February 7, 2024

In a nutshell:

- Detroit has the most diversified local tax structure in the state with exclusive access to higher tax rates and more tax options.

- Despite this diversified tax structure, Detroit levies property taxes at high rates compared to other cities in Michigan, which creates a disincentive for people and businesses to locate in Detroit.

- Expansion of local-option taxes in Detroit could allow the city to lower its high property tax rate, further diversify its revenue base, and levy taxes that can better grow with an expanding economy.

Our recent report shows that Detroit is really an anomaly in the state when it comes to local-option taxes because it has authorization to levy more types of local taxes than any other local government in the state. How ever, local tax diversity alone cannot ensure fiscal health, which is affected by a number of factors, including local tax structure and local tax capacity, state and federal revenues and policies, legacy costs, service levels, and local service delivery costs and structures. Despite a fairly diversified local tax structure, Detroit continues to face fiscal problems.

ever, local tax diversity alone cannot ensure fiscal health, which is affected by a number of factors, including local tax structure and local tax capacity, state and federal revenues and policies, legacy costs, service levels, and local service delivery costs and structures. Despite a fairly diversified local tax structure, Detroit continues to face fiscal problems.

Detroit is unique: current local-option taxes

Among Michigan municipalities, Detroit is in a category of its own: it is the state’s largest city by far with over 672,000 residents and the state’s biggest city with a geographic size of nearly 139 square miles. Detroit’s population peaked in 1950 at 1.86 million residents; in the years since, the city has experienced decreases in city resources, increases in crime and violence, racial and financial tensions with its surrounding suburbs, and a municipal bankruptcy in 2013. Detroit’s city government revenue base is much more diverse than many other local governments in the state partly because the state has come to Detroit’s aid as it has dealt with issues such as population and tax base loss.

In Fiscal Year (FY) 2017, Detroit levied a property tax, income tax, utility users’ excise tax, and casino gambling tax. Detroit’s property tax levy in 2017 was 31.46 mills for operations and debt; with property taxes levied by overlapping governments too, city residents paid over 72 mills in total. The state average for city property taxes in 2017 was 17.25 mills with an average of 46.38 mills in total taxes paid by city residents to all local units. Detroit levies property taxes at high rates to compensate for the exodus of people and businesses from the city, which has eroded the property tax base, creating a relatively low taxable value per capita. Detroit also levies the highest city income tax in the state at a rate of 2.4 percent on residents and 1.2 percent on nonresidents. Twenty-two other cities (out of a total of 276 cities) also levy income taxes, most at rates of 1.0 percent on residents and 0.5 percent on nonresidents.

Detroit levies a five percent tax on the privilege of consuming public telephone, electric, steam, or gas services. This tax was authorized to the city originally to support the police budget; the law was amended to allow the tax to support both the city lighting authority and police budget. Finally, the city levies a 10.9 percent casino gambling tax, plus some additional fees from the casinos to help pay for public safety and other needs.

Why does Detroit continue to have revenue problems?

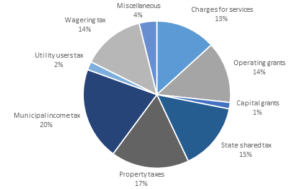

Even though the city levies more types of local taxes than other cities and receives the highest dollar amount of state revenue sharing, it continues to face fiscal challenges related to local revenues. The chart below shows FY2016 Detroit revenue by source in the city’s general fund and all other governmental funds. Local-option tax revenues make up approximately 53 percent of all revenue into the general fund, and state shared taxes and revenue make up another 15 percent.

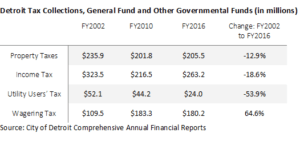

Despite its diversified tax structure, most of the major revenue sources for Detroit have declined in recent years. From FY2008 to FY2015, taxable values in Detroit declined by 27.3 percent, state revenue sharing payments declined by 21.8 percent, and city expenditures dropped by 8.4 percent. As the table below illustrates, all city tax revenue except casino gambling taxes declined from FY2002 to FY2016.

From FY2002 to FY2010, Detroit’s income tax revenue and rate declined (from 2.6 to 2.5 percent respectively). This decline in city income tax revenue corresponded with the cyclical economic declines caused by Michigan’s single state recession and the Great Recession. With the recovering economy, Detroit’s income tax revenue actually increased from FY2010 to FY2016 despite the tax rate decreasing from 2.5 to 2.4 percent.

The real estate and property value collapse during the Great Recession contributed to Detroit’s property tax revenues declining from FY2002 to FY2010. Since the Great Recession, property tax revenues have increased slightly from FY2010 to FY2016, but they remain below FY2002 levels. Detroit levies the property tax at a very high rate due, at least partly, to the fact that the city has a very low taxable value per capita ($8,918 in 2017 compared to a state average of $33,675).

The table above highlights the fact that most of the city’s local income sources have been declining in recent years. One potential way to help the city improve its local revenue capacity is to provide some property tax relief thereby encouraging more people to move to and open businesses in Detroit.

In order to provide property tax relief, Detroit needs more local tax options

Since emerging from bankruptcy, Detroit, and certainly the downtown area, appear to be experiencing a renaissance. That being said, the city faces many hurdles, including those related to local taxes and fiscal solvency.

One issue to be addressed is the city’s prohibitively high property tax rates. Expansion of local-option taxes in Detroit could allow the city to lower its property tax rate in order to spur investment and increase the city’s appeal to potential residents and businesses, as well as further diversify the city’s revenue base. The city could potentially benefit from taxes that would grow as the city becomes a destination to be visited again. Few other taxes alone are capable of yielding the amount of revenue produced by the property tax.

One tax source that can yield a large sum of revenue with a fairly low rate is a local-option sales tax. However, a local-option sales tax can be problematic for a number of reasons, the most important being the fact that the state Constitution is unclear as to whether the state would even be allowed to authorize local units to level a local sales tax. If the Constitution prohibits a local sales tax, then it would take a constitutional amendment, which requires a statewide vote of the people, to allow for one.

Lowering the local property tax rate in Detroit may require the city to levy a number of new taxes that, together, can replace the lost property tax revenue. These can include selective sales or excise taxes on certain goods and services, including vehicles, alcohol, marijuana (especially if recreational marijuana is ever legalized in Michigan), meals, vehicle rentals, entertainment or amusement services, and sharing economy services (i.e., ride-sharing or home-sharing). Many of Detroit’s peer cities (i.e., other big cities in Great Lakes or Midwestern region states) allow local units to levy either general retail sales taxes or selective sales taxes that are not allowed in Detroit.

If the state authorizes Detroit to levy more local-option taxes, this does not require the city to levy them, but simply expands the menu of tax options available to local officials and voters when choosing tax and service levels. Once a tax is approved at the state level, the Detroit City Council would need to pass an ordinance or resolution to levy the tax at whatever rate is desired and allowed for in state law. Then, local voters would have the final say as to whether any new local tax could be levied. The Michigan Constitution prohibits units of local government from levying any new taxes, or raising the rates on any existing taxes, without voter approval.

Detroit has emerged from bankruptcy and growth is clearly evident downtown, in midtown, and in pockets beyond, but even with its more diversified local revenue structure, it may not be able to weather the next financial storm without more local-option revenue sources available to it. More local-option taxes in Detroit could help to further diversify the city’s local revenue structure, allow it to benefit from the economic expansion happening downtown and throughout the city, and increase its appeal to residents and businesses with lower property tax burdens.