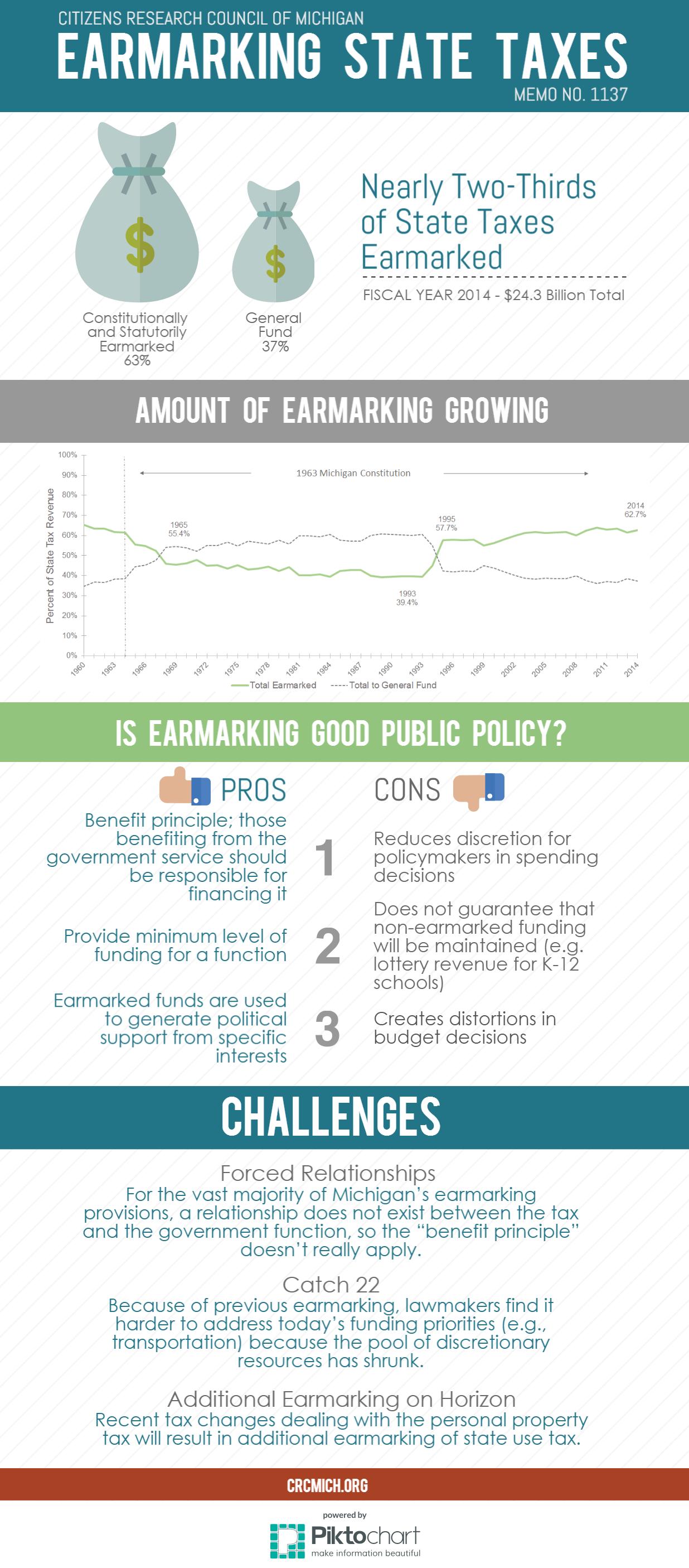

The Proposal A school finance reforms of the mid-1990s increased the amount of earmarking from 40 percent of state tax revenue in FY1993 to 58 percent in FY1995. Since that time, additional state budget resources have been dedicated to specific functions. In FY2014, nearly 63 percent of the total $24 billion collected from major state taxes was dedicated to specific functions. This means that almost two-thirds of the state tax revenue has been effectively removed from budgetary decision-making. Michigan has not seen this current level of tax earmarking since before the adoption of the 1963 Michigan Constitution.

The Proposal A school finance reforms of the mid-1990s increased the amount of earmarking from 40 percent of state tax revenue in FY1993 to 58 percent in FY1995. Since that time, additional state budget resources have been dedicated to specific functions. In FY2014, nearly 63 percent of the total $24 billion collected from major state taxes was dedicated to specific functions. This means that almost two-thirds of the state tax revenue has been effectively removed from budgetary decision-making. Michigan has not seen this current level of tax earmarking since before the adoption of the 1963 Michigan Constitution.

Earmarking of some taxes, such as transportation taxes, structures the taxes as a user fee; those benefiting from the government service are responsible contributing to the financing of it. Although transportation spending is the beneficiary of earmarked fuel and motor vehicle tax revenues, the growth of these revenues has failed to keep pace with the investment levels necessary to maintain the system. At the same time, lawmakers have been hesitant to supplement the dedicated funds with discretionary funding. Until recently, lawmakers have simply adopted the earmarked level of spending without attempting to address the actual financial needs of the system. And when lawmakers have decided to supplement the earmarked funding, they have found that the pool of discretionary funding from which to draw, as a share of the total, is much smaller because of other dedications. This has made designing a fiscal plan to re-prioritize state spending to address Michigan’s crumbling roads much more difficult.

For many of Michigan’s general taxes (e.g., sales, income, property), no clear relationship exists between the revenue source and the dedicated purpose. Earmarking takes decision making responsibilities out of the hands of those elected to make such decisions. The legislature’s “power of the purse” is effectively diminished. With proportionately fewer discretionary resources available to them, budget writers find it more difficult to reallocate funding according to shifting priorities. The current transportation funding debate illustrates many of the challenges arising from earmarking.